|

BOX 1.1 A Family Perspective This report, the third of the Committee on the Consequences of Uninsurance, examines the impacts on America’s families of not having health insurance for all their members. On the basis of a literature review this report provides new analyses of the consequences of a lack of insurance within families and the effects on the health of children and pregnant women. The Committee looks at the phenomenon of uninsurance from the perspective of the family, which is important for several reasons:

|

1

A Family Matter

When a member of a family is sick, the whole family can be affected. This report examines whether having an uninsured member of the family might affect the entire family, also. More than 38 million Americans are uninsured.1 In addition to the personal consequences for those people without coverage, another nearly 20 million immediate family members who are insured may also be affected by the lack of coverage of others in the family.2,3 This report will assess the literature on the physical and psychological health consequences as well as financial effects on the entire family unit of having one or more members uninsured.

This report of the Institute of Medicine (IOM) Committee on the Consequences of Uninsurance provides new analyses of the effects of not having health insurance within families (see Box 1.2). The Committee builds on the first report, Coverage Matters, which examines the dynamic, fragmented structure of health insurance in the United States, the causes of uninsurance, and which individuals

|

1 |

The Committee’s earlier reports refer to roughly 40 million uninsured individuals, based on the 1999 and 2000 Current Population Surveys (CPS). The 2001 CPS was available for this report and shows a dip to 38.7 million uninsured persons (Mills, 2001). |

|

2 |

Analyses in this report are based on tabulations of the March 2001 Current Population Survey (CPS) public use file designed to aggregate data by family units conducted by Matthew Broaddus, Center on Budget and Policy Priorities. |

|

3 |

The CPS estimates those who have been uninsured for the complete year. It has been criticized for probably over-estimating that number and underestimating the number covered by Medicaid. For example, in 1996 the CPS estimate of the number of nonelderly uninsured persons was 41 million and Medical Expenditure Panel Survey estimated 32 million for that year (Lewis et al., 1998; Fronstin, 2000). For a discussion of the main national surveys including insurance status see Coverage Matters, Appendix B. |

|

BOX 1.2 Committee Terminology The Committee specifies particular meanings for terms used in this report as follows:

|

are likely to be uninsured. It also extends the second report, Care Without Coverage, which concludes that health insurance is a vital factor in promoting good health for adults. This report provides analyses of two distinct sets of evidence: 1) studies of insurance effects on the health of children and pregnant women and 2) studies of the interactions within families that may be affected by the lack coverage of individual members.

The Committee recognizes that insurance coverage alone is not enough to ensure improved health outcomes. There are nonfinancial barriers to care as well, such as insufficient education to realize when health care is needed, inability to take time off from work to go to the doctor, lack of needed specialists in the immediate area, lack of culturally and linguistically appropriate services, and psychological inhibitions or fears about seeking care. In addition, there are lifestyle choices, such as smoking, diet, exercise, and alcohol use, that can affect health status and outcomes, even when appropriate care is sought. Nevertheless, insurance remains a very important factor in individual health.

This chapter first presents the purpose of the report and the rationale for using a family perspective to examine the impact of not having insurance. These sections are followed by a brief discussion of how families get health coverage—whom the family may consider to be its responsibility, whom insurers consider family for

coverage purposes, and how families evolve and change in relation to these definitions. Finally, the conceptual framework that guides the Committee’s work is briefly presented, as well as an overview of the report.

PURPOSE OF THE REPORT

The first of two main purposes of this report is to examine the patterns and consequences of having uninsured members within the family.4 The report looks at the health and financial impacts on families with and without children. As such it represents a departure from most research on the uninsured, which focuses on the effects of health insurance on individuals. Much of the current debate does not capture the impact on the family of having some or all members uninsured.

The family constitutes a useful vantage point because most people do not live alone but rather in family units. The Committee examines whether the poor health or impaired functioning of one member can affect the physical, psychological, social, and economic well-being of the unit as a whole. In fact, in this country, more than 85 percent of individuals live in families.5 Not all members of a family have the same opportunities for health coverage or can be insured by the same plan or program. The patterns of coverage within a family result in part from the sources and structure of health insurance plans and programs. This report documents the effects that a lack of coverage may have not only on the uninsured members and their health status but also the care that insured members, particularly children, receive.

