6

Social and Economic Costs of Uninsurance in Context

In the previous chapters of Hidden Costs, Value Lost, the Committee

-

developed an analytic structure for examining the societal economic impacts of uninsurance,

-

reviewed estimates of the costs of health care that those who lack coverage now use and identified the parties bearing these costs,

-

estimated the expected gain in health capital that insuring the uninsured would achieve,

-

considered additional, unquantified costs that uninsurance imposes on uninsured individuals and families, and society at large, and

-

presented estimates of the costs of the additional health care that the uninsured could be expected to use if they gained coverage.

This concluding chapter brings these various elements of costs consequent to uninsurance together, along with the anticipated costs and benefits of expanded coverage. Consolidating this information allows the Committee to consider whether allocating scarce social resources to expanding coverage to the more than 41 million uninsured Americans is worthwhile, and how it compares with other investments our society already makes in health- and life-enhancing services and interventions.

The Committee has also reserved for this final chapter an important discussion of the nonmaterial consequences of our nation’s policies regarding health insurance and access to health care. It is difficult to make claims about what our national tolerance of uninsurance is costing us ethically and politically because health insurance and even health care have never been recognized as rights of

citizenship or social membership that apply universally in the United States. Thus the Committee asks the converse question: What do we as a nation stand to gain by ensuring that all Americans have health insurance coverage? The Committee concludes that adopting a policy of universal health insurance coverage would be a societal expression of values and norms that are deeply, if sometimes obscurely, embedded in American culture and history.1

Box 6.1 at the end of the chapter consolidates the Committee findings from previous chapters as well as this one.

SUMMARIZING COSTS AND COMPARING INVESTMENTS IN HEALTH

Conclusion: The estimated benefits in terms of the value of healthy life years gained by providing coverage to those currently uninsured are likely greater than the incremental societal costs of the additional health care services that they would receive if insured. The costeffectiveness of the additional health care that the uninsured population would use with coverage is comparable to that of many other health-enhancing and life-extending interventions.

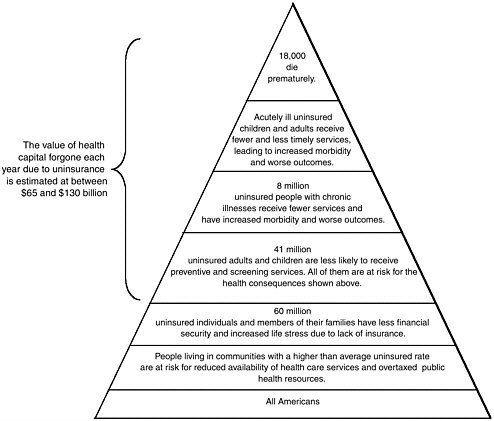

In its reports and analyses so far, the Committee has thought about and depicted the relationships among the various hypothesized and documented consequences of uninsurance in terms of a series of concentric circles, broadening outward, as in Figure 1.1. Because the Committee has considered health insurance primarily as it facilitates the receipt of health care by individuals, the health consequences for individuals are at the center of the circle. Immediately “ringing” the circle of uninsured individuals are their family members, a greater number of persons than the uninsured themselves who are at risk for adverse health, psychosocial, and economic impacts related to the uninsured status of a family member. One ring further out from families represents the communities in which uninsured persons and their families reside. Communities with higher-than-average uninsured rates comprise a larger population than that of the families that have at least one uninsured member. Residents of these communities may experience reduced access to health services even when they are insured themselves. Finally, ringing the communities is American society overall, where all members who pay taxes, purchase goods and services, and benefit from the presence of an educated and

FIGURE 6.1 Consequences of uninsurance.

productive workforce are likely to experience the adverse consequences of uninsurance socially and economically, even those who live in communities with relatively few uninsured persons.

