Overview and Summary of America’s Energy Future: Technology and Transformation

Energy has long played a critical role in our nation’s national security, economic prosperity, and environmental quality, and today concerns about how the United States produces and consumes energy are at the forefront of public attention. Political instability in primary energy-producing regions around the world, rapidly rising global demand for energy, especially in developing countries, and a growing awareness of the impact of fossil fuel use on global climate change have contributed to a new sense of urgency about the role of energy in ensuring security and U.S. well-being in the 21st century. Awareness is steadily growing that the United States must fundamentally transform the ways in which it produces, distributes, and consumes energy. Understanding and deciding exactly how and at what rate U.S. energy use and sources of energy supply should or will change have become among the most difficult and complex challenges of our time.

For more than three decades, America’s capacity for technological innovation has been a cornerstone of national strategies for dealing with energy policy issues. Now a renewed sense of urgency has raised the stakes and the scale of the challenge. Although new technology alone is unlikely to be sufficient to meet the nation’s energy challenges, developments in science and technology will substantially affect our ability to shape future energy options. New energy technologies hold considerable promise for enabling more-efficient energy use; for providing cleaner energy and safer, more-efficient recovery and use of traditional sources of supplies such as oil, coal, and natural gas; and for leading to a post–fossil fuel era of more secure and environmentally benign energy sources.

Despite the promise of new technology, however, the transformation of traditional patterns of energy supply and use is inevitably complicated—by the close interconnections of energy supply and use with economic interests nationally and in various regions; by the relative cost-effectiveness of new technologies; by the extent of disruption that might be caused to major stakeholders, both domestically and abroad, from the emergence of new resources and technologies; and by the broad scale and scope of the work of reducing greenhouse gas emissions while maintaining access to affordable energy. Some of these challenges are not new for the United States, but the urgency of addressing all of them simultaneously is unprecedented.

America’s Energy Future: Technology and Transformation,1 a report prepared by the Committee on America’s Energy Future (the AEF Committee) and published in 2009, explores potential technology pathways for fundamentally transforming U.S. patterns of energy supply and demand. The result of a project initiated in 2007 by the National Academy of Sciences and the National Academy of Engineering, the 700-page volume—the lead report in the America’s Energy Future (AEF) series—focuses on technologies that exist now or that should be ready in the near future and could be deployed extensively to bring about fundamental improvements in the U.S. energy enterprise. That report assesses the readiness of technologies for use, estimates how quickly over time they might be deployed, and outlines potential costs as well as barriers to and ultimate impacts of their adoption. It thus provides a technology assessment as a foundation for ongoing work by policy analysts.

This Overview and Summary highlights key findings presented and major topics discussed in America’s Energy Future: Technology and Transformation and also reflects results presented in three reports prepared by three separate study panels appointed, along with the AEF Committee, to carry out the AEF project. The three panel reports in the AEF series include the following:

-

Electricity from Renewable Resources: Status, Prospects, and Impediments;

-

Liquid Transportation Fuels from Coal and Biomass: Technological Status, Costs, and Environmental Impacts; and

-

Real Prospects for Energy Efficiency in the United States.2

In preparing the reports in the AEF series, the AEF Committee and the study panels used the vast existing energy-related literature and conducted additional analysis to help fill gaps and resolve or address conflicting conclusions. The AEF reports compare estimated results of an accelerated effort to phase in prospective technologies from now until 2035 against “business-as-usual” reference scenarios prepared by the U.S. Energy Information Administration (EIA).3 The reports do not forecast or judge which technologies or combinations of technologies will or should be implemented. They also do not consider the substantial energy savings that could be achieved through behavioral or lifestyle changes that might occur, nor do they recommend specific policy actions. Rather, the AEF series focuses on the potential benefits from deployment of currently available and emerging technology options that can contribute to meeting pressing U.S. energy challenges through 2035.

Key findings from America’s Energy Future: Technology and Transformation are summarized in the section below. An overview is then presented of the following topics: energy use in America; the nation’s energy efficiency potential; energy-supply options, including electricity from renewable resources, nuclear energy, and fossil fuel energy; future electricity generation costs and the development of transmission and distribution infrastructure; and alternative liquid transportation fuels.

Unless indicated otherwise, statistics cited and tables and figures included in this overview and summary are documented in America’s Energy Future: Technology and Transformation and in the other reports in the AEF series.

SUMMARY OF KEY FINDINGS

The AEF Committee concluded that with a sustained national commitment, the United States could obtain substantial energy efficiency improvements, develop new sources of energy, and realize reductions in greenhouse gas emissions through the accelerated deployment of existing and emerging technologies in a diverse-portfolio approach to help meet the nation’s energy challenges. However, mobilization of the public and private sectors, supported by sustained long-term policies and investments, will be required for the decades-long effort to develop, demonstrate, and deploy these technologies. Actions taken between now and 2020 to develop and demonstrate several key technologies will also largely determine the options available for many decades to come. It is imperative that the development and demonstration of key technologies be started very soon, even though some will be expensive, not all will be successful, and some may be overtaken by better technologies. Additional AEF study findings include the following:

-

Energy efficiency potential. The deployment of existing energy efficiency technologies is the nearest-term and lowest-cost option for moderating the U.S. consumption of energy, especially over the next decade. In fact, the full deployment of cost-effective energy efficiency technologies in buildings alone could eliminate the need to construct any new electricity-generating plants in the United States except to address regional supply imbalances, replace obsolete power generation assets, or substitute more environmentally benign sources of electricity. Accelerated deployment of these technologies in the buildings, transportation, and industrial sectors could reduce energy use in 2020 by about 15 percent (15–17 quads),4 relative to current projections, and by about 30 percent (32–35 quads) in 2030.

-

Electricity supply options. The United States has many promising options for obtaining new supplies of electricity and changing its supply mix during the next two to three decades, especially if renewable-

-

electric-power technologies, carbon capture and storage (CCS), and evolutionary nuclear technologies can be deployed at sufficient scale. Renewable energy sources could provide an estimated additional 500 terawatt-hours (TWh) of electricity per year by 2020 beyond current production of electricity from renewable energy sources and about an additional 1100 TWh per year by 2035. Coal-fired plants with CSS could provide as much as 1200 TWh of electricity per year by 2035 through repowering and retrofits of existing plants, and as much as 1800 TWh per year by 2035 through the construction of new plants. In combination, the entire existing inventory of coal-fired power plants could be replaced by CCS coal power by 2035. If current plants were modified to increase their power output and new plants were constructed, nuclear plants could provide an additional 160 TWh of electricity per year by 2020, and up to 850 TWh by 2035. The generation of electricity from natural gas could be expanded to meet a substantial portion of U.S. electricity demand by 2035. The deployment of any new supply technologies is very likely to result in higher consumer prices for electricity.

-

Modernizing the nation’s power grid. Expansion and modernization of the nation’s power grid—the electric power transmission and distribution systems—are urgently needed. This would cost (in 2007 dollars) $175 billion and $50 billion respectively for concurrent expansion and modernization of the transmission system, and $470 billion and $170 billion respectively for concurrent expansion and modernization of the distribution system.

-

Continued dependence on oil. Petroleum will continue to be an indispensable transportation fuel through at least 2035. Maintaining current rates of domestic petroleum production (about 5.1 million barrels per day in 2007) will be challenging. Despite limited options for replacing petroleum or reducing its use before 2020, more substantial longer-term options—including improved vehicle efficiency, use of biomass and coal-to-liquid fuels, and increased use of electric or hybrid-electric vehicles—could begin to make significant contributions in the 2030–2035 timeframe.

-

Reduction of greenhouse gas emissions. Substantial reductions in greenhouse gas emissions from the electricity sector are achievable over the next two to three decades. Displacing a significant proportion of

-

petroleum as a transportation fuel to achieve substantial greenhouse gas reductions will require a mixed strategy involving the widespread deployment of energy efficiency technologies, alternative liquid fuels with low carbon dioxide (CO2) emissions, and technologies for electrification of light-duty vehicles.

