David H. Kaye, M.A., J.D., is Distinguished Professor of Law and Weiss Family Scholar, The Pennsylvania State University, University Park, and Regents’ Professor Emeritus, Arizona State University Sandra Day O’Connor College of Law and School of Life Sciences, Tempe.

David A. Freedman, Ph.D., was Professor of Statistics, University of California, Berkeley.

[Editor’s Note: Sadly, Professor Freedman passed away during the production of this manual.]

CONTENTS

A. Admissibility and Weight of Statistical Studies

B. Varieties and Limits of Statistical Expertise

C. Procedures That Enhance Statistical Testimony

1. Maintaining professional autonomy

3. Disclosing data and analytical methods before trial

II. How Have the Data Been Collected?

A. Is the Study Designed to Investigate Causation?

2. Randomized controlled experiments

4. Can the results be generalized?

B. Descriptive Surveys and Censuses

1. What method is used to select the units?

2. Of the units selected, which are measured?

1. Is the measurement process reliable?

2. Is the measurement process valid?

3. Are the measurements recorded correctly?

III. How Have the Data Been Presented?

A. Are Rates or Percentages Properly Interpreted?

1. Have appropriate benchmarks been provided?

2. Have the data collection procedures changed?

3. Are the categories appropriate?

C. Does a Graph Portray Data Fairly?

2. How are distributions displayed?

D. Is an Appropriate Measure Used for the Center of a Distribution?

E. Is an Appropriate Measure of Variability Used?

IV. What Inferences Can Be Drawn from the Data?

1. What estimator should be used?

2. What is the standard error? The confidence interval?

3. How big should the sample be?

4. What are the technical difficulties?

B. Significance Levels and Hypothesis Tests

2. Is a difference statistically significant?

3. Tests or interval estimates?

4. Is the sample statistically significant?

C. Evaluating Hypothesis Tests

1. What is the power of the test?

4. How many tests have been done?

5. What are the rival hypotheses?

2. Do outliers influence the correlation coefficient?

3. Does a confounding variable influence the coefficient?

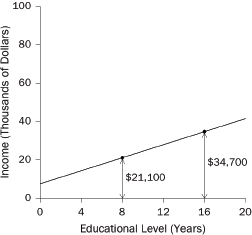

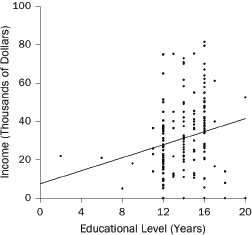

1. What are the slope and intercept?

2. What is the unit of analysis?

B. The Spock Jury: Technical Details

C. The Nixon Papers: Technical Details

D. A Social Science Example of Regression: Gender Discrimination in Salaries

2. Standard errors, t-statistics, and statistical significance

Statistical assessments are prominent in many kinds of legal cases, including antitrust, employment discrimination, toxic torts, and voting rights cases.1 This reference guide describes the elements of statistical reasoning. We hope the explanations will help judges and lawyers to understand statistical terminology, to see the strengths and weaknesses of statistical arguments, and to apply relevant legal doctrine. The guide is organized as follows:

- Section I provides an overview of the field, discusses the admissibility of statistical studies, and offers some suggestions about procedures that encourage the best use of statistical evidence.

- Section II addresses data collection and explains why the design of a study is the most important determinant of its quality. This section compares experiments with observational studies and surveys with censuses, indicating when the various kinds of study are likely to provide useful results.

- Section III discusses the art of summarizing data. This section considers the mean, median, and standard deviation. These are basic descriptive statistics, and most statistical analyses use them as building blocks. This section also discusses patterns in data that are brought out by graphs, percentages, and tables.

- Section IV describes the logic of statistical inference, emphasizing foundations and disclosing limitations. This section covers estimation, standard errors and confidence intervals, p-values, and hypothesis tests.

- Section V shows how associations can be described by scatter diagrams, correlation coefficients, and regression lines. Regression is often used to infer causation from association. This section explains the technique, indicating the circumstances under which it and other statistical models are likely to succeed—or fail.

- An appendix provides some technical details.

- The glossary defines statistical terms that may be encountered in litigation.

1. See generally Statistical Science in the Courtroom (Joseph L. Gastwirth ed., 2000); Statistics and the Law (Morris H. DeGroot et al. eds., 1986); National Research Council, The Evolving Role of Statistical Assessments as Evidence in the Courts (Stephen E. Fienberg ed., 1989) [hereinafter The Evolving Role of Statistical Assessments as Evidence in the Courts]; Michael O. Finkelstein & Bruce Levin, Statistics for Lawyers (2d ed. 2001); 1 & 2 Joseph L. Gastwirth, Statistical Reasoning in Law and Public Policy (1988); Hans Zeisel & David Kaye, Prove It with Figures: Empirical Methods in Law and Litigation (1997).

A. Admissibility and Weight of Statistical Studies

Statistical studies suitably designed to address a material issue generally will be admissible under the Federal Rules of Evidence. The hearsay rule rarely is a serious barrier to the presentation of statistical studies, because such studies may be offered to explain the basis for an expert’s opinion or may be admissible under the learned treatise exception to the hearsay rule.2 Because most statistical methods relied on in court are described in textbooks or journal articles and are capable of producing useful results when properly applied, these methods generally satisfy important aspects of the “scientific knowledge” requirement in Daubert v. Merrell Dow Pharmaceuticals, Inc.3 Of course, a particular study may use a method that is entirely appropriate but that is so poorly executed that it should be inadmissible under Federal Rules of Evidence 403 and 702.4 Or, the method may be inappropriate for the problem at hand and thus lack the “fit” spoken of in Daubert.5 Or the study might rest on data of the type not reasonably relied on by statisticians or substantive experts and hence run afoul of Federal Rule of Evidence 703. Often, however, the battle over statistical evidence concerns weight or sufficiency rather than admissibility.

B. Varieties and Limits of Statistical Expertise

For convenience, the field of statistics may be divided into three subfields: probability theory, theoretical statistics, and applied statistics. Probability theory is the mathematical study of outcomes that are governed, at least in part, by chance. Theoretical statistics is about the properties of statistical procedures, including error rates; probability theory plays a key role in this endeavor. Applied statistics draws on both of these fields to develop techniques for collecting or analyzing particular types of data.

2. See generally 2 McCormick on Evidence §§ 321, 324.3 (Kenneth S. Broun ed., 6th ed. 2006). Studies published by government agencies also may be admissible as public records. Id. § 296.

3. 509 U.S. 579, 589–90 (1993).

4. See Kumho Tire Co. v. Carmichael, 526 U.S. 137, 152 (1999) (suggesting that the trial court should “make certain that an expert, whether basing testimony upon professional studies or personal experience, employs in the courtroom the same level of intellectual rigor that characterizes the practice of an expert in the relevant field.”); Malletier v. Dooney & Bourke, Inc., 525 F. Supp. 2d 558, 562–63 (S.D.N.Y. 2007) (“While errors in a survey’s methodology usually go to the weight accorded to the conclusions rather than its admissibility,…‘there will be occasions when the proffered survey is so flawed as to be completely unhelpful to the trier of fact.’”) (quoting AHP Subsidiary Holding Co. v. Stuart Hale Co., 1 F.3d 611, 618 (7th Cir.1993)).

5. Daubert, 509 U.S. at 591; Anderson v. Westinghouse Savannah River Co., 406 F.3d 248 (4th Cir. 2005) (motion to exclude statistical analysis that compared black and white employees without adequately taking into account differences in their job titles or positions was properly granted under Daubert); Malletier, 525 F. Supp. 2d at 569 (excluding a consumer survey for “a lack of fit between the survey’s questions and the law of dilution” and errors in the execution of the survey).

Statistical expertise is not confined to those with degrees in statistics. Because statistical reasoning underlies many kinds of empirical research, scholars in a variety of fields—including biology, economics, epidemiology, political science, and psychology—are exposed to statistical ideas, with an emphasis on the methods most important to the discipline.