Figure 6.1 presents a wedge sliced out of the concentric circles just described. This slice or pyramid helps visualize the numbers of people affected in different ways by uninsurance. It illustrates the ever greater numbers of Americans adversely affected at each ring or band from the cross-section of the circle. The tip or smallest band indicates the number of uninsured individuals who die prematurely because of their uninsured status, an estimate from the Committee’s second report, Care Without Coverage. The next two bands add in the number of acutely and chronically ill persons under age 65 who receive less adequate and effective care because of their lack of coverage, as documented in the Committee’s second report and its third report, Health Insurance Is a Family Matter. Yet the uninsured people who fall ill or suffer injury are only some of the over 41 million persons who lack coverage, all of whom are at risk for adverse health and economic consequences. The 41 million uninsured persons are members of families, leading to an estimated total of 60 million persons who also bear some of the adverse

financial, psychosocial, and utilization effects of lack of coverage within the family. The 60 million members of families with at least one uninsured person are in turn residents and members of communities that may experience spillover effects of a relatively large uninsured population. Whether through residence in a community with a disproportionately large or growing uninsured population, or as a taxpayer and citizen, uninsurance touches the lives of all 284 million Americans.

Table 6.1 lists the elements of costs related to uninsurance that were examined in Chapters 3 and 4 and presents estimates for a few of them: expenditures for uncompensated care, forgone health capital, and the risk borne by uninsured people. Even though these are all expressed in monetary terms, they are not simply additive. The cost of uncompensated care provided to uninsured patients, a transfer, is meaningful only in terms of who is bearing this cost—ultimately, primarily taxpayers at all levels of government. (The cost of covering the uninsured will undoubtedly require additional transfers from taxpayers to those newly covered.) Both the value of the stock of health that those without coverage forgo as a result and the burden of financial risk that they are exposed to represent economic opportunity costs or losses to uninsured individuals themselves. These quantified values reflect only some of the very real costs of uninsurance.

Table 6.2 presents in summary form estimates of the current costs of care for the uninsured and projected costs and benefits of coverage. The annual incremental cost of the services the current uninsured population would use if health insurance coverage were universal cannot be compared directly with the annualized present value of the cumulative future benefits of coverage because they are expressed in different metrics.

The final step in the Committee’s analysis of economic costs is to consider the potential benefits of providing the uninsured with coverage together with the incremental costs of the additional health services that would improve their health. In order to do this, both the average per capita gain in health due to an additional year of health insurance for the uninsured population and the average per capita annual cost of the additional health services that the uninsured population would use if they had coverage must be made consistent with each other. The estimate of the value of health gained with an additional year of coverage is calculated as a discounted present value of the gain for a cohort of uninsured people over the course of their lives (with a range of $1,645 to $3,280, as presented in Table 4.1), and thus the estimate of the cost, for each additional year of insurance, of the additional health care that the uninsured would use if insured must be calculated as the present value for an uninsured cohort over the course of their lives.

The Committee calculated the present value of incremental costs for an uninsured population of the current size and demographic composition based on the Hadley and Holahan (2003b; see Chapter 5) analysis of projected incremental health care costs using a 3 percent discount rate. The cost per additional year of health insurance provided to the otherwise uninsured is the expected lifetime increase in service costs with continuous coverage up to age 65, divided by the additional years of coverage provided over the lifetime. The estimated range of per

capita costs for the incremental services calculated in this fashion is $1,004 to $1,866, depending on whether the incremental service costs are calculated based on public or private health insurance expenditures.2 The estimated benefits ($1,645–$3,280, from Table 4.1) fall in a higher range than the estimated incremental, societal costs ($1,004–$1,866). Because not all of the care that the insured population use is likely to be effective and contributing to their better health outcomes (i.e., some insured care is wasteful and even harmful [IOM, 2001b]), the comparative value of the estimated health benefit achieved with these incremental services, which represent both effective and marginal or ineffective care, is even more notable.