-

Technology research, development, and demonstration. Although there are technologies that can increase energy efficiency and supply new energy for the next decade, research and development (R&D) are needed to fill the pipeline with new technologies to be implemented after 2020. To meet this need, both the public and the private sectors will need to perform extensive research, development, and demonstration over the next decade.

-

Barriers to accelerated deployment. Formidable barriers could delay or even prevent the accelerated deployment of the energy-supply and end-use technologies described in this overview and summary and in the AEF series of reports. Examples of such barriers include the level of investment that will be required for widespread technology deployment, the low turnover rate of the energy system’s capital-intensive infrastructure, or the lack of energy efficiency standards for many products. Policy and regulatory actions, as well as other incentives, will be required to overcome these barriers.

ENERGY USE IN AMERICA

America’s energy system evolved over the past century in response to rapidly growing demand for energy, advances in technology, diverse public policies and regulations, and powerful market forces integral to economic growth and globalization. That system is currently a vast and complex set of interlocking technologies for the production, distribution, and use of fuels and electricity (Figure 1). As a result, the U.S. energy system’s technologies and production assets are of many different vintages and often rely on aging and increasingly vulnerable infrastructure.

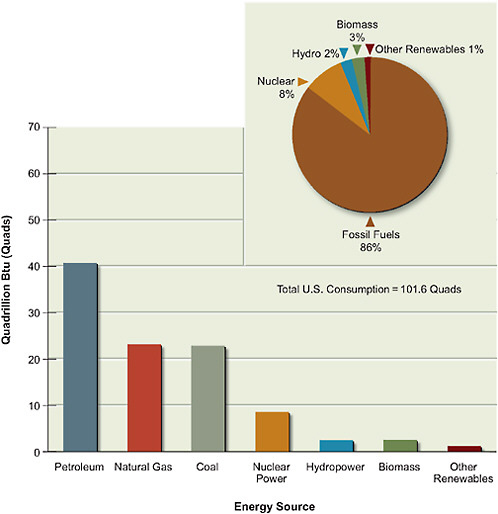

In the United States, cheap and readily available energy obtained from the burning of fossil fuels has driven economic prosperity since the end of the 19th century. Today, fossil fuels produce 85 percent of America’s energy. Coal and

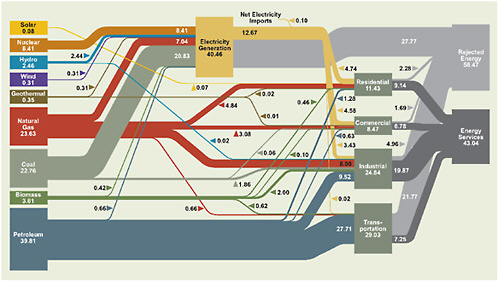

FIGURE 1 Delivery of energy (in quads) in the United States: Shown on the left are the primary fuel sources of energy delivered in the United States in 2007; on the right, the figure shows how that energy was distributed throughout the economy for use in the residential, commercial, industrial, and transportation sectors.

natural gas provide almost 75 percent of electricity, and petroleum fuels 95 percent of transportation (Figures 1 and 2). However, the burning of fossil fuels has a number of deleterious environmental impacts, among the most serious of which is the emission of greenhouse gases, primarily CO2. At present, the United States emits about 6 billion metric tons of CO2 per year into the atmosphere.

Despite decades of declining energy consumption per dollar of gross domestic product, the United States still has a higher per capita consumption of energy than either the European Union or Japan. And, despite improvements in energy efficiency the United States remains the world’s largest energy consumer by a wide margin, and its dependence on energy imports continues to rise. The United States is almost completely dependent on petroleum for transportation—a situation that entails unique energy-security challenges. The nation relies on coal, nuclear energy, renewable energy (primarily hydropower), and, more recently, natural gas for generating its electricity.

At the same time, U.S. domestic oil and gas reserves are being depleted;5 aging but currently operating nuclear plants were constructed largely in the 1970s and 1980s, and many coal-fired plants are even older; electrical transmission and distribution systems depend on infrastructure and technologies built in the 1950s. Renewing or replacing these assets will take decades and require investments totaling several trillion dollars.

There is growing recognition that the U.S. energy system as currently configured is unsustainable over the long run. World competition for fossil fuels continues to grow unabated. Prices of fossil fuels have been volatile; over the past 2 years, petroleum has ranged from $32 to $147 a barrel, and natural gas from $4 to $13 per thousand cubic feet. Concerns continue to mount with respect to the environmental impacts of burning fossil fuels, particularly their emission of greenhouse gases and influence on climate change. As noted earlier, the United States annually produces more than 6 billion metric tons of CO2, a major greenhouse gas. And economists have predicted that if the country continues “business as usual,” its dependence on fossil fuels will continue to grow.

The AEF Committee concluded that with a sustained national commitment, the United States can develop and deploy a portfolio of existing and emerging energy technologies at an accelerated pace. These efforts could result in substantial energy efficiency improvements, new sources of energy, and reductions in greenhouse gas emissions. Over the next 25 years, the technical potential of efficiency and of new sources of energy could substantially decarbonize the electricity sector. Over the same time period, the prospects in the transportation sector as a result of increased energy efficiency and use of alternative fuels are more limited but nonetheless substantial.

In the near term, energy efficiency is the lowest-cost option for reducing U.S. consumption of energy, especially over the next decade. In the future, a variety of

TABLE 1 U.S. Electricity Generation: Current Fuel Sources and New Options for 2020 and 2035 (in terawatt-hours)

options for electricity generation will be available and could potentially replace all coal-fired power plants lacking carbon capture and storage (Table 1).

Achieving substantial reductions in CO2 emissions from the electricity sector is likely to require an approach involving the accelerated deployment of multiple technologies enabling improved energy efficiency, the accelerated deployment of renewable sources of energy, new technologies for the burning of coal and natural gas with CCS, and the installation of evolutionary nuclear technologies. To enable this portfolio approach in the electricity sector, the viability of two key technologies must be demonstrated during the next decade to allow for their widespread deployment starting around 2020:

-

It must be demonstrated whether CCS technologies for sequestering the carbon produced during the generation of electricity from coal and natural gas are technically and commercially viable for application to both existing and new power plants. Construction will be required before 2020 of a suite (approximately 15–20) of retrofit and new demonstration plants with CCS featuring a variety of feedstocks, generation technologies, carbon capture strategies, and geologic storage locations.

-

It must be demonstrated, by constructing a suite of about five plants during the next decade, whether evolutionary nuclear plants are commercially viable in the United States.

A failure to demonstrate the viability of these two key technologies during the next decade would greatly restrict options to reduce the electricity sector’s CO2 emissions in succeeding decades and would likely require a major shift to natural gas for electricity generation. This is so because natural gas plants can be built relatively quickly and inexpensively, and their electricity prices could be more attractive than those of other low-carbon energy-producing technologies such as electricity production from renewable energy sources with energy storage.

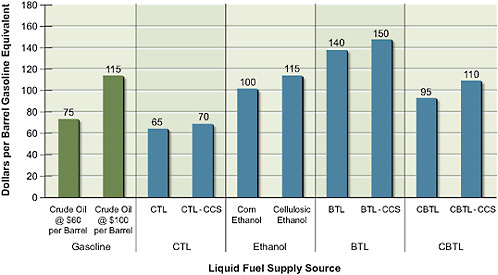

For transportation, new power systems and improvements in the efficiency of vehicles could save 1 million barrels per day of petroleum equivalent by 2020 and 4.1 million barrels per day by 2030. By 2035, emerging liquid transportation fuels, including cellulosic ethanol and coal-and-biomass-to-liquid fuels with CCS, could replace about 15 percent of current fuel consumption in transportation. At the same time, coal-to-liquid fuels with CCS could replace another 15–20 percent of the transportation fuels consumed currently. However, the annual harvesting of up to 500 million dry metric tons of biomass and an increase in U.S. coal extraction by 50 percent over current levels would be required to provide the necessary supply of feedstock for this level of liquid fuel production.