Experts who specialize in using statistical methods, and whose professional careers demonstrate this orientation, are most likely to use appropriate procedures and correctly interpret the results. By contrast, forensic scientists often lack basic information about the studies underlying their testimony. State v. Garrison6 illustrates the problem. In this murder prosecution involving bite mark evidence, a dentist was allowed to testify that “the probability factor of two sets of teeth being identical in a case similar to this is, approximately, eight in one million,” even though “he was unaware of the formula utilized to arrive at that figure other than that it was ‘computerized.’”7

At the same time, the choice of which data to examine, or how best to model a particular process, could require subject matter expertise that a statistician lacks. As a result, cases involving statistical evidence frequently are (or should be) “two expert” cases of interlocking testimony. A labor economist, for example, may supply a definition of the relevant labor market from which an employer draws its employees; the statistical expert may then compare the race of new hires to the racial composition of the labor market. Naturally, the value of the statistical analysis depends on the substantive knowledge that informs it.8

C. Procedures That Enhance Statistical Testimony

1. Maintaining professional autonomy

Ideally, experts who conduct research in the context of litigation should proceed with the same objectivity that would be required in other contexts. Thus, experts who testify (or who supply results used in testimony) should conduct the analysis required to address in a professionally responsible fashion the issues posed by the litigation.9 Questions about the freedom of inquiry accorded to testifying experts,

6. 585 P.2d 563 (Ariz. 1978).

7. Id. at 566, 568. For other examples, see David H. Kaye et al., The New Wigmore: A Treatise on Evidence: Expert Evidence § 12.2 (2d ed. 2011).

8. In Vuyanich v. Republic National Bank, 505 F. Supp. 224, 319 (N.D. Tex. 1980), vacated, 723 F.2d 1195 (5th Cir. 1984), defendant’s statistical expert criticized the plaintiffs’ statistical model for an implicit, but restrictive, assumption about male and female salaries. The district court trying the case accepted the model because the plaintiffs’ expert had a “very strong guess” about the assumption, and her expertise included labor economics as well as statistics. Id. It is doubtful, however, that economic knowledge sheds much light on the assumption, and it would have been simple to perform a less restrictive analysis.

9. See The Evolving Role of Statistical Assessments as Evidence in the Courts, supra note 1, at 164 (recommending that the expert be free to consult with colleagues who have not been retained

as well as the scope and depth of their investigations, may reveal some of the limitations to the testimony.

Statisticians analyze data using a variety of methods. There is much to be said for looking at the data in several ways. To permit a fair evaluation of the analysis that is eventually settled on, however, the testifying expert can be asked to explain how that approach was developed. According to some commentators, counsel who know of analyses that do not support the client’s position should reveal them, rather than presenting only favorable results.10

3. Disclosing data and analytical methods before trial

The collection of data often is expensive and subject to errors and omissions. Moreover, careful exploration of the data can be time-consuming. To minimize debates at trial over the accuracy of data and the choice of analytical techniques, pretrial discovery procedures should be used, particularly with respect to the quality of the data and the method of analysis.11

II. How Have the Data Been Collected?

The interpretation of data often depends on understanding “study design”—the plan for a statistical study and its implementation.12 Different designs are suited to answering different questions. Also, flaws in the data can undermine any statistical analysis, and data quality is often determined by study design.

In many cases, statistical studies are used to show causation. Do food additives cause cancer? Does capital punishment deter crime? Would additional disclosures

by any party to the litigation and that the expert receive a letter of engagement providing for these and other safeguards).

10. Id. at 167; cf. William W. Schwarzer, In Defense of “Automatic Disclosure in Discovery,” 27 Ga. L. Rev. 655, 658–59 (1993) (“[T]he lawyer owes a duty to the court to make disclosure of core information.”). The National Research Council also recommends that “if a party gives statistical data to different experts for competing analyses, that fact be disclosed to the testifying expert, if any.” The Evolving Role of Statistical Assessments as Evidence in the Courts, supra note 1, at 167.

11. See The Special Comm. on Empirical Data in Legal Decision Making, Recommendations on Pretrial Proceedings in Cases with Voluminous Data, reprinted in The Evolving Role of Statistical Assessments as Evidence in the Courts, supra note 1, app. F; see also David H. Kaye, Improving Legal Statistics, 24 Law & Soc’y Rev. 1255 (1990).

12. For introductory treatments of data collection, see, for example, David Freedman et al., Statistics (4th ed. 2007); Darrell Huff, How to Lie with Statistics (1993); David S. Moore & William I. Notz, Statistics: Concepts and Controversies (6th ed. 2005); Hans Zeisel, Say It with Figures (6th ed. 1985); Zeisel & Kaye, supra note 1.

in a securities prospectus cause investors to behave differently? The design of studies to investigate causation is the first topic of this section.13

Sample data can be used to describe a population. The population is the whole class of units that are of interest; the sample is the set of units chosen for detailed study. Inferences from the part to the whole are justified when the sample is representative. Sampling is the second topic of this section.

Finally, the accuracy of the data will be considered. Because making and recording measurements is an error-prone activity, error rates should be assessed and the likely impact of errors considered. Data quality is the third topic of this section.

A. Is the Study Designed to Investigate Causation?

When causation is the issue, anecdotal evidence can be brought to bear. So can observational studies or controlled experiments. Anecdotal reports may be of value, but they are ordinarily more helpful in generating lines of inquiry than in proving causation.14 Observational studies can establish that one factor is associ-

13. See also Michael D. Green et al., Reference Guide on Epidemiology, Section V, in this manual; Joseph Rodricks, Reference Guide on Exposure Science, Section E, in this manual.

14. In medicine, evidence from clinical practice can be the starting point for discovery of cause-and-effect relationships. For examples, see David A. Freedman, On Types of Scientific Enquiry, in The Oxford Handbook of Political Methodology 300 (Janet M. Box-Steffensmeier et al. eds., 2008). Anecdotal evidence is rarely definitive, and some courts have suggested that attempts to infer causation from anecdotal reports are inadmissible as unsound methodology under Daubert v. Merrell Dow Pharmaceuticals, Inc., 509 U.S. 579 (1993). See, e.g., McClain v. Metabolife Int’l, Inc., 401 F.3d 1233, 1244 (11th Cir. 2005) (“simply because a person takes drugs and then suffers an injury does not show causation. Drawing such a conclusion from temporal relationships leads to the blunder of the post hoc ergo propter hoc fallacy.”); In re Baycol Prods. Litig., 532 F. Supp. 2d 1029, 1039–40 (D. Minn. 2007) (excluding a meta-analysis based on reports to the Food and Drug Administration of adverse events); Leblanc v. Chevron USA Inc., 513 F. Supp. 2d 641, 650 (E.D. La. 2007) (excluding plaintiffs’ experts’ opinions that benzene causes myelofibrosis because the causal hypothesis “that has been generated by case reports…has not been confirmed by the vast majority of epidemiologic studies of workers being exposed to benzene and more generally, petroleum products.”), vacated, 275 Fed. App’x. 319 (5th Cir. 2008) (remanding for consideration of newer government report on health effects of benzene); cf. Matrixx Initiatives, Inc. v. Siracusano, 131 S. Ct. 1309, 1321 (2011) (concluding that adverse event reports combined with other information could be of concern to a reasonable investor and therefore subject to a requirement of disclosure under SEC Rule 10b-5, but stating that “the mere existence of reports of adverse events…says nothing in and of itself about whether the drug is causing the adverse events”). Other courts are more open to “differential diagnoses” based primarily on timing. E.g., Best v. Lowe’s Home Ctrs., Inc., 563 F.3d 171 (6th Cir. 2009) (reversing the exclusion of a physician’s opinion that exposure to propenyl chloride caused a man to lose his sense of smell because of the timing in this one case and the physician’s inability to attribute the change to anything else); Kaye et al., supra note 7, §§ 8.7.2 & 12.5.1. See also Matrixx Initiatives, supra, at 1322 (listing “a temporal relationship” in a single patient as one indication of “a reliable causal link”).

ated with another, but work is needed to bridge the gap between association and causation. Randomized controlled experiments are ideally suited for demonstrating causation.