Another way to help judge whether investing in health insurance for the uninsured is “worth it” to Americans as a society is to compare this investment with other investments in health that we do make. Table 6.3 arrays cost-effectiveness ratios, with the costs of adopting the intervention expressed in terms of the cost for each additional quality-adjusted life year (QALY) gained, for selected life-saving and health-improving measures. This array includes the Committee’s estimate for the intervention of providing continuous health insurance across the population in boldface type. Dual passenger airbags in autos (compared with airbags on the driver side only), for example, has a cost for every quality-adjusted life year gained of $75,000. Compared to an annual clinical breast exam, an annual mammography for women between ages 55 and 65 carries a cost of $186,000 for every QALY gained. Among women ages 20 to 75, the cost of every additional QALY gained with annual Pap smears (compared with one every 2 years) is $2 million (Graham, 1999).

The Committee calculated the incremental cost per QALY gained by insuring the uninsured by dividing the incremental cost per additional year of insurance provided by the change in QALYs per additional year of insurance provided (see Table 6.4). The change in QALYs per additional year of insurance provided is the total lifetime increase in QALYs from gaining insurance, divided by the number of years of insurance provided over the remaining lifespan. The expected lifetime gain in QALYs is the expected gain in health capital divided by the imputed value of a life year ($160,000).

Converting the Committee’s benefit-cost figures for the health value gained relative to the incremental cost of additional health services with coverage yields an incremental cost per QALY of between $50,000 and $180,000. This range reflects two different upper and lower bounds: one is the difference between the cost based on public versus private coverage and the other the high- and low-bound assumptions about differences in the underlying health status of demo-graphically similar insured and uninsured populations. Providing health insurance

TABLE 6.1 Costs of Uninsurance, Estimated (Annual) and Hypothesized

|

Who Is Affected |

Consequence |

Units |

Value per Unit |

Total Estimate |

|

Internal Costs |

||||

|

Individuals |

Morbidity Premature mortality |

Disease prevalence rates Decreased life expectancy QALYs |

$160,000/year of life in perfect health |

$65–$130 billion (Forgone benefits of coverage) |

|

Families |

Developmental losses for children |

Educational attainment |

|

(Subsumed in health capital) |

|

|

Interactive health effects |

Differential coverage and utilization effects for children by parental coverage status |

|

(Subsumed in health capital) |

|

Stress and financial uncertainty |

Value of risk borne by uninsured individual |

$40–$80 annually per uninsured individual |

$1.6–$3.2 billion (Forgone benefits of coverage) |

|

|

Depletion of assets |

Assets; bankruptcy |

|

(Transfer) |

|

|

Firms |

Time lost from work; reduced productivity on the job |

Absenteeism Value of lost production |

Unknown |

|

|

External Costs |

||||

|

Communities |

Uncompensated care: Diverted public resources or additional taxes to pay for care to uninsured |

Local tax burdens for uncompensated care Allocational decisions for public budgets Losses from inefficient care for the uninsured |

|

$35 billion (Current expenditures; primarily transfers) |

|

|

Diminished quality, availability of health services |

Community-wide unavailability of specialty services |

Unknown |

|

|

Diminished population health, costs to other public programs |

Immunization rates; contagious disease rates; disability rates |

Unknown |

||

|

Nation |

Workforce productivity |

Labor force participation Disability rates |

Unknown |

|

|

Unrealized social norms |

|

Not quantifiable |

||

TABLE 6.2 Estimates of Current Annual Cost of Health Care Services for Full- and Part-Year Uninsured Individuals, Projected Incremental Annual Costs of Services If Insured, and Economic Value Gained by Uninsured Individuals If Insured, Annualized

|

|

Billions $, estimated for 2001 |

|

Current cost of care for full- and part-year uninsured |

98.9 |

|

Amount paid out of pocket by full- and part-year uninsured |

26.4 |

|

Insurance payments (for part-year uninsured only) and workers’ compensation |

|

|

Private |

24.2 |

|

Public |

13.8 |

|

Uncompensated care |

34.5 |

|

Projected annual costs of additional utilization with coverage |

34–69 |

|

Benefits of insuring the uninsured |

|

|

Aggregate value of health capital forgone by the uninsured, annualized |

65–130 |

|

Aggregate annual value of risk borne by uninsured |

1.6–3.2 |

|

SOURCES: Hadley and Holahan, 2003a,b; Vigdor, 2003. |

|

to those who now lack it is likely to be at least as cost-effective in enhancing health and longevity as some other common health care practices.

