1

The Healthcare Imperative

INTRODUCTION

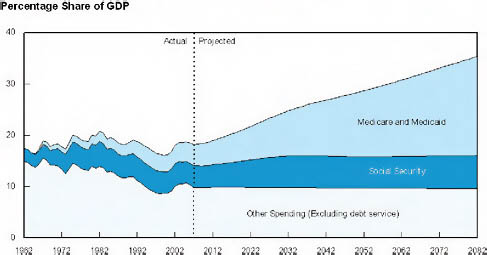

With projected expenditures of $4.4 trillion in 2018, national health spending could potentially grow more than 300 percent over the course of just 18 years (CMS, 2009). According to projections from the Congressional Budget Office (CBO), federal spending on Medicare and Medicaid alone will increase from about 5 percent of GDP in 2009 to more than 6 percent in 2019 and approximately 12 percent by 2050, mostly from growth in per capita costs (Elmendorf, 2009). Research indicates that, if costs per enrollee in Medicare and Medicaid grow at the same rate over the next four decades as they have over the past four, those two programs will increase from 5 percent of GDP today to 20 percent by 2050 (Figure 1-1) (CBO, 2007).

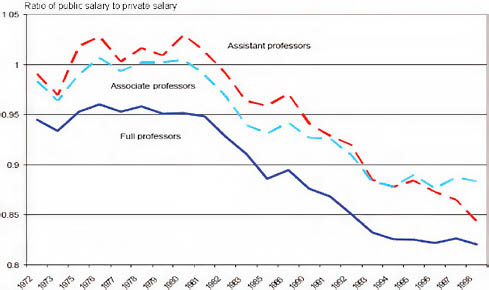

The costs of health care have therefore not just strained the federal budget; they have affected state governments and the private sector as well. In 2008, Medicaid spending accounted for approximately 21 percent of total state spending and represented the single largest component of state spending (National Association of State Budget Officers, 2009). These levels of healthcare expenditures have restricted the ability of state and local governments to fund other priorities, most prominently the needed investments in education (The White House, 2009). Beginning in the early 1980s, as healthcare costs began to rise, salaries began declining at public institutions relative to private institutions at all academic ranks, putting public universities at risk and at clear competitive disadvantage with their private counterparts in faculty recruitment (Figure 1-2) (Kane and Orszag, 2003).

FIGURE 1-1 Long-term fiscal gap and health care costs.

SOURCE: CBO, 2007.

In the private sector, healthcare costs have contributed to slowing the growth in wages and jobs (National Coalition on Health Care, 2008). While health insurance prices rapidly escalate and employers cut back on the provision of health insurance benefits (Kaiser Family Foundation, 2009b), the number of uninsured rose from 45.7 million in 2007 to 46.3 million in 2008 (U.S. Census Bureau, 2009).

FIGURE 1-2 Ratio of public to private research university salaries.

SOURCE: Kane and Orszag, 2003.

On the individual level, the average cost of annual health insurance premiums for a family of four exceeded $13,000 in 2009, growing 5 percent in just a single year (Kaiser Family Foundation, 2009a). Health insurance premium increases have consistently exceeded inflation and the growth in worker’s wages, forcing individuals to spend increasing amounts of their income simply to maintain health coverage (Kaiser Family Foundation, 2009b). Estimates of the real increase in per capita income devoted to health spending over the next 8 decades have been calculated to be almost 120 percent (Chernew et al., 2009). Fifty-three percent of Americans said their family limited their medical care in the past 12 months because of cost concerns, 19 percent reported serious financial problems due to medical bills, with 13 percent depleting all or most of their savings and 7 percent unable to pay for basic necessities such as food, heat, or housing (Kaiser Family Foundation, 2009b).