Anecdotal evidence usually amounts to reports that events of one kind are followed by events of another kind. Typically, the reports are not even sufficient to show association, because there is no comparison group. For example, some children who live near power lines develop leukemia. Does exposure to electrical and magnetic fields cause this disease? The anecdotal evidence is not compelling because leukemia also occurs among children without exposure.15 It is necessary to compare disease rates among those who are exposed and those who are not. If exposure causes the disease, the rate should be higher among the exposed and lower among the unexposed. That would be association.

The next issue is crucial: Exposed and unexposed people may differ in ways other than the exposure they have experienced. For example, children who live near power lines could come from poorer families and be more at risk from other environmental hazards. Such differences can create the appearance of a cause-and-effect relationship. Other differences can mask a real relationship. Cause-and-effect relationships often are quite subtle, and carefully designed studies are needed to draw valid conclusions.

An epidemiological classic makes the point. At one time, it was thought that lung cancer was caused by fumes from tarring the roads, because many lung cancer patients lived near roads that recently had been tarred. This is anecdotal evidence. But the argument is incomplete. For one thing, most people—whether exposed to asphalt fumes or unexposed—did not develop lung cancer. A comparison of rates was needed. The epidemiologists found that exposed persons and unexposed persons suffered from lung cancer at similar rates: Tar was probably not the causal agent. Exposure to cigarette smoke, however, turned out to be strongly associated with lung cancer. This study, in combination with later ones, made a compelling case that smoking cigarettes is the main cause of lung cancer.16

A good study design compares outcomes for subjects who are exposed to some factor (the treatment group) with outcomes for other subjects who are

15. See National Research Council, Committee on the Possible Effects of Electromagnetic Fields on Biologic Systems (1997); Zeisel & Kaye, supra note 1, at 66–67. There are problems in measuring exposure to electromagnetic fields, and results are inconsistent from one study to another. For such reasons, the epidemiological evidence for an effect on health is inconclusive. National Research Council, supra; Zeisel & Kaye, supra; Edward W. Campion, Power Lines, Cancer, and Fear, 337 New Eng. J. Med. 44 (1997) (editorial); Martha S. Linet et al., Residential Exposure to Magnetic Fields and Acute Lymphoblastic Leukemia in Children, 337 New Eng. J. Med. 1 (1997); Gary Taubes, Magnetic Field-Cancer Link: Will It Rest in Peace?, 277 Science 29 (1997) (quoting various epidemiologists).

16. Richard Doll & A. Bradford Hill, A Study of the Aetiology of Carcinoma of the Lung, 2 Brit. Med. J. 1271 (1952). This was a matched case-control study. Cohort studies soon followed. See Green et al., supra note 13. For a review of the evidence on causation, see 38 International Agency for Research on Cancer (IARC), World Health Org., IARC Monographs on the Evaluation of the Carcinogenic Risk of Chemicals to Humans: Tobacco Smoking (1986).

not exposed (the control group). Now there is another important distinction to be made—that between controlled experiments and observational studies. In a controlled experiment, the investigators decide which subjects will be exposed and which subjects will go into the control group. In observational studies, by contrast, the subjects themselves choose their exposures. Because of self-selection, the treatment and control groups are likely to differ with respect to influential factors other than the one of primary interest. (These other factors are called lurking variables or confounding variables.)17 With the health effects of power lines, family background is a possible confounder; so is exposure to other hazards. Many confounders have been proposed to explain the association between smoking and lung cancer, but careful epidemiological studies have ruled them out, one after the other.

Confounding remains a problem to reckon with, even for the best observational research. For example, women with herpes are more likely to develop cervical cancer than other women. Some investigators concluded that herpes caused cancer: In other words, they thought the association was causal. Later research showed that the primary cause of cervical cancer was human papilloma virus (HPV). Herpes was a marker of sexual activity. Women who had multiple sexual partners were more likely to be exposed not only to herpes but also to HPV. The association between herpes and cervical cancer was due to other variables.18

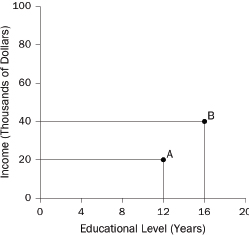

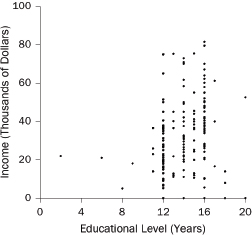

What are “variables?” In statistics, a variable is a characteristic of units in a study. With a study of people, the unit of analysis is the person. Typical variables include income (dollars per year) and educational level (years of schooling completed): These variables describe people. With a study of school districts, the unit of analysis is the district. Typical variables include average family income of district residents and average test scores of students in the district: These variables describe school districts.

When investigating a cause-and-effect relationship, the variable that represents the effect is called the dependent variable, because it depends on the causes. The variables that represent the causes are called independent variables. With a study of smoking and lung cancer, the independent variable would be smoking (e.g., number of cigarettes per day), and the dependent variable would mark the presence or absence of lung cancer. Dependent variables also are called outcome variables or response variables. Synonyms for independent variables are risk factors, predictors, and explanatory variables.

17. For example, a confounding variable may be correlated with the independent variable and act causally on the dependent variable. If the units being studied differ on the independent variable, they are also likely to differ on the confounder. The confounder—not the independent variable—could therefore be responsible for differences seen on the dependent variable.

18. For additional examples and further discussion, see Freedman et al., supra note 12, at 12–28, 150–52; David A. Freedman, From Association to Causation: Some Remarks on the History of Statistics, 14 Stat. Sci. 243 (1999). Some studies find that herpes is a “cofactor,” which increases risk among women who are also exposed to HPV. Only certain strains of HPV are carcinogenic.

2. Randomized controlled experiments

In randomized controlled experiments, investigators assign subjects to treatment or control groups at random. The groups are therefore likely to be comparable, except for the treatment. This minimizes the role of confounding. Minor imbalances will remain, due to the play of random chance; the likely effect on study results can be assessed by statistical techniques.19 The bottom line is that causal inferences based on well-executed randomized experiments are generally more secure than inferences based on well-executed observational studies.

The following example should help bring the discussion together. Today, we know that taking aspirin helps prevent heart attacks. But initially, there was some controversy. People who take aspirin rarely have heart attacks. This is anecdotal evidence for a protective effect, but it proves almost nothing. After all, few people have frequent heart attacks, whether or not they take aspirin regularly. A good study compares heart attack rates for two groups: people who take aspirin (the treatment group) and people who do not (the controls). An observational study would be easy to do, but in such a study the aspirin-takers are likely to be different from the controls. Indeed, they are likely to be sicker—that is why they are taking aspirin. The study would be biased against finding a protective effect. Randomized experiments are harder to do, but they provide better evidence. It is the experiments that demonstrate a protective effect.20

In summary, data from a treatment group without a control group generally reveal very little and can be misleading. Comparisons are essential. If subjects are assigned to treatment and control groups at random, a difference in the outcomes between the two groups can usually be accepted, within the limits of statistical error (infra Section IV), as a good measure of the treatment effect. However, if the groups are created in any other way, differences that existed before treatment may contribute to differences in the outcomes or mask differences that otherwise would become manifest. Observational studies succeed to the extent that the treatment and control groups are comparable—apart from the treatment.

The bulk of the statistical studies seen in court are observational, not experimental. Take the question of whether capital punishment deters murder. To conduct a randomized controlled experiment, people would need to be assigned randomly to a treatment group or a control group. People in the treatment group would know they were subject to the death penalty for murder; the

19. Randomization of subjects to treatment or control groups puts statistical tests of significance on a secure footing. Freedman et al., supra note 12, at 503–22, 545–63; see infra Section IV.

20. In other instances, experiments have banished strongly held beliefs. E.g., Scott M. Lippman et al., Effect of Selenium and Vitamin E on Risk of Prostate Cancer and Other Cancers: The Selenium and Vitamin E Cancer Prevention Trial (SELECT), 301 JAMA 39 (2009).

controls would know that they were exempt. Conducting such an experiment is not possible.