The second purpose of this report is to update and reassess analyses of the impact of insurance status on the health of children and pregnant women. The Committee reviewed the literature to determine whether there are documented clinical differences associated with the insurance status of pregnant women, infants, and children. Health insurance or lack of coverage affects and is affected by family interactions, so the Committee has given particular attention to research on health outcomes in the context of the family.

Whether family members have coverage or not was the critical variable of interest in the studies reviewed. However, some studies also considered the differing impacts of public and private coverage. Distinctions based on variations in benefit levels and aspects of underinsurance are generally not addressed by this report.6 In its previous report, Care Without Coverage, the Committee shows that

|

4 |

Generally the Committee focuses on families with uninsured individuals, defined as those having no coverage for any health benefits and no assistance in paying for health care other than what is available through charity and safety-net institutions. Since the federal Medicare program provides almost universal coverage for individuals at least 65 years old, the Committee concentrates analyses on the population under age 65. (See Appendix B for a description of Medicare.) |

|

5 |

The data used in this report generally exclude families with all members over age 64 because Medicare covers almost all of them. |

|

6 |

The Committee recognizes the importance of underinsurance but in this project focuses primarily on family members with no insurance. |

uninsured adults suffer diminished health and experience reduced life expectancy. This report determines whether pregnant women, newborns, and children without insurance experience similar negative effects.

NEED FOR A FAMILY PERSPECTIVE

Social and economic life in America is organized around families. The health and well-being of families is especially important in determining children’s opportunities later in life (Shonkoff and Phillips, 2000). The health of any member can affect the whole family. Yet our most important means to obtain health services— health insurance—is frequently offered on an individual basis or with only partial regard to an individual’s family circumstances. The mismatch between families’ functioning as a social and economic whole and the qualification for insurance coverage as individuals is at the root of many of these negative consequences for family members and the family unit.

Four aspects of family experience distinguish the consequences of uninsurance for families from the consequences of uninsured persons considered strictly as individuals: (1) the health of one member can affect other family members; (2) public programs designed to provide coverage for individuals frequently do not consider the implications for family units; (3) parents make decisions about their children’s care that may be influenced by their own experiences with and attitudes toward the health system; and (4) as individuals within the family mature and age, transitions of age, work, and marital status can trigger loss of coverage for the family.

First and foremost, the health of one family member can influence the health and well being of other individuals within the family and the family as a whole. Care Without Coverage: Too Little, Too Late documented how being uninsured compromises the health of individual adults. This report examines how individuals’ lack of insurance affects the health of pregnant women, children, and families as a whole. When parents’ health is impaired, their ability to care physically and emotionally for their children may be adversely affected as well. A focus on the consequences within a family of having no insurance draws our attention to the relationship between parental health and its impact on children.

Second, examining uninsurance in a family context highlights the fact that most publicly financed health insurance programs have been designed to provide coverage to individuals. If all individuals were entitled to the insurance, there would be no issue of a mismatch of family definitions or a gap in coverage. Without universal coverage, however, the issue of who qualifies for coverage and who does not is real. Families may find that different members are eligible for different programs, while some members are not eligible at all. When family members have different sources or types of coverage, each family member may be required to use a different doctor, hospital, or clinic. Considering the family as the unit of analysis leads to an examination of the effects that a patchwork of programs may have on access to health services and health outcomes for family members.

Third, parents or other adults in the family unit often make decisions about health care for younger members. Parents’ experiences with the health care system, their beliefs about health care, and their ability to negotiate that system on their children’s behalf may influence whether and how even children with coverage actually use appropriate services. The fact that family members may be eligible for coverage does not guarantee that they will enroll. Furthermore, being enrolled does not assure use of services. This report examines some of the financial and nonfinancial barriers to use of services that can affect health outcomes.