While the United States has the highest per capita spending on health care of any industrialized nation—50 percent greater than the second highest and twice as high as the average for Europe (Peterson and Burton, 2008), it continually lags behind other nations on many healthcare outcomes, including life expectancy and infant mortality (Anderson and Frogner, 2008; Docteur and Berenson, 2009). Employers and employees in other industrialized countries spend about 63 percent of what the United States spends on health care, but U.S. workforce health trails by about 10 percent. Indeed, the emerging economies of Brazil, India, and China rank behind the United States by about 5 percent on workforce health measures, but these countries spend only a fraction—about 15 percent—of what the United States spends on health care (Milstein, 2009). The relatively poor performance in health outcomes relative to investment suggests ample opportunity for improvement on both costs and outcomes. This prospect is supported by findings that high-spending areas in the United States—spending $6,304 per capita compared to $3,922 per capita in the lowest spending quintile in 1996—utilize 60 percent more frequent physician and hospital visits, testing, and use of procedures yet achieve no quality advantage (Fisher et al., 2003). Together, these findings underscore the opportunities to lower costs without impacting clinical outcomes.

The necessity of bending the cost curve stimulated the Institute of Medicine’s (IOM’s) Roundtable on Value & Science-Driven Health Care to partner with the Peter G. Peterson Foundation, a private philanthropy dedicated to the nation’s fiscal security, in the conduct of a workshop series The Healthcare Imperative: Lowering Costs and Improving Outcomes, part of the Learning Health System series, in 2009. Guided by an IOM Planning Committee, the meetings were aimed at engaging participants in specifically exploring, identifying, and characterizing the major causes of excess healthcare spending, waste, and inefficiency in the United States; considering the strategies that might reduce per capita health spending in the United

States while improving health outcomes; and exploring the policy options relevant to the effective implementation of those strategies. The chapters in this book highlight common themes from the discussions and provide summaries of the presentations from a variety of perspectives.

PROMOTING EFFICIENCY AND REDUCING DISPARITIES IN HEALTH CARE

Peter R. Orszag, M.Sc., Ph.D.

Office of Management and Budget

Rising healthcare costs are not only a critical issue for employers and for both enrollees and patients who ultimately bear the costs of health insurance and health care, they also constitute the nation’s central fiscal challenge.

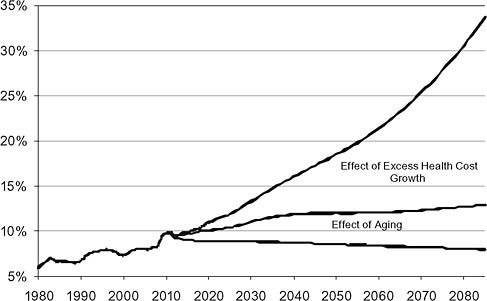

On our current trajectory, Medicare and Medicaid will double as a share of spending on federal programs within the next 30 years (OMB, 2009). And, while the aging of the population also contributes to this rise in spending, healthcare cost growth is the primary driver over the long term (see Figure 1-3). In fact, slowing the rate of healthcare cost growth by just 0.15 percentage points per year would produce the same amount of sav-

FIGURE 1-3 Sources of Projected Growth in Medicare, Medicaid and Social Security (Spending, % OF GDP).

SOURCE: OMB, 2009.

ings for the federal budget as closing the 75-year Social Security shortfall (OMB, 2009).

Put simply, if we do not act to address rising healthcare costs, anything else we do to reduce long-term federal deficits will be for naught.

Crowding Out Key Investments

While rising healthcare costs are projected to drive the federal budget toward fiscal insolvency over the long term, they also threaten to crowd out key governmental investments. State funding for higher education provides a striking example of this crowd-out effect.

Over the past several decades, state support for higher education has steadily declined. State appropriations for higher education fell from an average of roughly $8.50 per $1,000 in personal income in 1977, to an average of about $7 per $1,000 in personal income in 2002—a drop of nearly 20 percent (Kane et al., 2003). It is notable that, as this drop-off has occurred, salaries for professors in public institutions have declined steadily relative to salaries for professors in private institutions. Whereas, prior to 1980, salaries were largely comparable for professors in public and private institutions of higher education, the public/private ratio of average salaries fell to roughly 0.85 for professors by 1998 (Kane et al., 2003). Although this is only one metric, it is indicative of the strain placed on public investments.