ENERGY EFFICIENCY POTENTIAL

America’s potential for increasing energy efficiency—that is, reducing energy use while delivering the same services—is enormous. Technology exists today, or is expected to be developed before 2030, that could save about 30 percent of the energy used in the buildings, transportation, and industrial sectors while saving money. Potentially, the use of energy efficiency technologies could lower energy consumption by about 15 percent (15–17 quads) in 2020 and an additional 15 percent (32–35 quads) in 2030, compared to the EIA reference case. In fact, the potential savings from increasing energy efficiency in buildings, transportation, and industry could more than offset the EIA’s projected increases in U.S. energy consumption through 2030.

Energy Efficiency—Buildings Sector

Residential and commercial buildings account for about 73 percent of the electricity used in the United States. A number of diverse studies have assessed this sector’s potential for energy savings and are remarkably consistent with each

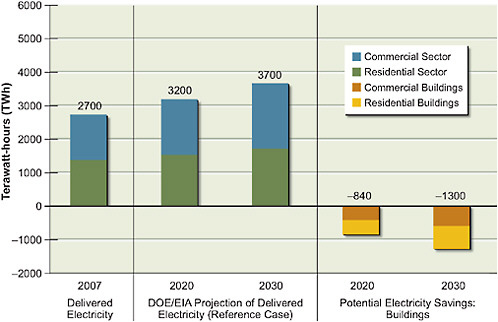

FIGURE 3 Comparison of the delivered electricity in the United States in 2007, used mainly in buildings (left), with the building sector’s projected electricity consumption in 2020 and 2030 (middle), and consumption if there is an accelerated deployment of efficiency technologies (right).

other and with the AEF Committee’s independent analysis. Energy savings of 25–30 percent, relative to the EIA reference case, could be achieved over the next 20–25 years (Figure 3).

More-efficient technologies for space heating and cooling, water heating, and lighting would likely provide most of this reduction. Replacing incandescent lighting with advanced lighting, including compact fluorescent and light-emitting diode (LED) lamps, could save 35 percent of the electricity used for lighting by 2030. In total, these savings could hold buildings’ energy use constant, even as population and other drivers of use grow. For the entire buildings sector, a cumulative investment of $440 billion in existing technology between 2010 and 2030 could produce an annual savings of $170 billion in reduced energy costs. Many efficiency technologies are a sound financial investment for individuals as well, given that most of these more energy-efficient technologies pay for themselves in 2–3 years.

Technologies under development promise even greater gains. In lighting and windows, these technologies include “superwindows” that hold in heat extremely well and dynamic windows that adjust cooling and electric lighting when daylight is available. For cooling, the industry is developing advanced systems that reduce the need for cooling and use low-energy technologies, such as evaporative cooling, solar-thermal cooling, and heat-sensitive dehumidifiers. Other technologies include electronic systems that provide more control over the energy used in homes and very-low-energy-use buildings that combine holistic designs with on-site generation of renewable energy.

Energy Efficiency—Transportation Sector

The transportation sector, which is almost completely dependent on petroleum, produces about one-third of the U.S. greenhouse gases emitted in energy use. However, automobile manufacturers can use technologies existing now to increase fuel economy substantially. Improving today’s spark-ignition, diesel, and hybrid vehicles would lead to most of the reductions in fuel consumption possible over the next 10–20 years. Technologies that improve the efficiency of gasoline sparkignition engines could reduce new-vehicle fuel consumption by 10–15 percent by 2020 and a further 15–20 percent by 2030. Improvements in transmission efficiency and reductions in rolling resistance, aerodynamic drag, and vehicle size and weight can all increase vehicle fuel efficiency as well. Turbocharged diesel engines, which are already 10–15 percent more efficient than gasoline engines, could steadily replace non-turbocharged engines in the fleet. Similarly, the efficiency of gasoline hybrid-electric vehicles, which already consume 30 percent less fuel than spark-ignition engines, should continue to improve.

In the next decade, policy will also drive light-duty-vehicle efficiency gains. The federal government in 2007 set corporate average fuel economy (CAFE) standards for new light-duty vehicles to reach 35 miles per gallon by 2020, a 40 percent improvement in average new-vehicle fuel efficiency. In May 2009, the Obama administration reached agreement with the automotive industry and the state of California to accelerate the achievement of compliance with these standards by 2016. Achieving these goals and continuing to improve efficiency after 2020 will require that manufacturers’ historic emphasis on increasing vehicle power and size be reversed in favor of a focus on fuel economy. Meeting the new CAFE standards will also most likely require that a large fraction of new vehicles be hybrids (Table 2).

TABLE 2 Plausible Share of Advanced Light-Duty Vehicles in the New-Vehicle Market in 2020 and 2035

Over the next decade, plug-in hybrid electric vehicles (PHEVs) that use electricity plus a variety of potential alternative liquid fuels will begin to enter the market, although they are unlikely to reach large numbers before 2020. Whereas hybrids mainly improve performance or fuel economy, PHEVs can draw a good deal of their energy from the electric grid, depending on their design and patterns of daily use. Plug-in vehicles using batteries that allow them to run 40–60 miles on electricity could reduce gasoline/diesel consumption by 75 percent. However, most announced midsize vehicles are being designed for an all-electric range of between 10 and 40 miles. The reductions in fuel consumption will depend not only on the extent of the all-electric range but also on how consumers use these vehicles and the availability of places to charge them daily.

After 2030, hydrogen fuel-cell vehicles and battery-electric vehicles may also make up a significant portion of vehicle sales. Because fuel-cell and battery-electric vehicles could ultimately eliminate the need for petroleum in transportation, they could also reduce and possibly even eliminate light-duty-vehicle tailpipe emissions of greenhouse gases. However, the full-fuel-cycle emissions of greenhouse gases—cumulative emissions associated with all steps in the use of a fuel, from production and refining to distribution and final use—will depend on how hydrogen is produced for use in fuel cell vehicles and how electricity is produced for PHEVs. The success of PHEVs will depend on the development of batteries that have much higher performance capabilities and lower costs than those currently available. The success of fuel cell vehicles will depend on improved and lower-cost fuel cells and probably on a better means of storing hydrogen on board the vehicles.

For heavy-duty freight trucks, future energy efficiency technologies include hybrid-electric systems that better regulate auxiliary features, such as air-conditioning and power steering, and reduce idling. Significant reductions in aerodynamic drag and the use of continuously variable transmissions also offer great potential. Reductions of 10–20 percent in fuel consumption by medium- and heavy-duty vehicles seem to be feasible over the next decade. Shifting freight from trucks to rail can also offer considerable energy savings, because rail is about 10 times more energy-efficient than trucking is.

In the air transportation sector, the latest generation of airliners offers a 15–20 percent improvement in fuel efficiency. However, these newer airplanes are likely to do little more than offset the additional fuel consumption associated with the projected growth in air travel.

System-level improvements not connected to a particular economic sector or transportation mode can also increase future transportation energy efficiency. Using intelligent transportation systems to manage traffic flow, improving land-use management, and employing information technology in place of commuting and long-distance business travel are just a few examples.

Energy Efficiency—Industrial Sector

Independent studies estimate that the industrial sector can cost-effectively reduce fuel use by 14–22 percent—5–7 quads—by 2020, compared with reference case projections. Most of the gains will occur in energy-intensive manufacturing—especially chemicals and petroleum, pulp and paper, iron and steel, and cement—which is the focus of this analysis.

In chemical and petroleum production, technologies for improving energy efficiency include high-temperature reactors, corrosion-resistant metal- and ceramic-lined reactors, and sophisticated process controls. By 2020, the petroleum-refining sector could cost-effectively increase its energy efficiency by 10–20 percent.

The pulp and paper industry could increase its efficiency through the use of waste heat for drying, advanced water-removal and filtration technologies, high-efficiency pulping processes, and modernized lime kilns. This sector could experience cost-effective gains of 16–26 percent in energy efficiency by 2020.

Promising advances in technology that could be available by 2020 for manufacturing iron and steel include advances for melting, heat recovery, integration of refining functions, and heat capture from waste gas. The American Iron and Steel

Institute recently announced a goal of using 40 percent less energy in production in 2025 than was used in 2003.

