Introduction

Dale W. Jorgenson

Harvard University

Dr. Jorgenson, Chair of the National Research Council’s Board on Science, Technology, and Economic Policy (STEP), welcomed participants to the day’s workshop on Software Growth and the Future of the U.S. Economy. The program, whose agenda he acknowledged as very ambitious, was the fourth in the Board’s series “Measuring and Sustaining the New Economy.” The series was begun in the midst of a tremendous economic boom, and although conditions had changed, the basic structural factors had not: A new economy has in fact had momentous impact on productivity growth in the United States and around the world, and it is therefore of great importance for economic policy and for the country’s future.1

PRODUCTIVITY AND MOORE’S LAW

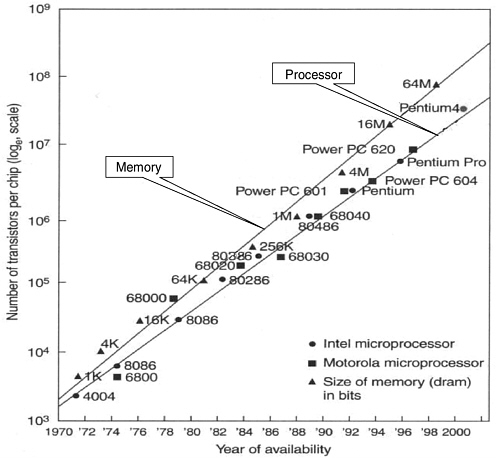

Recapping the series to date, Dr. Jorgenson noted that it began by addressing a hardware phenomenon, the development of semiconductor technology, which he called “the most basic story of the New Economy.” He used a graph to illustrate its driving force: the growth of capacity on memory chips and on logic chips, which are the basic hardware components for computers, and, increasingly, for communications equipment as well (See Figure 1). Translating this technical description into economic terms, he showed a graph of the relative prices of semiconductors from 1977 to 2000 (See Figure 2). Only in the previous 5 years or so had “relatively reasonable” data on semiconductor prices become available in the United States. But as information piled up, price changes for semiconductors were seen to mirror the dramatic developments of technology: Moore’s Law,

FIGURE 1 Transistor density on microprocessors and memory chips.

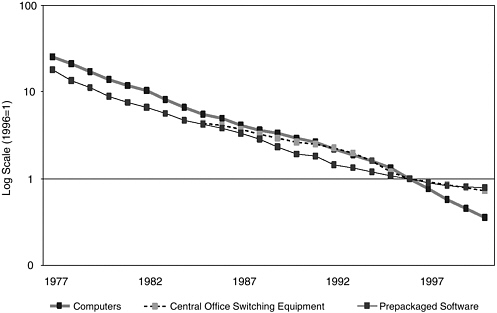

FIGURE 2 Relative prices of computers and semiconductors, 1977-2000.

NOTE: All price indexes are divided by the output price index.

which expresses a doubling of the number of transistors on a chip every 18 to 24 months, was mirrored in the price indexes for semiconductors.

Extending this information to such hardware as computers and communications equipment was the next step. Since 1985, the Bureau of Economic Analysis (BEA) of the U.S. Department of Commerce has maintained price indexes for computers in the national accounts. As a result of this “very satisfactory situation,” economists have a clear idea of the obviously momentous effect that computers have on economic growth. Dr. Jorgenson held up the collaboration that produced these indexes, in which the government has been represented by BEA and the private sector by IBM, as a paradigm for STEP’s program on Measuring and Sustaining the New Economy. He noted that the Board had designed its program to bring together those doing the measuring, who are mainly in government agencies, with those who know the technology, who are mainly in the private sector.

THREE CATEGORIES OF SOFTWARE

Within U.S. national accounts software is broken down into three categories: prepackaged, custom, and own-account. Prepackaged software, although just what

it says—shrink-wrapped—is more commonly purchased with the computer itself; the software or patches to it are also often downloaded from a Web site. Custom software comes from firms like SAP or Oracle that produce large software systems to perform business functions—database management, human-resource management, cost accounting, and so on—and must be customized for the user. Own-account software refers to software systems built for a unique purpose, generally a large project such as managing a weapons system or an airline reservations system.

Dr. Jorgenson noted that quite a bit of price information has been gathered on prepackaged software, but that it makes up only 25 to 30 percent of the software market. Custom and own-account software are not as easy to measure as is shrink-wrapped, something reflected in the fact that price information on both of these components is scarcer than it is on prepackaged software and that no price index exists for either. As a consequence, “there is a large gap in our understanding of the New Economy,” he said, adding that the aim of the day’s workshop was to begin trying to fill this gap in.

A HISTORY OF DECLINING PRICES

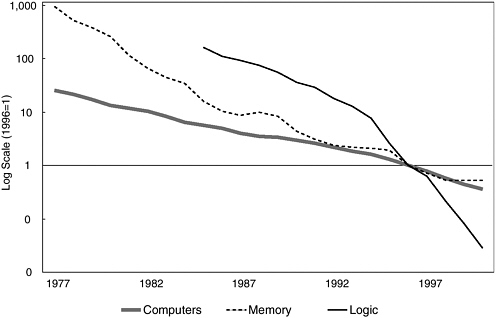

Referring again to the chart, which he dubbed the “gold standard” for measurement issues, Dr. Jorgenson emphasized the tremendous declines in prices that it depicts (See Figure 2). While the chart goes back only as far as 1977, computer prices have declined at about 15 percent per year since the computer’s commercialization. Semiconductor prices have been declining even more rapidly, about 50 percent a year for logic chips and about 40 percent a year for memory chips.

His next chart, based on a historic series constructed by BEA, showed prepackaged software prices declining at rates comparable to those of hardware as represented by computers and by communications equipment; prices of the latter, which relies increasingly on semiconductor technology, have behaved rather similarly to those of computers (See Figure 3). That software improvement, although not based on Moore’s Law, has paralleled hardware’s trend for a long time is “a bit of a mystery,” he said.

Having imparted what he called “the good news,” Dr. Jorgenson promised that William J. Raduchel, next to speak on “The Economics of Software,” would “explain the bad news: that we don’t have a very clear understanding collectively of the economics of software.” Dr. Raduchel, Dr. Jorgenson’s former colleague in economics at Harvard, designed early software for econometrics and model simulation. At this, Dr. Jorgenson remarked, he had such success that he left the academy for high-tech industry and ultimately, through a succession of steps, became chief technology officer of AOL-Time Warner.