While state investment in higher education has been declining relative to income, state spending on health care has been rising—driven by the Medicaid program, the costs of which are shared by both the federal and state governments. These are complementary trends. Research shows that, having controlled for other factors, higher education appropriations per capita are negatively related to Medicaid spending per capita. In particular, a $1 increase in real state Medicaid spending per capita is linked to a real reduction in higher-education appropriations per capita by about $.06 or $.07—a relationship that could potentially explain the vast majority of the decrease in real, higher-education spending per capita from the 1980s through the 1990s (Kane et al., 2003). Growing health costs, thus, not only threaten to hinder future economic growth by creating gaping federal budget deficits, but also by crowding key investments—such as in educa-tion—that are needed to lay a foundation for future prosperity.

Gap Between Cost and Quality

Even as we spend more on health care, we are not necessarily seeing a commensurate increase in quality. In fact, there is strong evidence that our healthcare system is riddled with inefficiency—meaning, quite simply, that we are not getting our money’s worth.

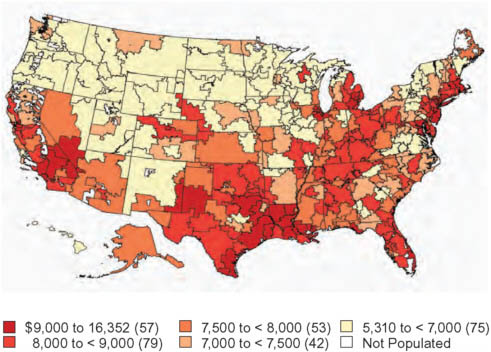

Perhaps the most compelling evidence of this inefficiency is the wide variation in healthcare spending per capita across the United States. Figure 1-4 shows this variation in spending per person specifically within the Medicare system by hospital referral region, adjusting for age, sex, and race. Furthermore, this very substantial variation in cost per beneficiary in Medicare is not correlated with overall health outcomes—and, in fact, the opposite may be the case (Orszag, 2008).

Based on this evidence, researchers have found that as much as 30 percent of Medicare’s costs could be saved without negatively affecting health outcomes if spending in high- and medium-cost areas could be reduced to the level in low-cost regions—and those estimates could probably be extrapolated to the healthcare system as a whole (Fisher, 2005; McGinnis, 2009; McKinsey Global Institute, 2007; Wennberg et al., 2002). This means that hundreds of billions of dollars per year in healthcare spending in the United States is not making people better off. Rather, these dollars are simply wasted.

Embedded in this troubling conclusion is a substantial opportunity: the possibility to reduce healthcare costs without adversely affecting health outcomes. This is one of the keys to healthcare reform—transforming

FIGURE 1-4 Medicare Spending per Capita (by Hospital Referral Region).

SOURCE: Reprinted with permission from Dartmouth Atlas of Health Care.

the healthcare system into one that emphasizes quality rather than just quantity.

Rising Inequality in Life Expectancy

As we consider how to restrain the growth of healthcare costs, it is also important to keep in mind another disturbing trend: recent gains in life expectancy have not been shared equally across socioeconomic groups. Life expectancy in the United States has been steadily increasing for the past several decades, and the gaps between women and men and between whites and African Americans have narrowed somewhat. But differences in life expectancy by educational attainment and income have been growing. In other words, socioeconomic status has become an increasingly important determinant of life expectancy, whether measured at birth or at age 65 (CBO, 2008).

Reducing this disparity in life expectancy should involve both addressing the greater incidence of unhealthy behaviors among those with lower incomes and educational attainment—such as with regard to smoking and nutrition—and a lack of access to quality medical care. These are two independent factors.

********

Since I addressed the Institute of Medicine last May, the President worked with Congress to enact comprehensive health insurance reform. Much has and will be written about health insurance reform. But, in short, this reform addresses many of the problems that I identified in my speech last May.