To experience the largest energy savings, cement plants must upgrade to an advanced dry-kiln process, but this purchase is economical only when producers must replace an older kiln. However, a combination of other improvements, including advanced control systems and developments in combustion efficiency, could decrease energy use by about 10 percent. In addition, changing the chemistry of cement to decrease the amount of lime in it could reduce energy use by another 10–20 percent. The AEF Committee estimated that savings of 20 percent in the U.S. cement industry are possible by 2020.

Across the industrial sector, several technologies could improve efficiency in a number of applications. Growth in the use of combined heat and power production is the most significant. This process uses the waste heat that is produced when fuel is converted to electricity for water heating, space heating, or industrial processes. Other promising technologies include remanufacturing products for resale, advanced materials that hold up well at high temperatures, sensor systems that increase control, and advances in recycling.

Energy Efficiency—Barriers to Deployment of Better Technologies

Numerous barriers discourage the use of energy efficiency technologies. In the buildings sector, most utilities profit when consumers use more energy and so are not rewarded for achieving increases in energy efficiency. Similarly, as builders and landlords do not pay the energy bills, they lack the financial incentives to invest in energy efficiency. Even for those who wish to invest, information about the energy costs of specific appliances and equipment is often hard to find. Despite the quick payback, people are also put off by these technologies’ initial higher costs. In transportation, the unpredictability of future oil prices and the inability of vehicle manufacturers to change production processes rapidly and drastically are hindrances. In the industrial sector, cautious business owners are often concerned about adopting any new technology. In addition, high initial costs for efficiency improvements, a lack of knowledge, and taxes that inadvertently discourage investments in energy efficiency pose barriers. Sustained public and private support will be needed to overcome these formidable barriers. It is especially important that the installation of efficient technologies and systems be encouraged whenever infrastructure, industrial equipment, and other long-lived assets are bought or constructed.

Meanwhile, some national and state policies have already started the United States on a path toward fulfilling energy efficiency’s potential. Vehicle and appliance efficiency standards, combined with research and development sponsored by the U.S. Department of Energy (DOE), have been particularly successful. Other effective policies include the federal promotion of combined heat and power, the ENERGY STAR® product labeling program, building energy codes, and utility- and state-sponsored end-use efficiency programs. These initiatives have already resulted in a nearly 13-quad annual reduction in primary energy use.

New incentives that might help overcome traditional barriers to adopting energy efficiency include heightened concern about potential increases in energy prices, questions about future availability of fuel and electricity, and increasingly stringent air-quality standards. Other important motivations include a desire to improve product quality and productivity, corporate sustainability initiatives, and rising environmental awareness. Even so, substantial energy savings will be realized only if efficient technologies and practices achieve wide use and if well-designed policies can surmount barriers and encourage energy efficiency.

ENERGY-SUPPLY OPTIONS

Electricity from Renewable Resources

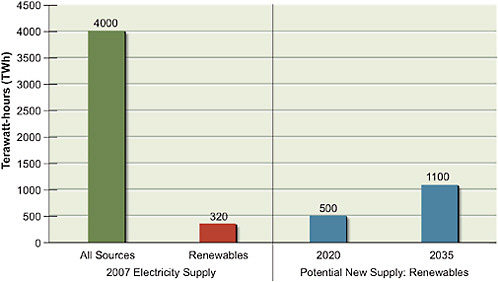

Over the past 20 years, the level of electricity generation from renewable resources has risen significantly. The largest source of renewable energy in the United States, conventional hydroelectric power, generated 6 percent (almost 250,000 gigawatt-hours, or GWh, out of a total 4.16 million GWh) of the electricity produced in 2007. However, environmental concerns may limit further growth in hydroelectric sources, and nonhydroelectric renewable sources currently provide only 2.5 percent of all U.S. electricity. Based on the current rate of growth, the EIA’s reference case estimates that nonhydroelectric renewables will contribute only 7 percent of electricity generation by 2030. But the AEF Committee found that with a sustained, accelerated effort, nonhydroelectric renewables could collectively provide 10 percent of the nation’s electricity generation by 2020 and 20 percent or more by 2035. With current hydropower included, renewables could fulfill more than a quarter of the nation’s electricity needs by 2035 (Figure 4).

FIGURE 4 Estimated potential new energy supply from renewables in 2020 and 2035 (right) compared to current supply from all sources (left), including renewable sources (red) such as conventional hydropower. Potential new supply shown is in addition to currently operating supply. An accelerated deployment of technologies is assumed. All values are rounded to two significant figures.

Technologies for Electric Power from Renewable Sources

Several renewable energy technologies for power generation from wind, solar, geothermal, hydropower, and biomass fuels are now available and are undergoing further improvements.

In the wind sector, turbine technology has advanced substantially in recent years. Future technology development and deployment will focus on improving efficiency and lowering production costs and in particular will aim to improve turbine output of electricity and the effective integration of wind turbines into electric grid operations.

Solar electric power can be produced by either solar photovoltaic or concentrating solar power technologies. For areas of high solar intensity, such as the southwestern United States, concentrating solar power technology can be the cheapest means of producing solar electricity on a utility-scale level. Advances in high-temperature and optical materials could further reduce costs. Effective elec-

tricity storage technologies will be important for the widespread deployment of solar electric power.

Conventional geothermal power, which uses steam or hot water present within about 3 kilometers (km) of Earth’s surface to drive a heat engine, is a fairly mature technology, but it has a limited resource base. Identified geothermal resources in the western United States have an electrical power capacity of 13 gigawatts (GW). Greatly expanding that base will require enhanced geothermal systems that can mine heat down to 10 km. Such systems face many technical challenges and are not currently operating.

Conventional hydropower is the least expensive and most developed renewable source of electricity. Given environmental concerns that will probably limit hydropower’s expansion, the focus now is on increasing its efficiency and reducing its environmental impacts. Other hydrokinetic technologies can produce electricity using currents, tides, and ocean waves, but no commercial facilities are currently operating, even though many designs and demonstration plants exist.

Biopower relies on three main feedstocks: wood or plant waste, municipal solid waste or landfill gas, and crops grown for energy. These can be used with a variety of technologies to produce electricity, including technologies already used in natural gas plants. However, given resource constraints, the use of biomass for electricity production will compete with its use for alternative liquid transportation fuels such as ethanol.

Renewables—Generation Capacity and Resource Base

Wind and solar power currently have the highest growth rates as renewable resources for electricity generation. Although wind power represented less than 1 percent of total electricity generation in 2007, from 1997 to 2007 it experienced a 25.6 percent compounded annual rate of growth. In 2008, another 8.4 GW of capacity was added, for a total capacity of approximately 25 GW. Despite the economic downturn, which led to decreased financing for new projects and caused layoffs in manufacturing, 2.8 GW of new wind power generation capacity was installed in the first quarter of 2009 alone.

Central-utility generation of electricity from concentrating solar power (CSP) and photovoltaics (PV) combined to supply 600 GWh in 2007, 0.01 percent of the electricity generated in the United States. This level has been approximately constant since 1990. However, it does not account for the increase in residential and other small-PV installations, the fastest-growing sector in solar electricity. Use

of solar PV in the United States has grown at a compounded annual rate of more than 40 percent from 2000 to 2005, with a generation capacity of almost 0.5 GW.

The United States has sufficient resources to expand significantly the amount of electricity that it generates from renewables. Solar energy, followed by wind, offers the greatest potential among domestic renewable resources. Solar energy could potentially produce many times the current and projected future U.S. electricity consumption. Wind power across the continental United States could produce 11 million GWh per year, far more than the estimated total of 4 million GWh of electricity generated in 2008. These numbers, however, represent the total resource base and exceed what can be developed cost-effectively. More importantly, the resource bases for wind and solar energy are not evenly distributed in space and time and are not as concentrated as fossil and nuclear energy sources are. Finally, there are many technological, economic, and other constraints on using large-scale renewable energy sources.

Renewables—Deployment Potential

Between now and 2020, there are no technological constraints to the accelerated adoption of renewable energy, but several substantial barriers exist. One significant barrier is that existing technologies for electricity generation from renewables are more expensive than those for most fossil-fuel-based sources of electricity if no costs are assigned to emissions of greenhouse gases or other pollutants. Other hindrances include a lack of sufficient transmission capacity and the inconsistency of policies supporting the renewable power industry.