The final section of the chapter presents the Committee’s reflections on the ethical and political significance of health insurance within American society. Claims about cultural values and implicit social norms are particularly likely to be challenged as lacking adequate empirical grounding; nonetheless, the Committee believes it would be irresponsible to remain silent on normative issues and attempts to articulate American cultural and political normative underpinnings and their implications for the health policy choices Americans now face. That some of the benefits of expanding health insurance coverage to the entire population are not quantifiable makes them no less important to our strength and integrity as a democratic national community.

REALIZING SOCIAL VALUES AND IDEALS

Conclusion: Health insurance contributes essentially to obtaining the kind and quality of health care that can express the equality and

TABLE 6.3 Cost-Effectiveness Ratios for Selected Life-Saving Measuresa

|

Intervention |

Comparator |

Target Population |

Cost per QALY Saveda |

|

Annual colorectal screening |

No screening |

People 50–75 |

$22,000 |

|

Frontal airbags with manual belts |

Manual belts (50% use) |

Drivers of passenger cars |

$30,000 |

|

Radon mitigation in homes |

No testing or mitigation |

Home residents with radon levels above 20 pCi/liter |

$71,000 |

|

Dual passenger airbags |

Driver side only |

Front right passenger |

$75,000 |

|

Coronary angioplasty |

No revascularization |

Patients with mild angina and one-vessel disease |

$136,000 |

|

Universal coverage |

16.5% uninsured population under age 65 |

Currently uninsured |

$50,000–$180,000 |

|

Annual mammography |

Annual clinical breast exam |

Women ages 55–65 |

$186,000 |

|

Annual mammography |

Annual clinical breast exam |

Women ages 40–50 |

$297,000 |

|

Methylene chloride exposure limit of 25 ppm |

Limit of 500 ppm |

Workers exposed to methylene chloride |

$235,000 |

|

Solvent-detergent to eliminate AIDS virus and other infectious diseases |

No solventdetergent |

Patients undergoing plasma transfusion |

$384,000 |

|

Screening to prevent HIV transmission to patients |

Universal precautions |

Health care workers in acute care setting |

$606,000 |

|

Annual Pap smear |

Pap smear every 2 years |

Women ages 20–75 |

$2,000,000 |

|

Lap/shoulder belts (9% use) |

No restraints |

Rear-center seats of cars |

$3,000,000 |

|

aAll dollars have been adjusted to 2001 dollars by the medical care price index. SOURCES: Graham, 1999; Estimate for universal coverage is by the Committee. |

|||

TABLE 6.4 Incremental Cost-Effectiveness Analysis of Continuous Health Insurance Coverage for the Uninsured (Estimates for 2001)

|

|

Average change in cost per additional year of insurance, $ |

Average gain in health capital per additional year of insurance, $ |

Average gain in health capital per additional year of insurance, QALYs |

Incremental cost/QALY, $ |

|

Private coverage |

1,866 |

|

||

|

YOL |

|

2,014 |

0.013 |

148,257 |

|

QALY lower bound |

1,645 |

0.010 |

181,489 |

|

|

QALY upper bound |

3,280 |

0.020 |

91,018 |

|

|

Public coverage |

1,004 |

|

||

|

YOL |

|

2,014 |

0.013 |

79,769 |

|

QALY lower bound |

1,645 |

0.010 |

97,650 |

|

|

QALY upper bound |

3,280 |

0.020 |

48,972 |

|

|

SOURCES: Committee estimates, from Vigdor, 2003, Hadley and Holahan, 2003b. |

||||

dignity of every person. Despite the absence of an explicit Constitutional or statutory right to health care (except for emergency care in hospitals), disparities in access to and the quality of health care of the kind that prevail between insured and uninsured Americans contravene widely accepted democratic cultural and political norms of equal consideration and equal opportunity.