Many studies of the deterrent effect of the death penalty have been conducted, all observational, and some have attracted judicial attention. Researchers have catalogued differences in the incidence of murder in states with and without the death penalty and have analyzed changes in homicide rates and execution rates over the years. When reporting on such observational studies, investigators may speak of “control groups” (e.g., the states without capital punishment) or claim they are “controlling for” confounding variables by statistical methods.21 However, association is not causation. The causal inferences that can be drawn from analysis of observational data—no matter how complex the statistical technique—usually rest on a foundation that is less secure than that provided by randomized controlled experiments.

That said, observational studies can be very useful. For example, there is strong observational evidence that smoking causes lung cancer (supra Section II.A.1). Generally, observational studies provide good evidence in the following circumstances:

- The association is seen in studies with different designs, on different kinds of subjects, and done by different research groups.22 That reduces the chance that the association is due to a defect in one type of study, a peculiarity in one group of subjects, or the idiosyncrasies of one research group.

- The association holds when effects of confounding variables are taken into account by appropriate methods, for example, comparing smaller groups that are relatively homogeneous with respect to the confounders.23

- There is a plausible explanation for the effect of the independent variable; alternative explanations in terms of confounding should be less plausible than the proposed causal link.24

21. A procedure often used to control for confounding in observational studies is regression analysis. The underlying logic is described infra Section V.D and in Daniel L. Rubinfeld, Reference Guide on Multiple Regression, Section II, in this manual. But see Richard A. Berk, Regression Analysis: A Constructive Critique (2004); Rethinking Social Inquiry: Diverse Tools, Shared Standards (Henry E. Brady & David Collier eds., 2004); David A. Freedman, Statistical Models: Theory and Practice (2005); David A. Freedman, Oasis or Mirage, Chance, Spring 2008, at 59.

22. For example, case-control studies are designed one way and cohort studies another, with many variations. See, e.g., Leon Gordis, Epidemiology (4th ed. 2008); supra note 16.

23. The idea is to control for the influence of a confounder by stratification—making comparisons separately within groups for which the confounding variable is nearly constant and therefore has little influence over the variables of primary interest. For example, smokers are more likely to get lung cancer than nonsmokers. Age, gender, social class, and region of residence are all confounders, but controlling for such variables does not materially change the relationship between smoking and cancer rates. Furthermore, many different studies—of different types and on different populations—confirm the causal link. That is why most experts believe that smoking causes lung cancer and many other diseases. For a review of the literature, see International Agency for Research on Cancer, supra note 16.

24. A. Bradford Hill, The Environment and Disease: Association or Causation?, 58 Proc. Royal Soc’y Med. 295 (1965); Alfred S. Evans, Causation and Disease: A Chronological Journey 187 (1993). Plausibility, however, is a function of time and circumstances.

Thus, evidence for the causal link does not depend on observed associations alone.

Observational studies can produce legitimate disagreement among experts, and there is no mechanical procedure for resolving such differences of opinion. In the end, deciding whether associations are causal typically is not a matter of statistics alone, but also rests on scientific judgment. There are, however, some basic questions to ask when appraising causal inferences based on empirical studies:

- Was there a control group? Unless comparisons can be made, the study has little to say about causation.

- If there was a control group, how were subjects assigned to treatment or control: through a process under the control of the investigator (a controlled experiment) or through a process outside the control of the investigator (an observational study)?

- If the study was a controlled experiment, was the assignment made using a chance mechanism (randomization), or did it depend on the judgment of the investigator?

If the data came from an observational study or a nonrandomized controlled experiment,

- How did the subjects come to be in treatment or in control groups?

- Are the treatment and control groups comparable?

- If not, what adjustments were made to address confounding?

- Were the adjustments sensible and sufficient?25

4. Can the results be generalized?

Internal validity is about the specifics of a particular study: Threats to internal validity include confounding and chance differences between treatment and control groups. External validity is about using a particular study or set of studies to reach more general conclusions. A careful randomized controlled experiment on a large but unrepresentative group of subjects will have high internal validity but low external validity.

Any study must be conducted on certain subjects, at certain times and places, and using certain treatments. To extrapolate from the conditions of a study to more general conditions raises questions of external validity. For example, studies suggest that definitions of insanity given to jurors influence decisions in cases of incest. Would the definitions have a similar effect in cases of murder? Other studies indicate that recidivism rates for ex-convicts are not affected by provid-

25. Many courts have noted the importance of confounding variables. E.g., People Who Care v. Rockford Bd. of Educ., 111 F.3d 528, 537–38 (7th Cir. 1997) (educational achievement); Hollander v. Sandoz Pharms. Corp., 289 F.3d 1193, 1213 (10th Cir. 2002) (stroke); In re Proportionality Review Project (II), 757 A.2d 168 (N.J. 2000) (capital sentences).

ing them with temporary financial support after release. Would similar results be obtained if conditions in the labor market were different?

Confidence in the appropriateness of an extrapolation cannot come from the experiment itself. It comes from knowledge about outside factors that would or would not affect the outcome.26 Sometimes, several studies, each having different limitations, all point in the same direction. This is the case, for example, with studies indicating that jurors who approve of the death penalty are more likely to convict in a capital case.27 Convergent results support the validity of generalizations.

B. Descriptive Surveys and Censuses

We now turn to a second topic—choosing units for study. A census tries to measure some characteristic of every unit in a population. This is often impractical. Then investigators use sample surveys, which measure characteristics for only part of a population. The accuracy of the information collected in a census or survey depends on how the units are selected for study and how the measurements are made.28

1. What method is used to select the units?

By definition, a census seeks to measure some characteristic of every unit in a whole population. It may fall short of this goal, in which case one must ask

26. Such judgments are easiest in the physical and life sciences, but even here, there are problems. For example, it may be difficult to infer human responses to substances that affect animals. First, there are often inconsistencies across test species: A chemical may be carcinogenic in mice but not in rats. Extrapolation from rodents to humans is even more problematic. Second, to get measurable effects in animal experiments, chemicals are administered at very high doses. Results are extrapolated—using mathematical models—to the very low doses of concern in humans. However, there are many dose–response models to use and few grounds for choosing among them. Generally, different models produce radically different estimates of the “virtually safe dose” in humans. David A. Freedman & Hans Zeisel, From Mouse to Man: The Quantitative Assessment of Cancer Risks, 3 Stat. Sci. 3 (1988). For these reasons, many experts—and some courts in toxic tort cases—have concluded that evidence from animal experiments is generally insufficient by itself to establish causation. See, e.g., Bruce N. Ames et al., The Causes and Prevention of Cancer, 92 Proc. Nat’l Acad. Sci. USA 5258 (1995); National Research Council, Science and Judgment in Risk Assessment 59 (1994) (“There are reasons based on both biologic principles and empirical observations to support the hypothesis that many forms of biologic responses, including toxic responses, can be extrapolated across mammalian species, including Homo sapiens, but the scientific basis of such extrapolation is not established with sufficient rigor to allow broad and definitive generalizations to be made.”).

27. Phoebe C. Ellsworth, Some Steps Between Attitudes and Verdicts, in Inside the Juror 42, 46 (Reid Hastie ed., 1993). Nonetheless, in Lockhart v. McCree, 476 U.S. 162 (1986), the Supreme Court held that the exclusion of opponents of the death penalty in the guilt phase of a capital trial does not violate the constitutional requirement of an impartial jury.

28. See Shari Seidman Diamond, Reference Guide on Survey Research, Sections III, IV, in this manual.

whether the missing data are likely to differ in some systematic way from the data that are collected.29 The methodological framework of a scientific survey is different. With probability methods, a sampling frame (i.e., an explicit list of units in the population) must be created. Individual units then are selected by an objective, well-defined chance procedure, and measurements are made on the sampled units.