A reasonable target for 2020 is that all renewable resources supply 20 percent of the nation’s electricity, with approximately half of that generated from nonhydropower renewables. By 2035, with continued accelerated adoption and sustained policies, electricity generation from renewable sources other than hydropower could reach 20 percent of total U.S. electricity generation.

The most in-depth description of how to scale renewable generation up to this level is the DOE’s 20-percent-wind-penetration scenario,6 which requires that the wind power industry install 16 GW of capacity annually until 2018—a rate almost double the current U.S. annual rate of deployment but less than the current global deployment of 27 GW. In total, this scenario predicts the installation of

100,000 wind turbines, establishing approximately 300 GW of new wind power capacity, with 250 GW onshore and 50 GW offshore. In considering the projected installation rate together with the reliability of wind facilities, the AEF Committee concluded that this scenario would be achievable with incentives for accelerated adoption.

Another approach to reach 20 percent generation of electricity from nonhydropower renewables is the expansion of multiple renewable sources. Obtaining an annual average of 20 percent of generation solely from wind power would be challenging because wind power is intermittent. However, wind could be balanced with multiple renewable resources including solar, which normally peaks at a different time of day from wind, and with steady baseload power from geothermal and biomass sources. Relying on multiple renewable resources could also take advantage of their geographical variability, provide more consistent generation, and reduce variability in supply over time. However, it would not reduce cost, eliminate the need to expand transmission, or reduce the need for other improvements to the electricity infrastructure. Reaching a level of 20 percent nonhydropower renewables by 2035 could be achieved by adding 9.5 GW of wind power annually, a total of 70 GW from solar PV, and 13 GW each of geothermal and biomass. The installation rate for wind power under this option is approximately the current rate of installation, and the installation rates of the other renewable technologies are consistent with an accelerated deployment schedule.

Greatly expanding the fraction of electricity generated from renewable sources will require changes in the present electric system because of variability over space and time in the availability of renewables such as wind and the difficulty of scaling up renewable resources. Integrating an additional 20 percent of renewable electricity, whether from wind, solar, or some combination of sources, will require an expansion of the transmission system as well as large increases in manufacturing, employment in the wind power industry, and investment. Integrating renewables so that they account for more than 50 percent of U.S. electricity generation would require scientific advances and major changes in electricity production and use. It would also necessitate the adoption of electricity storage technologies to offset renewables’ intermittency.

Renewables—Cost

Over the past 20–30 years, renewable sources of electricity generation have generally been more expensive than most other sources of electricity. In terms of cost

alone, onshore wind is the most favorable renewable electricity technology out to 2020 (see Figure 6 on p. 37). With federal production tax credits for renewables or high prices for natural gas, wind is competitive with natural gas for electricity generation.

Solar PV presents a different economic picture. PV is a distributed generation source, with the electricity generated in the place where it is used, such as on a house’s roof. Even though solar PV is much more expensive than utility-level sources, it competes against retail electricity prices, not wholesale electricity prices. Thus, if electricity prices continue to increase and more utilities adopt time-of-day pricing, which charges the highest rate during the middle of the day, solar PV could become more cost competitive. Its competitiveness could be limited, however, if residential and commercial solar PV systems fall short of their potential output because of placement on roofs that lack full exposure to the Sun. In addition, consumers still require the full electricity distribution system and utility connections for periods when their solar systems are not generating electricity.

In general, nearly all of the costs involved in using renewable energy for power generation are associated with the manufacturing and installation of the equipment. Fuel costs during operation—except those for biomass—are zero. Renewable energy manufacturing plants can be built quickly and incrementally compared to conventional coal and nuclear plants. Because speed at this stage allows utilities and developers to begin recouping costs sooner, innovations in manufacturing will strongly influence the evolution of the costs of using renewable technologies in electric power generation.

The DOE 20 percent wind study referred to above provides one estimate of the costs of obtaining a 20 percent annual average of total electricity generation from renewable energy sources in the United States. Although a single study, it included contributions from a wide array of stakeholders, including electric utilities, wind power companies, engineering consultant firms, and environmental organizations. The study considered the direct costs of installing the generating capacity and integrating this power into the electricity system. For the 20 percent scenario, it projected that wind power costs (capital, operation, and maintenance expenses) would be approximately $300 billion. In addition, estimates of the cumulative costs of needed improvements in the U.S. transmission system range from $23 billion to $100 billion (through 2024).

Renewables—Barriers to Deployment

High cost has been the major barrier to the adoption of renewable sources of electricity. Recent limitations in personnel, materials, and manufacturing have further increased the costs of solar PV and wind power projects. More importantly, because some sources of renewable electricity are intermittent, the more capacity there is, the greater is the difficulty of integrating that capacity into existing electric power systems. Providing 20 percent of all generation from renewable sources will require greater transmission capacity and additional generation sources that can be activated quickly to provide electricity when renewables are not available. Physically expanding the transmission system (including power lines), improving operators’ ability to control the system, and co-siting intermittent renewables with other sources of electricity can support the integration of renewables. At this high level of renewable technology deployment, land-use and other local impacts also become important. Such impacts have provoked local controversy around the siting of wind farms and associated transmission lines, and opposition is likely to continue in the future.

Consistent and long-term commitments from policy makers are essential for encouraging investment and allowing renewable generation to reach its potential. The “on-again, off-again” nature of the federal production tax credit, for example, has directly hampered the installation of new renewable generation facilities.

Renewables—Impacts

The lifetime emissions of CO2 and criteria pollutants7 per kilowatt-hour for renewable energy, i.e., accounting for emissions from the extraction of natural resources to final disposal, are lower than for fossil energy, although lifetime emissions associated with renewables are about the same as those for nuclear power. Renewable electricity technologies (except for biopower, some geothermal, and high-temperature solar technologies) also use significantly less water than is required for nuclear, natural-gas-fired, or coal-fired electricity production. Land-use requirements are substantially higher for renewables, but in some cases (e.g., wind) the land can often be used for multiple activities, such as agriculture.

Nuclear Energy

U.S. energy companies have recently expressed increased interest in constructing new nuclear power plants. Among their motivations are the need for additional baseload generating capacity, concern about emissions of greenhouse gases from fossil fuel plants, and the volatility of natural gas prices. They have also cited favorable experiences with existing nuclear power plants, including ongoing improvements in reliability and safety.8 If this interest continues, an expansion of nuclear power through 2020 and, most likely, through 2035 will not require any major research and development. Nonetheless, the high cost of nuclear power plant construction is a major concern, as is the aging of current plants. The actual experience with the handful of plants that could be built before 2020 will be critical in shaping the possibilities for the increased role of nuclear power.

Nuclear Power—Technologies

The nuclear plants now in place in the United States were built with technology developed in the 1960s and 1970s. The industry has since discovered how to make better use of existing plants, along with incorporating new technologies that improve safety and security, decrease costs, and reduce the generation of high-level waste. Incremental improvements to the 104 currently operating U.S. nuclear plants have enabled them to produce more power than anticipated over their lifetimes. The average plant’s capacity factor9 grew from 66 percent in 1990 to 91.8 percent in 2007, made possible primarily by shortening the duration of outages, reducing periods when plants were off-line, and improving maintenance. Modifying existing plants to increase output is considerably less expensive than adding new capacity, and additional improvements are expected. In fact, nearly as much new nuclear capacity could be added in this way before 2020 as could be produced during that period by building new plants. Additionally, most of the operators of current nuclear power plants have received or are expecting to receive

20-year operating-license extensions. These first extensions would allow plants to operate for a total of 60 years. Discussions have also begun about extending current licenses an additional 20 years, for a total of 80 years.

New plants constructed before 2020 will be “evolutionary” plants, based on modifications of existing plant designs and using technologies that are largely ready now. Plants built after 2020 may use alternative plant designs in two categories: thermal neutron reactor designs (all current U.S. reactors are thermal) and fast neutron reactor designs. Some thermal neutron reactor plants operate at higher temperatures than current plants and produce heat that could be used, in addition to electricity. Fast neutron reactor plants are designed to destroy undesirable isotopes associated with much of the long-lived radioactive waste in used fuel. In some cases, they also breed additional fuel. These plants could reduce the volume of, and the heat emitted by, long-lived nuclear waste that must go to a repository for disposal. However, significant research and development will be needed before these alternative reactor types can be expected to make significant contributions to the U.S. energy supply.