Fourth, looking at the family as a whole highlights how individuals’ insurance needs and opportunities change over the life cycle of the family. This broad view of families across age categories encompasses the interplay in young families between parents’ and children’s health coverage status and use, changes in health care coverage as children approach adulthood, and evolving relationships to work as couples approach retirement. For example, late-middle-age couples are likely to have increasing health needs and one or both may feel ready to retire, but neither may be eligible for Medicare (IOM, 2002a,b).

HOW FAMILIES GET HEALTH INSURANCE COVERAGE

The rate of uninsurance for families stems, in large part, from differences between how families manage their finances, make decisions about health care, and define themselves as a functional economic unit on the one hand, and how employers, insurers, and public programs set the rules for individual and family coverage on the other. There are many, often inconsistent, definitions of family. This definitional mismatch has implications beyond limiting the data available for research. Definitions of family used by insurance companies often do not fit actual dependency relationships. Public programs may ignore family links altogether. Because both family composition and opportunities for health insurance change over time, gaining and keeping health insurance for all of its members pose a challenge for families. These factors contribute to a mixture of coverage patterns within families.

Individuals’ perceptions of what makes up a family and who is a member reflect a richness and variety of human experiences. This richness is often lost when researchers attempt to count and measure what happens to and within families because demographic analysis relies on uniform definitions and historical conventions in order to count people and families consistently. The definition of family used for statistical purposes and the constraints it imposes are discussed further in Chapter 2.

The Insurance Unit

Most health insurance coverage in the United States is provided by employers and governments. Insured family members receive coverage through their job or

that of a family member or through a government program such as Medicaid or Medicare. Public programs and employers may limit who gets insurance, under what conditions, and for how long.

Employers offer health insurance to their employees as a pre-tax workplace benefit. Generally they also offer coverage to the immediate family members of their workers but often contribute a lower proportion of the premium compared to their worker-only contribution. Virtually all larger firms (200 or more workers) and 65 percent of small firms (3–199 workers) offer at least some of their employees health insurance benefits, usually with the employer paying part of the premium, and generally make health insurance coverage available to family members as well (Kaiser-HRET, 2001).7 In this way, employers facilitate insurance of families. Employers and the health insurance plans that they sponsor decide which family members are eligible. Family coverage includes the spouse and children of the employee, but policies vary in how long a dependent child can stay on as part of the family policy.

Insurance companies, employers, and the public sponsors of coverage define a family-based “insurance unit,” which may be different from a family-defined “responsibility unit.” A grandmother taking care of her grandchildren, a brother and sister living together and, in some cases, long-term companions might consider themselves family and feel responsibility toward each other. If one member of the unit became ill, the other would see to it that care was provided and paid for, to the best of his or her ability. Yet individuals in these family responsibility units might not be able to provide insurance for all the members through traditional employment-based insurance and they may not be eligible for public insurance coverage. The family responsibility unit might also extend to members living outside the immediate household. For example, parents of a 22-year-old recent graduate living independently with an entry-level job and no insurance might assume responsibility for some of the adult child’s health care costs in the event of an illness or injury. In fact, one-third of the public has someone outside their household—an elderly parent (13 percent), a grown child (8 percent), another family member, or a friend (14 percent)—for whom they feel responsible for seeing that they get proper medical care (NPR-Kaiser-Kennedy School of Government, 2002). One-third of those with this responsibility said that the person had problems getting medical care.