To illustrate the idea of a sampling frame, suppose that a defendant in a criminal case seeks a change of venue: According to him, popular opinion is so adverse that it would be difficult to impanel an unbiased jury. To prove the state of popular opinion, the defendant commissions a survey. The relevant population consists of all persons in the jurisdiction who might be called for jury duty. The sampling frame is the list of all potential jurors, which is maintained by court officials and is made available to the defendant. In this hypothetical case, the fit between the sampling frame and the population would be excellent.

In other situations, the sampling frame is more problematic. In an obscenity case, for example, the defendant can offer a survey of community standards.30 The population comprises all adults in the legally relevant district, but obtaining a full list of such people may not be possible. Suppose the survey is done by telephone, but cell phones are excluded from the sampling frame. (This is usual practice.) Suppose too that cell phone users, as a group, hold different opinions from landline users. In this second hypothetical, the poll is unlikely to reflect the opinions of the cell phone users, no matter how many individuals are sampled and no matter how carefully the interviewing is done.

Many surveys do not use probability methods. In commercial disputes involving trademarks or advertising, the population of all potential purchasers of a product is hard to identify. Pollsters may resort to an easily accessible subgroup of the population, for example, shoppers in a mall.31 Such convenience samples may be biased by the interviewer’s discretion in deciding whom to approach—a form of

29. The U.S. Decennial Census generally does not count everyone that it should, and it counts some people who should not be counted. There is evidence that net undercount is greater in some demographic groups than others. Supplemental studies may enable statisticians to adjust for errors and omissions, but the adjustments rest on uncertain assumptions. See Lawrence D. Brown et al., Statistical Controversies in Census 2000, 39 Jurimetrics J. 347 (2007); David A. Freedman & Kenneth W. Wachter, Methods for Census 2000 and Statistical Adjustments, in Social Science Methodology 232 (Steven Turner & William Outhwaite eds., 2007) (reviewing technical issues and litigation surrounding census adjustment in 1990 and 2000); 9 Stat. Sci. 458 (1994) (symposium presenting arguments for and against adjusting the 1990 census).

30. On the admissibility of such polls, see State v. Midwest Pride IV, Inc., 721 N.E.2d 458 (Ohio Ct. App. 1998) (holding one such poll to have been properly excluded and collecting cases from other jurisdictions).

31. E.g., Smith v. Wal-Mart Stores, Inc., 537 F. Supp. 2d 1302, 1333 (N.D. Ga. 2008) (treating a small mall-intercept survey as entitled to much less weight than a survey based on a probability sample); R.J. Reynolds Tobacco Co. v. Loew’s Theatres, Inc., 511 F. Supp. 867, 876 (S.D.N.Y. 1980) (questioning the propriety of basing a “nationally projectable statistical percentage” on a suburban mall intercept study).

selection bias—and the refusal of some of those approached to participate—non-response bias (infra Section II.B.2). Selection bias is acute when constituents write their representatives, listeners call into radio talk shows, interest groups collect information from their members, or attorneys choose cases for trial.32

There are procedures that attempt to correct for selection bias. In quota sampling, for example, the interviewer is instructed to interview so many women, so many older people, so many ethnic minorities, and the like. But quotas still leave discretion to the interviewers in selecting members of each demographic group and therefore do not solve the problem of selection bias.33

Probability methods are designed to avoid selection bias. Once the population is reduced to a sampling frame, the units to be measured are selected by a lottery that gives each unit in the sampling frame a known, nonzero probability of being chosen. Random numbers leave no room for selection bias.34 Such procedures are used to select individuals for jury duty. They also have been used to choose “bellwether” cases for representative trials to resolve issues in a large group of similar cases.35

32. E.g., Pittsburgh Press Club v. United States, 579 F.2d 751, 759 (3d Cir. 1978) (tax-exempt club’s mail survey of its members to show little sponsorship of income-producing uses of facilities was held to be inadmissible hearsay because it “was neither objective, scientific, nor impartial”), rev’d on other grounds, 615 F.2d 600 (3d Cir. 1980). Cf. In re Chevron U.S.A., Inc., 109 F.3d 1016 (5th Cir. 1997). In that case, the district court decided to try 30 cases to resolve common issues or to ascertain damages in 3000 claims arising from Chevron’s allegedly improper disposal of hazardous substances. The court asked the opposing parties to select 15 cases each. Selecting 30 extreme cases, however, is quite different from drawing a random sample of 30 cases. Thus, the court of appeals wrote that although random sampling would have been acceptable, the trial court could not use the results in the 30 extreme cases to resolve issues of fact or ascertain damages in the untried cases. Id. at 1020. Those cases, it warned, were “not cases calculated to represent the group of 3000 claimants.” Id. See infra note 35.

A well-known example of selection bias is the 1936 Literary Digest poll. After successfully predicting the winner of every U.S. presidential election since 1916, the Digest used the replies from 2.4 million respondents to predict that Alf Landon would win the popular vote, 57% to 43%. In fact, Franklin Roosevelt won by a landslide vote of 62% to 38%. See Freedman et al., supra note 12, at 334–35. The Digest was so far off, in part, because it chose names from telephone books, rosters of clubs and associations, city directories, lists of registered voters, and mail order listings. Id. at 335, A-20 n.6. In 1936, when only one household in four had a telephone, the people whose names appeared on such lists tended to be more affluent. Lists that overrepresented the affluent had worked well in earlier elections, when rich and poor voted along similar lines, but the bias in the sampling frame proved fatal when the Great Depression made economics a salient consideration for voters.

33. See Freedman et al., supra note 12, at 337–39.

34. In simple random sampling, units are drawn at random without replacement. In particular, each unit has the same probability of being chosen for the sample. Id. at 339–41. More complicated methods, such as stratified sampling and cluster sampling, have advantages in certain applications. In systematic sampling, every fifth, tenth, or hundredth (in mathematical jargon, every nth) unit in the sampling frame is selected. If the units are not in any special order, then systematic sampling is often comparable to simple random sampling.

35. E.g., In re Simon II Litig., 211 F.R.D. 86 (E.D.N.Y. 2002), vacated, 407 F.3d 125 (2d Cir. 2005), dismissed, 233 F.R.D. 123 (E.D.N.Y. 2006); In re Estate of Marcus Human Rights Litig., 910

2. Of the units selected, which are measured?

Probability sampling ensures that within the limits of chance (infra Section IV), the sample will be representative of the sampling frame. The question remains regarding which units actually get measured. When documents are sampled for audit, all the selected ones can be examined, at least in principle. Human beings are less easily managed, and some will refuse to cooperate. Surveys should therefore report nonresponse rates. A large nonresponse rate warns of bias, although supplemental studies may establish that nonrespondents are similar to respondents with respect to characteristics of interest.36

In short, a good survey defines an appropriate population, uses a probability method for selecting the sample, has a high response rate, and gathers accurate information on the sample units. When these goals are met, the sample tends to be representative of the population. Data from the sample can be extrapolated

F. Supp. 1460 (D. Haw. 1995), aff’d sub nom. Hilao v. Estate of Marcos, 103 F.3d 767 (9th Cir. 1996); Cimino v. Raymark Indus., Inc., 751 F. Supp. 649 (E.D. Tex. 1990), rev’d, 151 F.3d 297 (5th Cir. 1998); cf. In re Chevron U.S.A., Inc., 109 F.3d 1016 (5th Cir. 1997) (discussed supra note 32). Although trials in a suitable random sample of cases can produce reasonable estimates of average damages, the propriety of precluding individual trials raises questions of due process and the right to trial by jury. See Thomas E. Willging, Mass Torts Problems and Proposals: A Report to the Mass Torts Working Group (Fed. Judicial Ctr. 1999); cf. Wal-Mart Stores, Inc. v. Dukes, 131 S. Ct. 2541, 2560–61 (2011). The cases and the views of commentators are described more fully in David H. Kaye & David A. Freedman, Statistical Proof, in 1 Modern Scientific Evidence: The Law and Science of Expert Testimony § 6:16 (David L. Faigman et al. eds., 2009–2010).