Health reform uses the best available knowledge and most promising ideas from across the political spectrum to control healthcare costs by transforming the health system from one that delivers greater quality with less quantity. It does so by, among other changes:

-

Imposing an excise tax on the highest-cost insurance plans, providing employers with an incentive to seek higher-quality and lower-cost health benefits;

-

Reforming incentives to improve the way health care is delivered to patients throughout the country through such mechanisms as bundled payments and accountable-care organizations; and

-

Creating an Independent Payment Advisory Board in Medicare so that reforming the healthcare system is not a one-time event but an ongoing process with the goal of improving care and lowering costs.

This represents the first serious piece of legislation to address the forces underlying rising healthcare costs—and it does so while giving more choice and security to those with health insurance, providing access to coverage to those without, improving the quality of health care for all, and generating the most deficit reduction of any legislation in over a decade.

WHY AMERICANS SPEND MORE FOR HEALTH CARE

Eric Jensen, M.B.A, and Lenny Mendonca, M.B.A.

McKinsey Global Institute

In 2006, the United States spent $2.1 trillion on health care, more than twice what the nation spent on food, and more than China’s citizens consumed on all goods and services. With growth in healthcare costs continually exceeding growth of the gross domestic product (GDP), it begs the question: are we receiving commensurate value for the money that is spent? The McKinsey Global Institute published an updated report in December 2008 addressing this question by comparing healthcare costs in the United States to some of our peer members of the Organisation for Economic Cooperation and Development (OECD), a multinational association with one of the world’s largest and most reliable sources of comparable economic and social data. This paper summarizes some of the main findings in this published update. By providing a comprehensive analysis of U.S. healthcare costs and pinpointing where spending is above expected, our objective is to make a constructive contribution to public debate and decision making on issues related to the U.S. health system.

Comparison of Healthcare Spending in the United States and Internationally

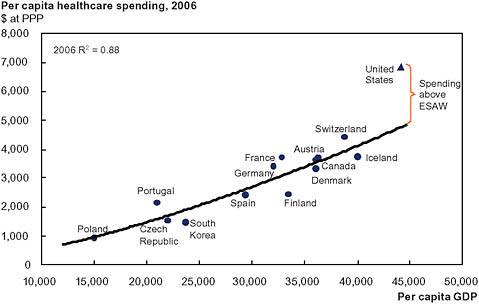

To identify the extent of spending above expected, we looked at healthcare spending on a per capita basis as a function of GDP per capita. As seen in Figure 1-5, wealth is an incredibly powerful predictor of healthcare spending for most OECD countries. The notable exception is healthcare spending in the United States, which is far off the expected regression line.

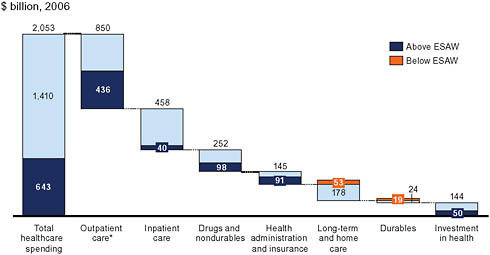

We then evaluated the gap between “estimated spending according to wealth” (ESAW) and actual spending for each component of the health system. In doing so, we found that the United States spent nearly $643 billion more than expected in 2006 given U.S. wealth levels. As seen in Figure 1-6, outpatient care, the largest and fastest-growing cost category, accounts for $436 billion, or two-thirds of spending above expected. Four other cost categories—drugs, health administration and insurance, investment in health, and inpatient care—are responsible for $279 billion in spending

FIGURE 1-5 The U.S. spending on health care compared to other countries, adjusted for relative wealth.

NOTE: ESAW = estimated spending according to wealth; PPP = purchasing power parity.

SOURCE: Reprinted with permission from the McKinsey Global Institute.

FIGURE 1-6 Spending gap between the U.S. and other OECD countries.

NOTE: ESAW = estimated spending according to wealth.

*Outpatient care includes physician and dentist offices, same-day visits to hospitals including emergency departments, ambulatory surgery and diagnostic imaging centers, and other same-day care facilities.

SOURCE: Reprinted with permission from the McKinsey Global Institute.

above expected. In the remaining two categories of long-term and home care, and durable medical equipment, U.S. spending was $72 billion less than expected.