Alternative fuel cycles may also offer potential. The United States currently employs a once-through nuclear fuel cycle in which used fuel is disposed of after removal from the reactor. In contrast, alternative (closed) nuclear fuel cycles reprocess used fuel to produce new fuel. In principle, these alternative fuel cycles could extend fuel supplies and reduce the amount of long-lived nuclear waste. However, the reprocessing technology commonly used today, called plutonium and uranium extraction (PUREX), yields a separated stream of plutonium. As a result, the process is associated with an increased risk of nuclear weapons proliferation, theft, or diversion of nuclear materials.10 A modified version of PUREX that keeps uranium with the plutonium would be less risky and could be used after 2020. Other alternatives are being investigated but are unlikely to be ready for commercial use before 2035. Research and development is still needed on reactor design, fuel design, separation processes, fuel production, and fuel application.

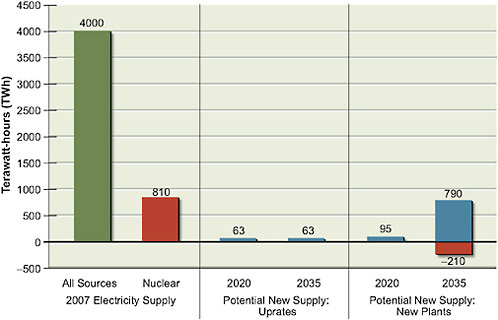

FIGURE 5 Estimates of potential new electricity supply from nuclear “uprates” (middle), which are increases in power generation capacity at existing nuclear power plants, and new plants (right) in 2020 and 2035 compared to supply from all sources (left, in green). The supply generated by nuclear power is shown in red. An accelerated deployment of technologies and a capacity factor of 90 percent are assumed. It is also assumed that current plants will be retired at the end of 60-year operating lives, resulting in a reduced supply of electricity from nuclear power in 2035, shown by the negative-valued red bar on the right. However, if operating extensions to 80 years are approved for these plants, they may not be retired by 2035. All values are rounded to two significant figures.

Nuclear Power—Development Potential

By 2020, as many as five to nine new evolutionary nuclear plants could be built in the United States. However, in light of the long construction times, the first one is unlikely to be operating before 2015. By combining new power plants with capacity from modified plants, an increase of 12–20 percent in U.S. nuclear capacity is possible by 2020 (Figure 5).

After 2020, the potential magnitude of nuclear power’s contribution to the U.S. energy supply is uncertain. The operating licenses of existing plants will begin to expire in 2028. If the government does not issue extensions to lengthen their

operating lifetimes to 80 years, plants will have to be shut down. If this occurs, about 30 percent of the current U.S. nuclear power capacity will be retired by 2035. Many companies will thus have to decide soon whether to replace retiring plants with new plants. Because cost is the major barrier to new construction, companies will need to know whether evolutionary plants can be built on budget and on schedule. One important purpose of providing federal loan guarantees, especially for the next 5–10 nuclear power plants, is for companies to acquire experience with early plants to help guide further decisions.11

The scale of new nuclear deployment after 2020 will depend on the performance of plants built during the next decade. If the first set of new plants constructed in the United States meet cost, schedule, and performance targets, many more plants could be deployed after 2020. Construction of 3–5 plants per year could take place until 2035, growing to 5–10 plants per year after 2035 if there is sufficient demand. However, if the first plants do not meet their targets, other plants are not likely to follow quickly.

Nuclear Power—Costs

The AEF Committee estimated that the levelized cost of electricity (LCOE)—the average cost of generating a unit of electricity over the life of the facility—for new evolutionary nuclear plants could range from 8¢/kWh to 13¢/kWh (see Figure 6 on p. 37). Existing federal incentives—including loan guarantees—could reduce this cost to about 6–8¢/kWh for plants that receive them. These costs are higher than the current average wholesale cost of electricity but are likely to be similar to future costs, particularly if fossil fuel plants are required to sequester CO2 or pay a carbon fee. The costs for improvements to existing plants are from one-tenth to one-third those for the construction of new plants. The possible costs from advanced plant designs and alternative fuel cycles are at present highly uncertain, but plants with these features are likely to cost significantly more than current designs do, although the money saved from handling high-level waste materials that are less long-lived could offset some of the differences.

Nuclear Power—Barriers to Deployment

The high and somewhat uncertain cost of new nuclear power plants, together with the resulting financial risk, is the most significant barrier to new deployment. Nuclear power plants have low operating costs per unit of electricity generated but incur high initial capital costs that present a challenge for companies. In terms of licensing, the U.S. Nuclear Regulatory Commission (USNRC) has begun a revised process that allows for reactor design certification, early site permits, and combined construction and operating licenses. Nevertheless, in light of the surge in recent applications, there may be bottlenecks and delays. Shortages of personnel and equipment could also limit construction over the next decade, but these issues should wane over time.

Public opinion regarding nuclear power has recently improved, but it would most likely turn negative if safety or security problems arose. New reactor construction has been barred in 13 states, although several of these states are reconsidering their bans. The absence of a policy decision regarding the disposal of long-lived nuclear wastes is not a technical impediment to the expansion of nuclear power, but it still poses a public concern.12

Nuclear Power—Impacts

Future expansion of nuclear power would help diversify the U.S. electricity supply. Barring a crash program, renewable energy sources and fossil fuels with carbon capture and storage will most likely not meet the entire U.S. demand for electricity in 2035, even with gains in efficiency. Diversification of the electricity supply would serve as an insurance policy for the United States, particularly in a carbon-constrained economy.

The potential of nuclear power to reduce greenhouse gas emissions is a major factor favoring its expansion, although nuclear power does pose other environmental issues. Under the maximum nuclear power adoption rate discussed in America’s Energy Future: Technology and Transformation, avoided CO2 emissions could reach 180 million tons per year by 2020 and 2.4 billion tons per year by

2050.13 However, the disposal of the resulting radioactive waste, particularly used fuel, presents an environmental challenge. Yucca Mountain, Nevada, one potential disposal site, could not be ready until after 2020, and the prospect is further diminished by the Obama administration’s stated intent not to pursue the development of that site. But the safe and secure on-site or interim storage of used fuel for many decades—until a permanent disposal location can be agreed on—is technically and economically feasible.14

From a security perspective, accidents or terrorist attacks on nuclear reactors or used-fuel storage facilities could release radioactive material. However, existing plants have taken measures to reduce the likelihood and consequences of such events. Furthermore, evolutionary and advanced designs have features that further enhance safety and security.

Fossil Fuel Energy

Fossil fuels—petroleum, natural gas, and coal—currently supply about 85 percent of the nation’s primary energy (see Figure 1) and will continue to be a major source for decades to come.

Resource Base for Petroleum, Natural Gas, and Coal

Although the potentially retrievable amount of petroleum and natural gas worldwide is very large, most of this resource is located outside the United States. In 2007, the United States imported about 58 percent of the petroleum that it consumed, a drop from the 2006 peak of 60 percent. Most of this drop resulted from the growth in production of a half million barrels per day from the deepwater Gulf of Mexico, which suggests that sustaining domestic production levels will depend on developing discovered resources that can make up for a decline in production from existing oil and gas fields.

Maintaining domestic production of petroleum at current levels over the long run will be very challenging. Producing significant volumes before 2020 from U.S.