Government programs, in contrast to employment-based coverage, often insure individuals. For publicly funded coverage in programs such as Medicaid, Medicare, and the State Children’s Health Insurance Program (SCHIP), the public at large through its legislatures decides what groups of individuals are eligible. (All

three programs are described in Appendix B.) Currently, these groups include lower-income persons, sick people with high medical expenses, the disabled, and those over 65 years of age.8 Within the lower-income group (i.e., persons in families with incomes below 200 percent of the federal poverty level [FPL]), children, the disabled, and pregnant women have priority and to a lesser extent, so do parents. In addition to the federal and federal–state programs, several states have independently designed health insurance programs and subsidies using state revenues. Because the rules for these government programs are written to make it easier for people in priority age groups and in particular circumstances to get insurance, within a given family some members may be eligible for government insurance programs and others not. For example, a pregnant woman and later her infant might be covered through Medicaid because the income eligibility standard is relatively generous for these categories, but older siblings of the infant and the woman’s husband might not be eligible for coverage because the income eligibility standard is more restrictive for older children and most restrictive for adults (other than pregnant women). Often adults who are neither pregnant, disabled, nor over 65 are ineligible regardless of how little income they have.

Dynamic Nature of Families and Society

Changes in a family’s circumstances may lead to the gain or loss of eligibility for insurance coverage by one or more family members. Even when public policy or private insurance practices include family members initially, a change in a family’s circumstances can create new exclusions, some of which may be surprising. Many of the family transitions related to age, employment and marriage that can trigger a withdrawal of coverage are normal life occurrences that most of us experience. For example, a 62-year-old woman insured through her 65-year-old husband’s employer might find herself uninsured when he retires at 65. The husband would be covered through Medicare, but the wife might be without insurance for the three years before she turns 65 and becomes eligible for Medicare.

Broader social, political, and economic developments may also lead employers and the government to change the terms for offering coverage, which may in turn result in family members gaining or losing eligibility for coverage. Insurance

|

8 |

Family income levels are defined as follows: • Low income: an annual income of less than 100 percent of the federal poverty level (FPL), which is established on a yearly basis for different types of family groups that comprise a given household, for example, one adult, or one adult and two children; • Lower income: an annual income less than 200 percent of FPL; and • Moderate income: an annual income between 200 and 400 percent of FPL for a given family group. See Appendix D, Table D.1, for federal poverty levels. |

rules are not static but change with fluctuating public policy, business practices, and economic conditions. Insurance rules also reflect a changing social consensus about who should be covered or considered “family.” Since the mid-1980s, beginning with Medicaid eligibility expansions for pregnant women and young children, and extending through the enactment and implementation of SCHIP in the late 1990s, public programs have reflected a growing commitment to ensuring health coverage for lower-income children. Another example of social values changing toward a broader definition of family and influencing insurance rules is that in the private sector, almost 20 percent of workers are employed in firms that have extended their definitions of family to include nontraditional partners— same-sex partners and unmarried heterosexual couples (Kaiser-HRET, 2001).

Changes in economic conditions can also affect how employers and the public sector define who is eligible for family coverage and on what terms. In the past, a rapid rise in health care costs and a downturn in the economy have led employers to reduce coverage to dependents and increase premiums and copayments for their employees. This has begun to happen again (Gabel et al., 2001; Kaiser-HRET, 2001; Freudenheim, 2002). Likewise, public programs may decrease efforts to expand coverage to uninsured individuals, cut back on existing coverage, or be less aggressive in encouraging enrollment. Reductions in public coverage can result from explicit policy changes to limit enrollment or tighten eligibility requirements or through administrative actions to make enrollment and re-enrollment more difficult. Forty-seven states report having instituted in fiscal year 2002, or planning to introduce in fiscal year 2003, policies to reduce Medicaid expenditures, including increased copayments, reduced provider payment rates, and reduced optional benefits and eligibility groups (NASBO, 2002). In the past, during some periods of decline in employment-based insurance coverage, Medicaid expansions served to mitigate the impact of the decline on the number of uninsured people, but that cushion may be reduced (IOM, 2001).

In an attempt to capture some of these dynamics of the economic and social factors affecting family units that may not be clear from the statistics and to add a human dimension, some of the following chapters begin with a vignette or example of family circumstances based on the research in the chapter. These vignettes are composites of circumstances documented in the research literature that illustrate family experiences related to not having health insurance. The vignettes integrate that information to enrich understanding of the issue and broaden the perspectives on family.