Any kind of accounting of societal costs and benefits from the investment of economic resources in a policy like universal health insurance relies on some kind of unit of value: money, years of life, QALYs, or personal utility.3 Health care is valued for its contribution to personal health. Likewise, health insurance is valued instrumentally because it facilitates receipt of health care, an additional step removed from health itself. We value health insurance in part because it gives us access to services from which we expect to benefit, even for services far beyond our means to pay out of income and personal savings (de Meza, 1983; Nyman, 1999a,b). Because of the value of health and longevity is not something that we (in American society in the 21st century) readily trade off against other goods that can be purchased in the market place, there is good reason to account for it separately (Culyer, 1991; Weinstein and Manning, 1997).

In addition to the aggregate of costs and benefits calculated for individual lives, collective experiences and circumstances also depend on societal choices about health care and the distribution of health insurance coverage among members of society. In the following discussion, the Committee reviews some of these irreducibly collective implications of policy choices about health care and health insurance in American society. It also considers whether the failure to enact a national policy that guarantees everyone health benefits undermines the Committee’s conclusion that equity in access to health care is an important expression of central democratic values of equality of opportunity and mutual respect.

Altruism, Mutual Concern, and Health Care

Americans share a somewhat vague consensus that everyone should be able to obtain at least some forms and amount of health care under certain circumstances. Just how much health care, paid for by whom, and under what circumstances are contended.

In A Shared Destiny, the Committee reviewed the history of collective provision of health care in the United States, beginning with hospital charities in the 18th and 19th centuries to care for the poor and, by the middle of the 20th century, instituting public health insurance programs for particularly vulnerable

groups including the elderly, very low-income mothers and children, and the disabled. Despite numerous amendments to and expansions of the original Medicare and Medicaid statutes enacted in the mid-1960s, and greater state and federal regulation of commercial health insurance and employment-based health benefits to allow Americans to secure and maintain insurance coverage and financial access to health care, as a society we have stopped short of guaranteeing the benefits of health insurance to everyone and have tolerated endemic uninsurance.

Some argue that the growth of public provision in care and coverage “crowds out” charitable provision, depriving some of the opportunity to express their altruistic interests by donating to others (Epstein, 1997). On the other hand, some economists have argued that, because so many consider health care to be a good that should be provided to (at least some) people on the basis of need and not ability to pay, personal health care is actually a special kind of public good, a merit good (Musgrave, 1959, Fuchs, 1996). The externalities or spillover effects of providing merit goods are not material, but psychological. They are the utility or satisfaction one gets from knowing that others obtain the good one wants them to have. By providing health care or coverage through public provision, taxpayers benefit from knowing that others are receiving needed care, that suffering is reduced, or that families are not becoming impoverished by medical bills (Coate, 1995).

Experimental studies of distributional choices in health care suggest that people favor equity of some form in this arena.4 Egalitarian distributive choices in experimental settings have been demonstrated for goods, including health care, to which the notion of need, rather than that of taste or preference, applies (Yaari and BarHillel, 1984). Presented with the hypothetical scenario in which respondents were asked to allocate a fixed amount of pain medication between two people, identical in all respects, including level of pain—except that one could not metabolize the pain medication as well as the other, more than three-quarters of the respondents chose to allocate the medication so as to equalize the pain experienced by each of the individuals (Kahneman and Varey, 1991).