36. For discussions of nonresponse rates and admissibility of surveys conducted for litigation, see Johnson v. Big Lots Stores, Inc., 561 F. Supp. 2d 567 (E.D. La. 2008) (fair labor standards); United States v. Dentsply Int’l, Inc., 277 F. Supp. 2d 387, 437 (D. Del. 2003), rev’d on other grounds, 399 F.3d 181 (3d Cir. 2005) (antitrust).

The 1936 Literary Digest election poll (supra note 32) illustrates the dangers in nonresponse. Only 24% of the 10 million people who received questionnaires returned them. Most of the respondents probably had strong views on the candidates and objected to President Roosevelt’s economic program. This self-selection is likely to have biased the poll. Maurice C. Bryson, The Literary Digest Poll: Making of a Statistical Myth, 30 Am. Statistician 184 (1976); Freedman et al., supra note 12, at 335—36. Even when demographic characteristics of the sample match those of the population, caution is indicated. See David Streitfeld, Shere Hite and the Trouble with Numbers, 1 Chance 26 (1988); Chamont Wang, Sense and Nonsense of Statistical Inference: Controversy, Misuse, and Subtlety 174–76 (1993).

In United States v. Gometz, 730 F.2d 475, 478 (7th Cir. 1984) (en banc), the Seventh Circuit recognized that “a low rate of response to juror questionnaires could lead to the underrepresentation of a group that is entitled to be represented on the qualified jury wheel.” Nonetheless, the court held that under the Jury Selection and Service Act of 1968, 28 U.S.C. §§ 1861–1878 (1988), the clerk did not abuse his discretion by failing to take steps to increase a response rate of 30%. According to the court, “Congress wanted to make it possible for all qualified persons to serve on juries, which is different from forcing all qualified persons to be available for jury service.” Gometz, 730 F.2d at 480. Although it might “be a good thing to follow up on persons who do not respond to a jury questionnaire,” the court concluded that Congress “was not concerned with anything so esoteric as nonresponse bias.” Id. at 479, 482; cf. In re United States, 426 F.3d 1 (1st Cir. 2005) (reaching the same result with respect to underrepresentation of African Americans resulting in part from nonresponse bias).

to describe the characteristics of the population. Of course, surveys may be useful even if they fail to meet these criteria. But then, additional arguments are needed to justify the inferences.

1. Is the measurement process reliable?

Reliability and validity are two aspects of accuracy in measurement. In statistics, reliability refers to reproducibility of results.37 A reliable measuring instrument returns consistent measurements. A scale, for example, is perfectly reliable if it reports the same weight for the same object time and again. It may not be accurate—it may always report a weight that is too high or one that is too low—but the perfectly reliable scale always reports the same weight for the same object. Its errors, if any, are systematic: They always point in the same direction.

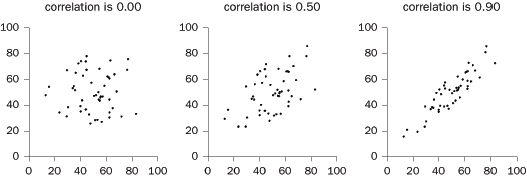

Reliability can be ascertained by measuring the same quantity several times; the measurements must be made independently to avoid bias. Given independence, the correlation coefficient (infra Section V.B) between repeated measurements can be used as a measure of reliability. This is sometimes called a test-retest correlation or a reliability coefficient.

A courtroom example is DNA identification. An early method of identification required laboratories to determine the lengths of fragments of DNA. By making independent replicate measurements of the fragments, laboratories determined the likelihood that two measurements differed by specified amounts.38 Such results were needed to decide whether a discrepancy between a crime sample and a suspect sample was sufficient to exclude the suspect.39

Coding provides another example. In many studies, descriptive information is obtained on the subjects. For statistical purposes, the information usually has to be reduced to numbers. The process of reducing information to numbers is called “coding,” and the reliability of the process should be evaluated. For example, in a study of death sentencing in Georgia, legally trained evaluators examined short summaries of cases and ranked them according to the defendant’s culpability.40

37. Courts often use “reliable” to mean “that which can be relied on” for some purpose, such as establishing probable cause or crediting a hearsay statement when the declarant is not produced for confrontation. Daubert v. Merrell Dow Pharms., Inc., 509 U.S. 579, 590 n.9 (1993), for example, distinguishes “evidentiary reliability” from reliability in the technical sense of giving consistent results. We use “reliability” to denote the latter.

38. See National Research Council, The Evaluation of Forensic DNA Evidence 139–41 (1996).

39. Id.; National Research Council, DNA Technology in Forensic Science 61–62 (1992). Current methods are discussed in David H. Kaye & George Sensabaugh, Reference Guide on DNA Identification Evidence, Section II, in this manual.

40. David C. Baldus et al., Equal Justice and the Death Penalty: A Legal and Empirical Analysis 49–50 (1990).

Two different aspects of reliability should be considered. First, the “within-observer variability” of judgments should be small—the same evaluator should rate essentially identical cases in similar ways. Second, the “between-observer variability” should be small—different evaluators should rate the same cases in essentially the same way.

2. Is the measurement process valid?

Reliability is necessary but not sufficient to ensure accuracy. In addition to reliability, validity is needed. A valid measuring instrument measures what it is supposed to. Thus, a polygraph measures certain physiological responses to stimuli, for example, in pulse rate or blood pressure. The measurements may be reliable. Nonetheless, the polygraph is not valid as a lie detector unless the measurements it makes are well correlated with lying.41

When there is an established way of measuring a variable, a new measurement process can be validated by comparison with the established one. Breathalyzer readings can be validated against alcohol levels found in blood samples. LSAT scores used for law school admissions can be validated against grades earned in law school. A common measure of validity is the correlation coefficient between the predictor and the criterion (e.g., test scores and later performance).42

Employment discrimination cases illustrate some of the difficulties. Thus, plaintiffs suing under Title VII of the Civil Rights Act may challenge an employment test that has a disparate impact on a protected group, and defendants may try to justify the use of a test as valid, reliable, and a business necessity.43 For validation, the most appropriate criterion variable is clear enough: job performance. However, plaintiffs may then turn around and challenge the validity of performance ratings. For reliability, administering the test twice to the same group of people may be impractical. Even if repeated testing is practical, it may be statistically inadvisable, because subjects may learn something from the first round of testing that affects their scores on the second round. Such “practice effects” are likely to compromise the independence of the two measurements, and independence is needed to estimate reliability. Statisticians therefore use internal evidence

41. See United States v. Henderson, 409 F.3d 1293, 1303 (11th Cir. 2005) (“while the physical responses recorded by a polygraph machine may be tested, ‘there is no available data to prove that those specific responses are attributable to lying.’”); National Research Council, The Polygraph and Lie Detection (2003) (reviewing the scientific literature).

42. As the discussion of the correlation coefficient indicates, infra Section V.B, the closer the coefficient is to 1, the greater the validity. For a review of data on test reliability and validity, see Paul R. Sackett et al., High-Stakes Testing in Higher Education and Employment: Appraising the Evidence for Validity and Fairness, 63 Am. Psychologist 215 (2008).

43. See, e.g., Washington v. Davis, 426 U.S. 229, 252 (1976); Albemarle Paper Co. v. Moody, 422 U.S. 405, 430–32 (1975); Griggs v. Duke Power Co., 401 U.S. 424 (1971); Lanning v. S.E. Penn. Transp. Auth., 308 F.3d 286 (3d Cir. 2002).

from the test itself. For example, if scores on the first half of the test correlate well with scores from the second half, then that is evidence of reliability.

A further problem is that test-takers are likely to be a select group. The ones who get the jobs are even more highly selected. Generally, selection attenuates (weakens) the correlations. There are methods for using internal measures of reliability to estimate test-retest correlations; there are other methods that correct for attenuation. However, such methods depend on assumptions about the nature of the test and the procedures used to select the test-takers and are therefore open to challenge.44

3. Are the measurements recorded correctly?

Judging the adequacy of data collection involves an examination of the process by which measurements are taken. Are responses to interviews coded correctly? Do mistakes distort the results? How much data are missing? What was done to compensate for gaps in the data? These days, data are stored in computer files. Cross-checking the files against the original sources (e.g., paper records), at least on a sample basis, can be informative.