CONCEPTUAL FRAMEWORK

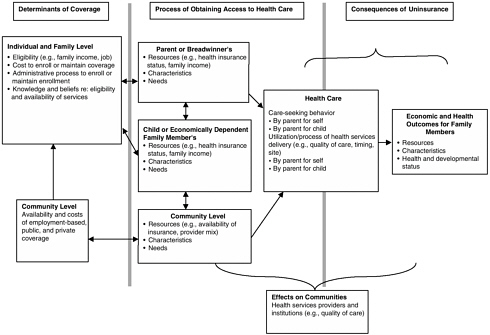

To guide its assessment of the literature on the health, social, and economic consequences for families of having one or more uninsured members, the Committee uses a conceptual framework based on a widely accepted behavioral model of access to health services (Andersen, 1995; Andersen and Davidson, 2001). This framework provides a common grounding to the Committee’s six reports.

The conceptual framework as adapted for the family-level analysis in this report extends the framework or model introduced in the Committee’s first report, Coverage Matters, to highlight the findings regarding family effects; see Figure 1.1. It makes explicit the interdependence and shared decision making within families and suggests how such interdependence may influence the relationship between the health insurance status of family members and the receipt of health care. Appendix A provides a further description of the framework.

Characteristics such as income, race, and family structure, which are discussed in the next chapter, are included in the parent and child boxes in the middle panel of Figure 1.1. These characteristics may affect the individual and family-level determinants of coverage in the panel on the left. For example, the family’s income level can determine whether the children in the family will be eligible for public health insurance and may affect whether and how frequently parents will seek care for their children. The relationship between the availability of insurance plans and family members’ eligibility for them is examined in relation to family characteristics and needs in Chapters 2 and 3.

The use of health services by children, influenced both by the insurance status of the child and the parent and by other family and individual characteristics and needs, can affect the child’s health and long-term development as well as the family’s economic health. These relationships are depicted as one moves from left to right across Figure 1.1. The financial and health consequences of uninsurance on the individual pregnant woman, child, and the whole family are the main focus of this report (Chapters 4–6). The health effects of uninsurance on working-age adults was the subject of the Committee’s previous report and is not discussed here. The health outcomes of pregnant women were not discussed in the previous report, however, and are covered in Chapter 6. In Figure 1.1 feedback loops operate among most of the boxes but not all are indicated, in the interest of clarity. For example, the poor health outcome for one child in the family (in the panel on the right) could cause health problems for another family member, possibly affecting the health needs and insurance status of a parent (boxes in the middle panel).

The mix of health services providers and institutions, their numbers, and their costs and revenues are factors at the community level that influence a family’s process of obtaining care—where it chooses to go for treatment as well as how frequently its members might seek care. The factors in the boxes labeled community level and effects on communities also are affected by the health care obtained in aggregate by all families. The economic and health outcomes of all families in aggregate can influence where doctors may choose to locate and what level of service quality hospitals can afford to provide. The quality of care that patients receive, as well as the costs of that care at the community level, reflect the care-seeking behavior of parents and children. The various community effects will be discussed in more detail in the Committee’s next report on community effects of uninsured populations.

REPORT OVERVIEW

This report provides new analyses of the consequences of a lack of insurance within families and the effects on the health of children and pregnant women. In the second chapter, the Committee examines insurance coverage patterns within families, including sources of coverage. The chapter describes the types of families that are most likely to have uninsured members and the characteristics associated with having some or all members uninsured. Chapter 3 considers the key transitions over a family’s life cycle that may affect insurance coverage, including aging and changes in employment and marital status. Chapter 4 discusses how family income, assets, and spending patterns affect and are affected by family choices about health insurance and purchases of health care and how being uninsured affects family economic stability. Chapter 5 describes the factors that may influence the health care decisions that parents make for their children, including their own experiences with the health care system. In addition, that chapter discusses the effect of parents’ health on the family environment and their children’s health. Chapter 6 assesses evidence on health and developmental outcomes associated with health insurance status for children, infants, and pregnant women. The Committee’s conclusions are presented in the seventh and final chapter.