Compassionate attitudes and expectations of mutual trust and concern among neighbors and fellow citizens are not static. They interact with and develop in response to particular features of civic life and the reasonable expectations that members of a society have regarding the collective provision of important social goods, such as health care. The strength and resiliency of communities as social, political and economic entities depend in part on intangible social resources sometimes referred to as social capital. Social capital is reflected in the extent of civic engagement, in the expression of norms of reciprocity among members of a community, and in the degree of trust among people who are social strangers.

In A Shared Destiny, the Committee considered the implications that differential access to health care based on insurance status might have for social cohesive-

ness and social capital. Because this relationship had not been explored in empirical studies, the Committee only formulated hypotheses about the possible interactions between uninsurance and social capital. Widespread uninsurance within a community may erode residents’ beliefs or confidence in their ability to take care of themselves or those they care about because of the real or perceived barriers to obtaining care. Conversely, the security or guarantee of financial access to needed care that health insurance offers may enhance the sense of both individual and collective efficacy (Lochner et al., 1999).

Conditions for Achieving Equality of Opportunity and Democratic Equality

Just what the essential equality among members of a democratic society consists of is contested in American political life. Nonetheless, equality in some sense stands with freedom of individual action as a bedrock value of our way of life. Two kinds of equality, however, are particularly fundamental and widely shared: equality of opportunity and equality of respect. The guarantee of health care or the provision of health insurance throughout society can make a unique contribution to the more complete realization of these values.

The state of our health affects what we can do or be in life (Sen, 1993). Building on John Rawls’ (1971) highly influential and more generally constructed theory of justice, political philosopher Norman Daniels (1985) developed an account of the special priority that we place on meeting the health care needs of ourselves and of others. When compared with the priority we give to having a dinner out and a movie, for example, health care is more important because it is necessary for maintaining normal functioning as human beings. The normal functioning of people in a particular society reflects a certain range of opportunities and ambitions that members of that society generally consider open to them. Poor health or disability reduces the range of opportunities and life choices open to us, while health care can restore to us a wider range of opportunities and reasonable plans for life than we might have without it. Because equality of opportunity to realize our own life plans and ambitions is a widely shared American ideal, Daniels’ account is particularly helpful as a way to explain and to justify giving health care and, derivatively, health insurance coverage, a special place in collective provision.

A second set of arguments for equality in the distribution of some kinds of highly valued goods (such as health care) draws on another widely shared ideal in American culture, that of democratic or political equality. Also following Rawls’ original argument, Elizabeth Anderson (1999) proposes that the ultimate goal of equal access to certain valued goods is “to create a community in which people stand in relations of equality to others” (p. 289). Such goods must be made available in ways that express respect for each member of society and not shame or demean those who receive the valued goods. Obtaining health care from public clinics and under charitable arrangements is better than having no access to health care, but for those with no alternatives because of the lack of financial means, it

can be a degrading experience that conveys a sense of one’s social inferiority and political ineffectuality.

When a highly valued social good like health care or health insurance is not available to all members of society, it belies nominal claims that everyone is deemed to have equal political and social worth (Walzer, 1983). Conversely, ensuring that all in society have the means to obtain health care on comparable terms expresses equality of concern and respect and thus can encourage and reinforce participation in social and political activities. Yet it is clear that we have repeatedly chosen not to act to expand health insurance coverage to all. Is this because of a conflict of political and ethical principles, a difference in the interpretation of basic principles, or a failure to recognize what is at stake in the policy choice we have and have not made?

Have We Chosen the Status Quo as a Matter of Principle?

Libertarians, those who place the highest priority on freedom of individual action and personal control over resources and property, believe the state that governs least governs best. Thus, the social contract among a group of equals committed first and foremost to liberty would be a “night-watchman state,” a minimal government that provides for mutual physical security and little else, according to political philosopher Robert Nozick (1974). The night-watchman state is not, however, an accurate characterization of the nature of the social contract that has developed over more than two centuries in the United States, as described in Chapters 1 and 2 with respect to the provision of health care and health insurance.