Data quality is a pervasive issue in litigation and in applied statistics more generally. A programmer moves a file from one computer to another, and half the data disappear. The definitions of crucial variables are lost in the sands of time. Values get corrupted: Social security numbers come to have eight digits instead of nine, and vehicle identification numbers fail the most elementary consistency checks. Everybody in the company, from the CEO to the rawest mailroom trainee, turns out to have been hired on the same day. Many of the residential customers have last names that indicate commercial activity (“Happy Valley Farriers”). These problems seem humdrum by comparison with those of reliability and validity, but—unless caught in time—they can be fatal to statistical arguments.45

44. See Thad Dunning & David A. Freedman, Modeling Selection Effects, in Social Science Methodology 225 (Steven Turner & William Outhwaite eds., 2007); Howard Wainer & David Thissen, True Score Theory: The Traditional Method, in Test Scoring 23 (David Thissen & Howard Wainer eds., 2001).

45. See, e.g., Malletier v. Dooney & Bourke, Inc., 525 F. Supp. 2d 558, 630 (S.D.N.Y. 2007) (coding errors contributed “to the cumulative effect of the methodological errors” that warranted exclusion of a consumer confusion survey); EEOC v. Sears, Roebuck & Co., 628 F. Supp. 1264, 1304, 1305 (N.D. Ill. 1986) (“[E]rrors in EEOC’s mechanical coding of information from applications in its hired and nonhired samples also make EEOC’s statistical analysis based on this data less reliable.” The EEOC “consistently coded prior experience in such a way that less experienced women are considered to have the same experience as more experienced men” and “has made so many general coding errors that its data base does not fairly reflect the characteristics of applicants for commission sales positions at Sears.”), aff’d, 839 F.2d 302 (7th Cir. 1988). But see Dalley v. Mich. Blue Cross-Blue Shield, Inc., 612 F. Supp. 1444, 1456 (E.D. Mich. 1985) (“although plaintiffs show that there were some mistakes in coding, plaintiffs still fail to demonstrate that these errors were so generalized and so pervasive that the entire study is invalid.”).

In the law, a selection process sometimes is called “random,” provided that it does not exclude identifiable segments of the population. Statisticians use the term in a far more technical sense. For example, if we were to choose one person at random from a population, in the strict statistical sense, we would have to ensure that everybody in the population is chosen with exactly the same probability. With a randomized controlled experiment, subjects are assigned to treatment or control at random in the strict sense—by tossing coins, throwing dice, looking at tables of random numbers, or more commonly these days, by using a random number generator on a computer. The same rigorous definition applies to random sampling. It is randomness in the technical sense that provides assurance of unbiased estimates from a randomized controlled experiment or a probability sample. Randomness in the technical sense also justifies calculations of standard errors, confidence intervals, and p-values (infra Sections IV–V). Looser definitions of randomness are inadequate for statistical purposes.

III. How Have the Data Been Presented?

After data have been collected, they should be presented in a way that makes them intelligible. Data can be summarized with a few numbers or with graphical displays. However, the wrong summary can mislead.46Section III.A discusses rates or percentages and provides some cautionary examples of misleading summaries, indicating the kinds of questions that might be considered when summaries are presented in court. Percentages are often used to demonstrate statistical association, which is the topic of Section III.B. Section III.C considers graphical summaries of data, while Sections III.D and III.E discuss some of the basic descriptive statistics that are likely to be encountered in litigation, including the mean, median, and standard deviation.

A. Are Rates or Percentages Properly Interpreted?

1. Have appropriate benchmarks been provided?

The selective presentation of numerical information is like quoting someone out of context. Is a fact that “over the past three years,” a particular index fund of large-cap stocks “gained a paltry 1.9% a year” indicative of poor management? Considering that “the average large-cap value fund has returned just 1.3% a year,”

46. See generally Freedman et al., supra note 12; Huff, supra note 12; Moore & Notz, supra note 12; Zeisel, supra note 12.

a growth rate of 1.9% is hardly an indictment.47 In this example and many others, it is helpful to find a benchmark that puts the figures into perspective.

2. Have the data collection procedures changed?

Changes in the process of collecting data can create problems of interpretation. Statistics on crime provide many examples. The number of petty larcenies reported in Chicago more than doubled one year—not because of an abrupt crime wave, but because a new police commissioner introduced an improved reporting system.48 For a time, police officials in Washington, D.C., “demonstrated” the success of a law-and-order campaign by valuing stolen goods at $49, just below the $50 threshold then used for inclusion in the Federal Bureau of Investigation’s Uniform Crime Reports.49 Allegations of manipulation in the reporting of crime from one time period to another are legion.50

Changes in data collection procedures are by no means limited to crime statistics. Indeed, almost all series of numbers that cover many years are affected by changes in definitions and collection methods. When a study includes such time-series data, it is useful to inquire about changes and to look for any sudden jumps, which may signal such changes.

3. Are the categories appropriate?

Misleading summaries also can be produced by the choice of categories to be used for comparison. In Philip Morris, Inc. v. Loew’s Theatres, Inc.,51 and R.J. Reynolds Tobacco Co. v. Loew’s Theatres, Inc.,52 Philip Morris and R.J. Reynolds sought an injunction to stop the maker of Triumph low-tar cigarettes from running advertisements claiming that participants in a national taste test preferred Triumph to other brands. Plaintiffs alleged that claims that Triumph was a “national taste test winner” or Triumph “beats” other brands were false and misleading. An exhibit introduced by the defendant contained the data shown in Table 1.53 Only 14% + 22% = 36% of the sample preferred Triumph to Merit, whereas

47. Paul J. Lim, In a Downturn, Buy and Hold or Quit and Fold?, N.Y. Times, July 27, 2008.

48. James P. Levine et al., Criminal Justice in America: Law in Action 99 (1986) (referring to a change from 1959 to 1960).

49. D. Seidman & M. Couzens, Getting the Crime Rate Down: Political Pressure and Crime Reporting, 8 Law & Soc’y Rev. 457 (1974).

50. Michael D. Maltz, Missing UCR Data and Divergence of the NCVS and UCR Trends, in Understanding Crime Statistics: Revisiting the Divergence of the NCVS and UCR 269, 280 (James P. Lynch & Lynn A. Addington eds., 2007) (citing newspaper reports in Boca Raton, Atlanta, New York, Philadelphia, Broward County (Florida), and Saint Louis); Michael Vasquez, Miami Police: FBI: Crime Stats Accurate, Miami Herald, May 1, 2008.

51. 511 F. Supp. 855 (S.D.N.Y. 1980).

52. 511 F. Supp. 867 (S.D.N.Y. 1980).

53. Philip Morris, 511 F. Supp. at 866.

29% + 11% = 40% preferred Merit to Triumph. By selectively combining categories, however, the defendant attempted to create a different impression. Because 24% found the brands to be about the same, and 36% preferred Triumph, the defendant claimed that a clear majority (36% + 24% = 60%) found Triumph “as good [as] or better than Merit.”54 The court resisted this chicanery, finding that defendant’s test results did not support the advertising claims.55

Table 1. Data Used by a Defendant to Refute Plaintiffs’ False Advertising Claim

| Triumph | Triumph | Triumph | Triumph | Triumph | |

| Much | Somewhat | About the | Somewhat | Much | |

| Better | Better | Same | Worse | Worse | |

| Than Merit | Than Merit | Than Merit | Than Merit | Than Merit | |

| Number | 45 | 73 | 77 | 93 | 36 |

| Percentage | 14 | 22 | 24 | 29 | 11 |

There was a similar distortion in claims for the accuracy of a home pregnancy test. The manufacturer advertised the test as 99.5% accurate under laboratory conditions. The data underlying this claim are summarized in Table 2.