TABLE 3 Conventional Oil Resources, Reserves, and Production (billions of barrels)

|

|

United States |

World |

U.S. Percent of World Total |

|

Resources |

430a |

3345b |

13 |

|

Reservesc |

29 |

1390 |

2.1 |

|

Annual production |

2.5/yr |

29.8/yr |

8.4 |

|

Annual consumption |

7.5/yr |

31.1/yrd |

24.1 |

|

aAdvanced Resources International, Undeveloped Domestic Oil, U.S. Department of Energy, Washington, D.C., February 2006. bNational Petroleum Council, Facing the Hard Truths About Energy, Topic Papers 7, 19, 21, 24, and 26, Washington, D.C., 2007. cBritish Petroleum, Statistical Review of Energy, London, June 2008. dAccording to British Petroleum, 2008, discrepancies between world production and consumption “are accounted for by stock changes; consumption of nonpetroleum additives and substitute fuels; and unavoidable disparities in the definition, measurement, or conversion of oil supply and demand data.” |

|||

unconventional resources, primarily oil shale, is not likely; it would, in addition, be more expensive than conventional sources of oil and might have larger negative environmental impacts as well. Also, U.S. crude oil reserves and production are only 2 and 8 percent, respectively, of the world’s totals (Table 3). By contrast, because U.S. petroleum consumption is 24 percent of world consumption, changes in U.S. demand are a significant factor in determining world demand, and therefore prices. Growing demand in other countries, however, could offset any downward price pressures resulting from reduced U.S. demand.

The cleanest fossil fuel, natural gas, emits about half as much CO2 per unit of energy as coal does when burned for electricity generation. While the U.S. natural gas resource base is only about 9 percent of the world total, some 86 percent of the natural gas consumed in the United States is produced domestically, and much of the rest comes from Canada. In recent years, natural gas production from conventional resources has declined. But production from unconventional resources, such as coal beds, tight gas sands (rocks through which flow is very slow), and natural gas shales has increased. Higher natural gas prices in 2007 and 2008 led to expanded drilling from unconventional sources. This expansion increased total U.S. gas production by about 9 percent in 2008 after a decade of its being roughly constant.

If the increase in domestic natural gas production is sustained over long periods, it could accommodate some portion of growth in domestic demand. Or, production from existing resources might decline and new resources might experience only modest growth, resulting in the United States having to import liquefied natural gas at unpredictable international market prices. A number of linked factors, including the amount of growth in demand, production technology, resource availability, and price, will determine which of these futures occurs.

About 12 percent of U.S. petroleum resources and 20 percent of U.S. natural gas resources are believed to lie in areas that are currently off-limits, such as some outer continental shelf (OCS) areas off the coasts of Washington, Oregon, and California, off the Atlantic Coast, and in the eastern Gulf of Mexico, although these estimates are highly uncertain and it is estimated that production would be moderate. For example, petroleum production from these areas could be around several hundred thousand barrels per day by the mid-2020s, compared to current domestic production of 5.1 million barrels per day. Gas production from these areas could be about 1.5 trillion cubic feet per year in the 2020–2030 period, compared to current domestic production of 19 trillion cubic feet per year. Policy makers are faced with balancing the energy security and economic benefits of developing these resources against the potentially negative environmental impacts. Most observers believe that U.S. oil production from these restricted areas would have only a small effect on world oil prices. But because natural gas markets are more regional, they might respond differently. Beyond price considerations, it is possible that increased natural gas production from restricted areas could offset the need to import natural gas.

The United States has at least 20 years’ worth of coal reserves in active mines and probably sufficient resources to meet the nation’s needs for well over a century at current rates of consumption. The resource base is unlikely to constrain coal use for many decades to come. Rather, the primary constraints will most likely be a combination of environmental, economic, geographic, geologic, and legal issues. Burning coal to generate electricity produces about 1 metric ton of CO2 equivalent per megawatt-hour. If carbon capture and storage technologies are successfully developed, it is possible that future coal consumption could remain at current levels or could increase, even if greenhouse gas emissions limits are put in place. However, if practical CCS technologies fail to materialize, coal use will be severely curtailed in a world where carbon emissions are constrained.

Carbon Capture and Storage

CCS technologies have been demonstrated at commercial scale, but no large power plant today captures and stores its CO2 by-product. The few large CO2 storage projects now underway are all coupled to nonpower facilities. For example, one offshore operation in Norway separates 50 million standard cubic feet of CO2 per day (1 million metric tons per year) from natural gas before the fuel is inserted into the European grid. The CO2 is then injected under the North Sea.

CO2 storage could be implemented in oil and gas reservoirs, deep formations with salt water, and deep coal beds. Specific sites would have to be selected, engineered, and operated with careful attention to safety. In particular, the deep subsurface rock formations selected to hold the CO2 must allow the injection of large quantities at sufficient rates and must also be layered geologically so as to prevent, over centuries to millennia, the upward migration of injected CO2. Current surveys suggest that the storage available within 50 miles of most of the major U.S. sources of CO2 would be more than enough to handle emissions for many decades, and that up to 20 percent of current emissions could be stored at estimated costs of $50 per ton of CO2 or less. However, given the large volumes involved, the challenge should not be underestimated. At typical densities, a single 1-GW coal-fired plant would have to inject about 300 million standard cubic feet of CO2 per day, a flow for which the volume would equal that of the petroleum produced from a large oil field.

Too little is known now to determine which power generation technologies and which CO2 storage options would be best for electricity production after 2020 if carbon emissions are constrained. The reliable cost and performance data needed for both carbon capture and carbon storage can be obtained only if full-scale demonstration facilities are constructed and operated. Such demonstrations could convince vendors, investors, and other private-industry interests that power plants incorporating advanced technologies and storage facilities could be built and operate cost-effectively. The variety of coal types and the myriad conversion options for coal, natural gas, and biomass fuels will require a diverse portfolio of CO2 capture demonstrations. Similarly, it will be necessary to operate a number of large-scale storage projects in a variety of subsurface settings to evaluate the options and their costs, risks, environmental impacts, legal liabilities, and regulatory and management issues.

The investments in such a portfolio of CCS demonstrations will be large, but there is no benefit in waiting to make them. The AEF Committee judged that

the period between now and 2020 could be sufficient for assessing the viability of CCS if demonstration projects proceed as rapidly as possible. If these investments are made now, 10 GW of CCS projects could be in place by 2020. If not, the ability to introduce CCS will be further delayed. Public acceptance of CCS as a viable strategy can be secured only as a result of demonstration projects that perform reliably.

Fossil Energy Use for Electric Power Generation

In 2006, power plants generated about 52 percent of U.S. electricity from coal and 16 percent from natural gas. Many of these plants could operate for 60 years or more, a period that plant operators do not want to shorten, given that constructing new plants requires obtaining large amounts of capital and numerous permits. Yet, significantly limiting U.S. greenhouse gas emissions will require dramatically reducing emissions from these plants. Alternatives include (1) retiring the plants; (2) raising the generating efficiency, thereby reducing greenhouse gas emissions per unit of electricity produced; (3) retrofitting with CO2 post-combustion capture capability; or (4) repowering/rebuilding at the site, resulting in a unit that is entirely or mostly new.

The two principal technologies for future coal-burning power plants are (1) those using an integrated gasification and combined cycle, which converts coal into a synthesis gas, then removes impurities from the coal gas before it is combusted, and finally utilizes excess heat from the primary combustion and generation in a steam cycle similar to that of a combined-cycle gas turbine and (2) enhancements to traditional pulverized-coal technologies. These technologies have varying potential for reducing coal plants’ greenhouse gas emissions. Pulverized-coal units now produce nearly all of the coal-based electric power in the United States. Compared with older steam plants, which have an efficiency of about 34–38 percent, these “ultrasupercritical” plants could reach 40–44 percent efficiency between 2020 and 2035. Replacing a plant of 37 percent efficiency with one of 42 percent efficiency would result in a 12 percent reduction in CO2-equivalent emissions and fuel consumption per kilowatt-hour of output.

Reducing emissions more dramatically in pulverized-coal plants will require CCS. With today’s technology, the cost for retrofitting to 90 percent CO2 capture at an existing pulverized-coal plant would be nearly as high as the cost of the original plant. In addition, 20–40 percent of the plant’s energy would be diverted for the separation, compression, and transmission of the CO2, thus reducing its effi-

ciency and increasing the cost of electricity. In addition, the feasibility of installing CO2-capture retrofits varies strongly from plant to plant. Analyses that can determine when retrofitting a plant becomes more cost-effective than building a new plant, and what percentage of CO2 is captured in that situation, would provide considerable aid to policy makers.