Hospitals were initially established by communities, both through voluntary associations and as public institutions, as collective resources and expressions of compassion and altruistic concern for the most unfortunate members in society, those who were both sick and impoverished (IOM, 2003a). Medical science progressed rapidly over the course of the 20th century, the value and cost of health care and hospital services rose commensurately with advances in efficacy, and both private and public (social) insurance schemes were established to make these increasingly valuable services within the reach of everyone. The federal tax subsidy for workplace health benefits amounts to between $120 and $160 billion for fiscal year 2003 (Burman, 2003; see also Sheils et al., 1999).

Medicare, Medicaid, and the State Children’s Health Insurance Program enjoy widespread public support and approval (NASI, 1999). Three-quarters of Americans responding in recent nationally representative opinion polls identified increasing the number of Americans covered by health insurance as a “very important” goal for Congress and the President (Kaiser Family Foundation, 2003). Surveys in both 1993 and 2000 found that more than 80 percent of respondents agreed with the statement that health care should be provided equally to everyone, with more than half agreeing “completely” or “strongly.” Two-thirds agreed with the statement that the federal government should guarantee health insurance

coverage for every American (Kaiser Family Foundation, 2003). A February 2003 opinion poll with a national sample of 1,200 asked adults whether they would be willing to pay more in higher insurance premiums or taxes to increase the number of Americans with health insurance. Fifty-two percent said that they would and 42 percent responded that they would not be willing to pay more (Kaiser Family Foundation, 2003). When these same respondents were asked in a separate question whether they would be willing to pay a specific amount more in premiums or taxes each month, the results were somewhat more positive. Forty-six percent said that they would be willing to pay $50 more monthly and 12 percent were willing to pay $30 extra monthly to increase the number of insured Americans.

Despite popular opinion favoring coverage expansions, over the past 30 years national efforts at health care reform extensive enough to provide coverage to everyone—to close the gap of the 15 to 20 percent of the American population without it at any given time over this period—have failed repeatedly. Does this mean that the values of equity, compassion, and mutual respect are not deeply held across American society or that equity in access to valuable health care is not important to the realization of these values?

The Committee concludes that these are not the correct conclusions to draw from our policy inaction at the national level. We believe instead that as a society and as a polity, Americans have failed to recognize just how important equitable access to care and coverage has become in honoring long-held ethical and political commitments. Comprehensive health reform has failed for reasons other than to reject the goal of universal coverage (Vladeck, 2003). The Committee believes that the United States has chronic, endemic uninsurance by default rather than by explicit choice.

CONCLUSION

This report and the work of the Committee on the Consequences of Uninsurance not only provide information about the costs resulting from the lack of coverage and some of the costs and benefits of expanding it to everyone, it also presents us with an ethical dilemma. In light of the information and analyses that the Committee has developed about choices we have not made as a society, as well as those that we have made to invest heavily in health care, we cannot excuse the unfairness and insufficient compassion with which our society deploys its considerable health care resources and expertise. Providing all members of American society with health insurance coverage would contribute to the realization of democratic ideals of equality of opportunity and mutual concern and respect. By tolerating a society in which a significant minority lacks the health care and coverage that most Americans enjoy, we are missing opportunities to become more fully the nation we claim to be.