Outpatient Care Cost Drivers

Outpatient care, which includes same-day hospital and physician office visits, was by far the largest and fastest-growing part of the U.S. healthcare system. Part of this growth has been driven by a structural shift in care delivery away from inpatient settings to outpatient settings—the United States now delivers 65 percent of care in an outpatient setting versus an OECD average of 52 percent. Theoretically this shift might save costs, because supporting fixed costs tend to be lower for outpatient care than when patients stay overnight in a hospital. Indeed, we estimated that the United States saves $100 billion to $120 billion a year on inpatient costs from shorter lengths of stay and fewer admissions. However, these savings only partly defray the $436 billion in outpatient care costs above expected, suggesting that this structural shift has increased—not decreased—total costs as a consequence of increases in consumption of healthcare services.

What underlies higher outpatient care costs and use? We identified five drivers, including (1) the highly profitable nature of outpatient care; (2) the judgment-based nature of physician care coupled with the fee-for-service nature of reimbursement; (3) unit price growth linked to technological innovation; (4) demand growth linked to greater availability of supply; and (5) relatively price-insensitive patients with limited out-of-pocket costs.

Inpatient Care Cost Drivers

As noted above, there has been a structural shift in the United States away from inpatient care, and so the above-expected spending in this category was relatively modest. The United States has shorter lengths of stay and fewer admissions than many of its OECD peers. However, the United States paid far more for each patient bed day than peer countries. Higher costs per patient bed day were driven by lower patient-to-nurse ratios, higher nursing salaries, higher supply costs, and higher hospital fixed costs.

Of note, the United States also performed more surgical procedures than OECD peer countries at 90 procedures per 1,000 population versus an OECD average of 71. Higher volumes for four procedures—percutaneous coronary intervention, coronary bypass, cardiac catheterization, and knee replacement—alone accounted for an estimated $21 billion in additional inpatient care costs.

Prescription Drug Cost Drivers

Higher U.S. drug spending was a result of lower usage rates coupled with higher prices and a more expensive drug mix. On a standard unit basis, the United States used 10 percent fewer drugs per capita than OECD peers. For equivalent drugs, prices were on average 50 percent higher in the United States than those in other OECD countries. Drug type matters in this analysis: the United States spent 77 percent more for branded drugs, 35 percent more for biologics, and 11 percent less for generics than peer countries. Maybe most important, however, is the mix of drugs used by Americans. When we factor in the effect of drug mix, the United States spent over 118 percent more for an “average” pill than peer OECD countries despite the fact that the United States used more generics.

Health Administration and Insurance Cost Drivers

Breaking down sources of above-expected spending, we found that $63 billion was attributable to private payers: $30 billion in the form of profits and tax, and $33 billion in selling, general, and administrative expenses. Public administration expenses for Medicare, Medicaid, and other programs accounted for the remaining $28 billion in U.S. spending above expected.

These higher costs were partly attributable to the diversity and number of payers as well as the multistate regulation of the U.S. healthcare system. Its structure creates additional costs and inefficiencies: redundant marketing, underwriting, claims processing, and management overhead. In other OECD countries, which have less-fragmented payment systems, these costs are much lower. Interestingly, we found that given the structure of the U.S. system, its administrative costs were actually $19 billion less than expected, suggesting that payers have had some success in restraining costs.

Exploration of Alternative Cost Drivers

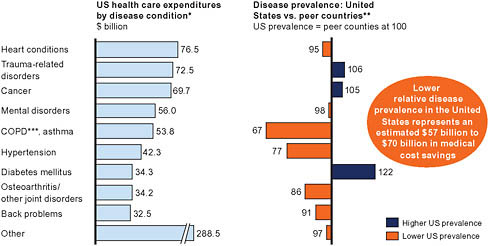

Among alternative explanations for higher healthcare costs in the United States, two bear further investigation: (1) Americans are sicker than people in other OECD countries, and (2) Americans obtain more value from the health system.