New natural gas combined-cycle plants are competitive with new coal plants. Even though natural gas plants have lower capital costs and shorter construction times, the price of natural gas strongly influences investors. For example, with natural gas at a price of $6 per million British thermal units (Btu), natural gas plants are the lowest-cost option for electricity generation, whereas natural gas at $16 per million Btu makes such plants the highest-cost option. For comparison, over the course of this study U.S. natural gas prices rose above $13 per million Btu and fell to below $4 per million Btu.

Future rules governing greenhouse gas emissions and the pace at which CCS technologies can be commercialized will also affect the competitiveness of coal versus natural gas. Although a large shift toward natural gas would increase demand and put upward pressure on prices, the AEF Committee considered it wise to plan for a broad range of future prices and varying domestic availability. It envisioned some CCS projects involving natural gas combined-cycle technology as being part of the recommended 10 GW of CCS demonstrations.

The AEF Committee compared the costs of new pulverized-coal, integrated gasification and combined-cycle, and natural gas plants, with and without CCS, built with components available today and with various prices assigned for CO2 emissions. (The committee also considered biomass, and biomass and coal in combination, as feedstocks.) If no price is put on CO2 emissions, pulverized coal without CCS is the cheapest option (see Figure 6 on p. 37). However, in a world with a price on carbon, CCS will most likely be required. If CCS becomes necessary, adding it to pulverized-coal plants is more expensive than adding it to integrated gasification and combined-cycle plants. Assuming a price of $50 per metric ton of CO2 and the use of bituminous coal, the cheapest of the four coal plant options for generating electricity is integrated gasification and combined-cycle plants with CCS, even though the electricity would still cost more than at current rates. If domestic natural gas proves plentiful and prices remain in the range of $7–9 per million Btu or lower,15 then natural gas plants with CCS could compete

economically with coal plants with CCS. In such a world, the cheapest way to gain large reductions in CO2 would be to use natural gas combined-cycle plants plus CCS to replace existing and future coal units over time. These cost estimates are subject to uncertainties regarding fuel costs, capital costs for first-of-a-kind plants, and the costs of CCS technology. In addition to these current options, coal combustion with pure oxygen instead of air is a possible option that would simplify CO2 capture and that might be competitive in the future.

If CCS is adequately developed, demonstration fossil-fuel CCS plants providing 10 GW could be operating by 2020, with strong policy incentives in place. One such incentive would be a CO2 emissions price of about $100 per metric ton. Given similar assumptions, 5 GW per year could be added between 2020 and 2025, and a further 10–20 GW per year from 2025 to 2035. This expansion would result in a total of 135–235 GW of fossil fuel power with CCS in 2035. The AEF Committee did not make a judgment about the mix of natural gas combined-cycle, pulverized-coal, and integrated gasification and combined-cycle plants with CCS that would be appropriate. Potentially, all existing coal-fired power plants could be replaced by those with CCS by 2035. Whether any coal plants and natural gas plants without CCS will still be operating in 2035 will depend on the policies in place at that time for limiting emissions of greenhouse gases.

Fossil Fuels—Impacts of and Barriers to Deployment

The widespread use of fossil fuels in the United States has significant environmental impacts, many of which have been addressed over the past few decades by a broad array of laws and regulations. The notable exception is the emission of greenhouse gases. A continual challenge is to keep policy instruments—especially those affecting greenhouse gas emissions—up to date and enforced as fuel consumption increases.

All of the pertinent environmental issues need to be fully considered in assessing the real costs of different energy options. Agencies, stakeholders, and investors concerned with environmental impacts must also prepare for future challenges. Increasing the use of coal, oil shale, and tar sands will intensify environmental and safety concerns surrounding extraction and emissions. Expansion of liquefied natural gas imports may raise concerns about potential impacts of storage facilities on coastal areas, impacts of pipeline enlargement, and infrastructure vulnerability to terrorist attacks. Burning more fossil fuels for electricity will increase power plants’ use of freshwater and negatively affect water quality, aquatic life, and surrounding ecosystems.

To continue the use of fossil fuels in a carbon-constrained world, government will have to develop, in addition to current policies, a regulatory structure for large-scale deployment of CCS between 2010 and 2020. This regulatory structure should address a number of issues, including CO2 pipeline-transport safety and land use, the stability and leakage of carbon stored underground, and public acceptance of such storage.

FUTURE ELECTRICITY GENERATION COSTS AND THE DEVELOPMENT OF TRANSMISSION AND DISTRIBUTION INFRASTRUCTURE

Estimating Future Costs of Electricity Generation

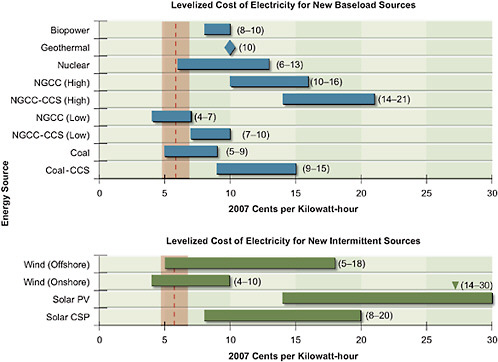

Although their potential is promising overall, new sources of electricity supply will likely result in higher electricity prices. Estimates of the levelized cost of electricity for new baseload and intermittent generation of electricity in 2020 are shown in Figure 6, which indicates a range of LCOE values for each technology and also shows that the ranges for many different technologies are overlapping.

The LCOEs for most of the new sources of electricity in 2020 shown in Figure 6 are higher than projected wholesale costs. The clear exceptions are natural gas combined-cycle generation with low gas prices, coal without CCS, some biopower for baseload generation, and onshore wind for intermittent generation. However, biopower can provide only limited new supplies of electricity, and wind power can incur large transmission and distribution costs for electric power generated by sources that are spatially distributed. Additionally, the generation of electricity using natural gas and coal without CCS might not be environmentally acceptable, and the price for electricity from natural gas could increase substantially, of course, if there were large price increases for this fuel.

Future electricity costs will also be affected substantially by the rate of deployment of energy efficiency improvements. The cost of the energy saved through efficiency, however, is considerably lower than the price of residential and commercial electricity. For example, a sizable fraction of the 30–35 percent reduction in energy use potentially achievable with existing energy efficiency technologies includes a substantial deployment of technologies at a cost that is a quarter of current retail electricity prices (although regional and other differences in cost are considerable).

FIGURE 6 Estimates of the levelized cost of electricity for new baseload and intermittent generating sources in 2020. The vertical shaded bar shows the approximate range of average U.S. wholesale electricity prices in 2007; the dashed vertical line shows the average value in 2007, which was 5.7¢/kWh.

Electricity Transmission and Distribution

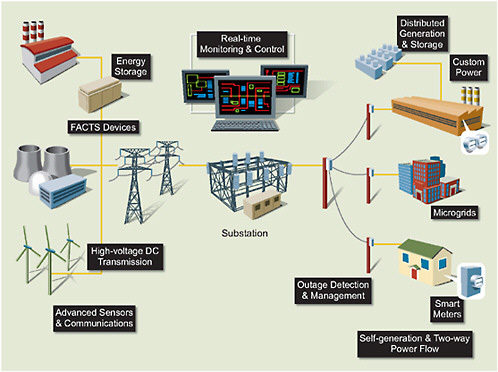

The U.S. electric power transmission and distribution system—the vital link between power-generating stations and customers—is in urgent need of expansion and upgrading. But with an investment only modestly greater than the cost of adding transmission lines and replacing vintage equipment, new technology could be incorporated that would improve the reliability of power delivery, enable the growth of wholesale power markets, allow integration of renewable energy sources into the power grid, improve resilience against blackouts and other disruptions, and provide better price signals to customers through “smart” metering.

FIGURE 7 Technologies for modernizing the U.S. transmission and distribution of electricity. Flexible Alternating Current Transmission System (FACTS) devices include technology for improving control and enhancing the steady-state security of transmission and distribution systems.

Transmission and Distribution—Emerging Technologies

Advanced power electronics, which have been used in limited applications, would provide increased control for both transmission and distribution, and high-voltage direct current (HVDC) lines offer the potential for more-efficient long-distance transmission and grid operation (Figure 7).16 Some DC lines are already