|

BOX 6.1 Spending on Health Care for Uninsured Americans 3.1 Uninsured children and adults are less likely to incur any health care expenses in a year and, on average, incur health care costs well below half of average health care spending by all those under age 65. 3.2 People who lack health insurance for an entire year have out-of-pocket expenditures comparable to those of people with private coverage, but they also have much lower family incomes. Out-of-pocket spending for health care by the uninsured is more likely to consume a substantial portion of family income than out-of-pocket spending by those with any kind of insurance coverage. 3.3 The total cost of health care services used by individuals who are uninsured for either part of or the entire year is estimated to be $98.9 billion for 2001. 3.4 The best available estimate of the value of uncompensated health care services provided to persons who lack health insurance for some or all of a year is roughly $35 billion annually, about 2.8 percent of total national spending for personal health care services. 3.5 Public subsidies to hospitals amounted to an estimated $23.6 billion in 2001, closely matching the cost of uncompensated services that hospitals reported providing. Overall, public support from the federal, state, and local governments accounts for between 75 and 85 percent of the total value of uncompensated care estimated to be provided to uninsured people each year. 3.6 There is mixed evidence that private payers subsidize uncompensated care. The impact of any such shifting of costs to privately insured patients and insurers is unlikely to be so large as to affect the prices of health care services and insurance premiums. 3.7 The costs of direct provision of health care services to uninsured individuals fall disproportionately on the local communities where they reside. Other Costs Associated with Uninsurance 4.1 The Committee’s best estimate of the aggregate, annualized cost of the diminished health and shorter life spans of Americans who lack health insurance is between $65 and $130 billion for each year of health insurance forgone. These are the benefits that could be realized if extension of coverage reduced the morbidity and mortality of uninsured Americans to the levels for individuals who are comparable on measured characteristics and who have private health insurance. These estimated benefits could be either greater or smaller if unmeasured personal char |

|

acteristics were responsible for part of the measured difference in morbidity and mortality between those with and those without coverage. This estimate does not include spillover losses to society as a whole of the poorer health of the uninsured population. It accounts for the value only to those experiencing poorer health and subsumes the losses to productivity that accrue to uninsured individuals themselves. 4.2 Uninsured individuals and families bear the burden of increased financial risk and uncertainty as a consequence of being uninsured. Although the estimated monetary value of the potential financial losses that those without coverage bear is relatively small (compared to the full cost of their services) because of charity care, the psychological and behavioral implications of living with financial and health risks and uncertainty may be significant. 4.3 Uninsured children are at greater risk than are children with health insurance of suffering delays in development that may affect their achievements and opportunities in later life. 4.4 Public programs, including Medicare, Social Security Disability Insurance, and the criminal justice system almost certainly have higher budgetary (transfer and economic) costs than they would if the U.S. population in its entirety had health insurance up to age 65. It is not possible, however, to estimate the extent to which such program costs are increased as a result of worse health due to lack of health insurance. 4.5 Individual employers who do not currently provide health insurance benefits to their employees are unlikely to be economically worse off, on net, as a result. Any systemic, regional, or national losses of productivity or productive capacity as a result of uninsurance among almost one-fifth of the working-age population cannot be measured with the data now available. 4.6 Not only those who lack coverage, but others in their communities as well, may experience reduced access to and availability of primary care and hospital services resulting from relatively high rates of uninsurance that imperil the financial viability of health care providers and institutions. In addition, population health resources and programs, including disease surveillance, communicable disease control, emergency preparedness, and community immunization levels, have been undermined by the competing demands for public dollars for personal health care services for those without coverage. Additional Costs of Care If Uninsured Gained Coverage 5.1 Estimates of the cost of the additional health care that would be provided to the uninsured once they became insured range from $34 to $69 billion per year, assuming no structural changes in the systems of health care financing or delivery, average scope of benefits, or provider payment. This incremental cost of services amounts to 2.8 to 5.6 percent of national spending for personal health care services in 2001. |

|

Social and Economic Costs in Context Conclusion 1: The estimated benefits in terms of the value of healthy life years gained by providing coverage to those currently uninsured are likely greater than the incremental societal costs of the additional health care services that they would receive if insured. The cost-effectiveness of the additional health care that the uninsured population would use with coverage is comparable to that of many other health-enhancing and life-extending interventions. Conclusion 2: Health insurance contributes essentially to obtaining the kind and quality of health care that can express the equality and dignity of every person. Despite the absence of an explicit Constitutional or statutory right to health care (except for emergency care in hospitals), disparities in access to and the quality of health care of the kind that prevail between insured and uninsured Americans contravene widely accepted democratic cultural and political norms of equal consideration and equal opportunity. |