In exploring the hypothesis that Americans are sicker than people in other OECD countries, we did not find this to be true. As demonstrated in Figure 1-7, the United States had lower prevalence along most of the health conditions listed. There were notable exceptions, such as diabetes and cancer, but generally the United States was in fact healthier than its

FIGURE 1-7 U.S. disease prevalence compared to peer countries.

aIncludes 35 or 60 medical conditions surveyed by the U.S. Medical Expenditure Panel Survey; the costs of these diseases represent 35 percent of total U.S. health expenditures.

bPeer countries are France, Germany, Italy, Spain, and the United Kingdom.

cChronic obstructive pulmonary disease.

SOURCE: Reprinted with permission from the McKinsey Global Institute.

OECD peers. This counterintuitive finding could be explained by the fact that (1) disease prevalence, particularly that of chronic disease, is growing globally and not just in the United States; (2) the younger U.S. population offset relatively higher prevalence of certain conditions in at-risk populations (such as heart disease for the over-30 population); and (3) Americans smoke far less than OECD peers and, as a consequence, have lower healthcare costs for related conditions.

On the question of whether Americans obtain more value from the health system, the evidence was mixed. Parts of the U.S. healthcare system, such as its best hospitals, are clearly world-class. Cutting-edge drugs and treatments are available earlier and waiting times to see a physician tend to be lower. Yet the United States lags behind other OECD countries on outcome measures including life expectancy and infant mortality. Furthermore, access to health care is unequal; more than 45 million Americans are uninsured.

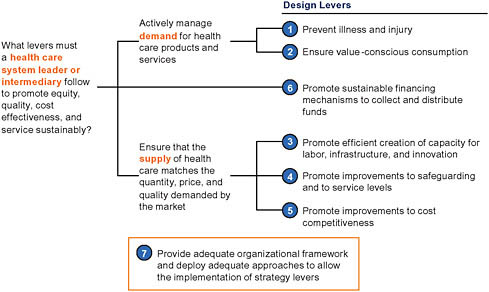

Framework for Reform Options

The drivers of high and rising costs are widespread within the U.S. healthcare system, and if they are not addressed in broad terms, healthcare spending growth is likely to continue unabated. Indeed, the Department

FIGURE 1-8 Framework for health reform.

SOURCE: Reprinted with permission from the McKinsey Global Institute.

of Health and Human Services projects that health spending will reach $4.3 trillion within the next 10 years.

As U.S. policy makers look at options for healthcare reform, they must consider action that addresses both supply and demand, focuses on the financing of health care, and ensures that any reform takes place within an effective organizational framework for implementation to be effective (Figure 1-8). And if the healthcare cost trajectory is going to bend, a focus on outpatient care spending is essential to that effort.

REFERENCES

Anderson, G. F., and B. K. Frogner. 2008. Health spending in OECD countries: Obtaining value per dollar. Health Affairs (Millwood) 27(6):1718-1727.

Chernew, M. E., R. A. Hirth, et al. 2009. Increased spending on health care: Long-term implications for the nation. Health Affairs (Millwood) 28(5):1253-1255.

CMS (Centers for Medicare & Medicaid Services). 2009. National health expenditure data overview. http://www.cms.hhs.gov/nationalhealthexpenddata/01_overview.asp (accessed June 1, 2009).

CBO (Congressional Budget Office). 2007. The Long-Term Budget Outlook. http://www.cbo.gov/ftpdocs/88xx/doc8877/12-13-LTBO.pdf (accessed March 1, 2010).

——. 2008. Growing Disparities in Life Expectancy (2008). http://www.cbo.gov/ftpdocs/91xx/doc9104/04-17-LifeExpectancy_Brief.pdf (accessed April 5, 2010).

Docteur, E., and R. Berenson. 2009. How does the quality of U.S. health care system compare internationally? http://www.urban.org/UploadedPDF/411947_ushealthcare_quality.pdf (accessed October 2, 2009).

Elmendorf, D. W. 2009. Options for controlling the cost and increasing the efficiency of health care. http://www.cbo.gov/ftpdocs/99xx/doc9911/02-25-Health_Insurance.pdf (accessed September 4, 2009).

Fisher, Elliott S., et al. 2003. The Implications of Regional Variations in Medicare Spending. Part 1: The Content, Quality, and Accessibility of Care. Annals of Internal Medicine, vol. 138, no. 4 (February 18):273-287.

Fisher, E. 2005. More Care Is Not Better Care. Expert Voices. National Institutes for Health Care Management. Issue 7: January 2005. http://www.nihcm.org/~nihcmor/pdf/ExpertV7.pdf (accessed April 4, 2010).

Kaiser Family Foundation. 2009a. Health care cost: A primer. http://www.kff.org/insurance/upload/7670_02.pdf (accessed September 7, 2009).

——. 2009b. Kaiser health tracking poll. http://www.kff.org/kaiserpolls/posr022509pkg.cfm (accessed September 7, 2009).

Kane, T. J., and P. R. Orszag. September 2003. “Funding Restrictions at Public Universities: Effects and Policy Implications.” Brookings Institution. Working Paper. http://www.brookings.edu/views/papers/orszag/20030910.pdf (accessed March 1, 2010).

Kane, T. J., P. R. Orszag, and D. Gunter. 2003. State Fiscal Constraints and Higher Education Spending. Discussion Paper 11. Urban-Brookings Tax Policy Center. http://www.taxpolicycenter.org/UploadedPDF/310787_TPC_DP11.pdf (accessed April 4, 2010).

McGinnis, J. M. 2009 (May 21). Opening remarks. The Healthcare Imperative: Lowering Costs, Improving Outcomes, Understanding the Targets, an Institute of Medicine Workshop.

McKinsey Global Institute. 2007. Accounting for the Cost of Health Care in the United States. McKinsey & Company. http://www.mckinsey.com/mgi/reports/pdfs/healthcare/MGI_US_HC_fullreport.pdf (accessed April 3, 2010).

Milstein, A. 2009. Tracking the Contribution of U.S. Health Care to the Global Competitiveness of American Employers and Workers. 2009 Business Roundtable Health Care Value Comparability Study. http://select.mercer.com/blurb/145847/article/20096311 (accessed August 7, 2009).

National Association of State Budget Officers. 2009. Fiscal survey of states. http://www.nasbo.org/Publications/PDFs/FSSpring2009.pdf/ (accessed September 7, 2009).

National Coalition on Health Care. 2008. The impact of rising health care costs on the economy: Effect on business operations. Washington, DC: National Coalition on Health Care.

OMB (Office of Management and Budget). 2009. Mid-Session Review: Budget of the U.S. Government—Fiscal Year 2010. Washington, DC: Office of Management and Budget.

Orszag, P. R. 2008. Increasing the Value of Federal Health Spending: Statement Before the Committee on Budget, U.S. House of Representatives. http://www.cbo.gov/ftpdocs/95xx/doc9563/07-16-HealthReform.pdf (accessed April 5, 2010).

——. 2010. Testimony of Peter R. Orszag, Director of the Office of Management and Budget, Before the Committee on the Budget, United States Senate. http://budget.senate.gov/republican/hearingarchive/testimonies/2010/2010-02-02Orszag.pdf (accessed April 5, 2010).

Peterson, C., and R. Burton. 2008. U.S. health care spending: Comparison with other OECD countries. http://digitalcommons.ilr.cornell.edu/key workplace/311 (accessed September 11, 2009).

U.S. Census Bureau. 2009. Income, poverty and health insurance coverage in the United States. http://www.census.gov/Press-Release/www/releases/archives/income_wealth/014227.html (accessed October 1, 2009).

The White House. 2009. Fiscal Responsibility Summit. http://www.whitehouse.gov/assets/blog/Fiscal_Responsibility_Summit_Report.pdf (accessed September 4, 2009).

Wennberg, J. E., E. Fisher, and J. Skinner. 2002. Geography and the Debate Over Medicare, Health Affairs, Feb. 13 Web exclusive. http://content.healthaffairs.org/cgi/reprint/hlthaff.w2.96v1 (accessed April 4, 2010).