Table 2. Home Pregnancy Test Results

| Actually Pregnant | Actually not Pregnant | ||||

| Test says pregnant | 197 | 0 | |||

| Test says not pregnant | 1 | 2 | |||

| Total | 198 | 2 | |||

Table 2 does indicate that only one error occurred in 200 assessments, or 99.5% overall accuracy, but the table also shows that the test can make two types of errors: It can tell a pregnant woman that she is not pregnant (a false negative), and it can tell a woman who is not pregnant that she is (a false positive). The reported 99.5% accuracy rate conceals a crucial fact—the company had virtually no data with which to measure the rate of false positives.56

54. Id.

55. Id. at 856–57.

56. Only two women in the sample were not pregnant; the test gave correct results for both of them. Although a false-positive rate of 0 is ideal, an estimate based on a sample of only two women is not. These data are reported in Arnold Barnett, How Numbers Can Trick You, Tech. Rev., Oct. 1994, at 38, 44–45.

4. How big is the base of a percentage?

Rates and percentages often provide effective summaries of data, but these statistics can be misinterpreted. A percentage makes a comparison between two numbers: One number is the base, and the other number is compared to that base. Putting them on the same base (100) makes it easy to compare them.

When the base is small, however, a small change in absolute terms can generate a large percentage gain or loss. This could lead to newspaper headlines such as “Increase in Thefts Alarming,” even when the total number of thefts is small.57 Conversely, a large base will make for small percentage increases. In these situations, actual numbers may be more revealing than percentages.

Finally, there is the issue of which numbers to compare. Researchers sometimes choose among alternative comparisons. It may be worthwhile to ask why they chose the one they did. Would another comparison give a different view? A government agency, for example, may want to compare the amount of service now being given with that of earlier years—but what earlier year should be the baseline? If the first year of operation is used, a large percentage increase should be expected because of startup problems. If last year is used as the base, was it also part of the trend, or was it an unusually poor year? If the base year is not representative of other years, the percentage may not portray the trend fairly. No single question can be formulated to detect such distortions, but it may help to ask for the numbers from which the percentages were obtained; asking about the base can also be helpful.58

B. Is an Appropriate Measure of Association Used?

Many cases involve statistical association. Does a test for employee promotion have an exclusionary effect that depends on race or gender? Does the incidence of murder vary with the rate of executions for convicted murderers? Do consumer purchases of a product depend on the presence or absence of a product warning? This section discusses tables and percentage-based statistics that are frequently presented to answer such questions.59

Percentages often are used to describe the association between two variables. Suppose that a university alleged to discriminate against women in admitting

57. Lyda Longa, Increase in Thefts Alarming, Daytona News-J. June 8, 2008 (reporting a 35% increase in armed robberies in Daytona Beach, Florida, in a 5-month period, but not indicating whether the number had gone up by 6 (from 17 to 23), by 300 (from 850 to 1150), or by some other amount).

58. For assistance in coping with percentages, see Zeisel, supra note 12, at 1–24.

59. Correlation and regression are discussed infra Section V.

students consists of only two colleges—engineering and business. The university admits 350 out of 800 male applicants; by comparison, it admits only 200 out of 600 female applicants. Such data commonly are displayed as in Table 3.60

As Table 3 indicates, 350/800 = 44% of the males are admitted, compared with only 200/600 = 33% of the females. One way to express the disparity is to subtract the two percentages: 44% − 33% = 11 percentage points. Although such subtraction is commonly seen in jury discrimination cases,61 the difference is inevitably small when the two percentages are both close to zero. If the selection rate for males is 5% and that for females is 1%, the difference is only 4 percentage points. Yet, females have only one-fifth the chance of males of being admitted, and that may be of real concern.

Table 3. Admissions by Gender

| Decision | Male | Female | Total | ||

| Admit | 350 | 200 | 550 | ||

| Deny | 450 | 400 | 850 | ||

| Total | 800 | 600 | 1400 | ||

For Table 3, the selection ratio (used by the Equal Employment Opportunity Commission in its “80% rule”) is 33/44 = 75%, meaning that, on average, women have 75% the chance of admission that men have.62 However, the selection ratio has its own problems. In the last example, if the selection rates are 5% and 1%, then the exclusion rates are 95% and 99%. The ratio is 99/95 = 104%, meaning that females have, on average, 104% the risk of males of being rejected. The underlying facts are the same, of course, but this formulation sounds much less disturbing.

60. A table of this sort is called a “cross-tab” or a “contingency table.” Table 3 is “two-by-two” because it has two rows and two columns, not counting rows or columns containing totals.

61. See, e.g., State v. Gibbs, 758 A.2d 327, 337 (Conn. 2000); Primeaux v. Dooley, 747 N.W.2d 137, 141 (S.D. 2008); D.H. Kaye, Statistical Evidence of Discrimination in Jury Selection, in Statistical Methods in Discrimination Litigation 13 (David H. Kaye & Mikel Aickin eds., 1986).

62. A procedure that selects candidates from the least successful group at a rate less than 80% of the rate for the most successful group “will generally be regarded by the Federal enforcement agencies as evidence of adverse impact.” EEOC Uniform Guidelines on Employee Selection Procedures, 29 C.F.R. § 1607.4(D) (2008). The rule is designed to help spot instances of substantially discriminatory practices, and the commission usually asks employers to justify any procedures that produce selection ratios of 80% or less.

The analogous statistic used in epidemiology is called the relative risk. See Green et al., supra note 13, Section III.A. Relative risks are usually quoted as decimals; for example, a selection ratio of 75% corresponds to a relative risk of 0.75.

The odds ratio is more symmetric. If 5% of male applicants are admitted, the odds on a man being admitted are 5/95 = 1/19; the odds on a woman being admitted are 1/99. The odds ratio is (1/99)/(1/19) = 19/99. The odds ratio for rejection instead of acceptance is the same, except that the order is reversed.63 Although the odds ratio has desirable mathematical properties, its meaning may be less clear than that of the selection ratio or the simple difference.

Data showing disparate impact are generally obtained by aggregating—putting together—statistics from a variety of sources. Unless the source material is fairly homogeneous, aggregation can distort patterns in the data. We illustrate the problem with the hypothetical admission data in Table 3. Applicants can be classified not only by gender and admission but also by the college to which they applied, as in Table 4.

Table 4. Admissions by Gender and College

| Decision | Engineering | Business | ||

| Male | Female | Male | Female | |

| Admit | 300 | 100 | 50 | 100 |

| Deny | 300 | 100 | 150 | 300 |

The entries in Table 4 add up to the entries in Table 3. Expressed in a more technical manner, Table 3 is obtained by aggregating the data in Table 4. Yet there is no association between gender and admission in either college; men and women are admitted at identical rates. Combining two colleges with no association produces a university in which gender is associated strongly with admission. The explanation for this paradox is that the business college, to which most of the women applied, admits relatively few applicants. It is easier to be accepted at the engineering college, the college to which most of the men applied. This example illustrates a common issue: Association can result from combining heterogeneous statistical material.64

63. For women, the odds on rejection are 99 to 1; for men, 19 to 1. The ratio of these odds is 99/19. Likewise, the odds ratio for an admitted applicant being a man as opposed to a denied applicant being a man is also 99/19.

64. Tables 3 and 4 are hypothetical, but closely patterned on a real example. See P.J. Bickel et al., Sex Bias in Graduate Admissions: Data from Berkeley, 187 Science 398 (1975). The tables are an instance of Simpson’s Paradox.

C. Does a Graph Portray Data Fairly?

Graphs are useful for revealing key characteristics of a batch of numbers, trends over time, and the relationships among variables.

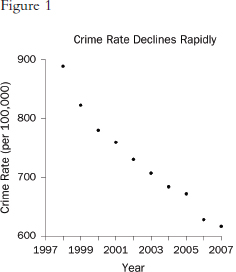

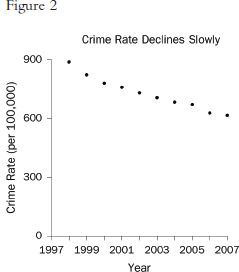

Graphs that plot values over time are useful for seeing trends. However, the scales on the axes matter. In Figure 1, the rate of all crimes of domestic violence in Florida (per 100,000 people) appears to decline rapidly over the 10 years from 1998 through 2007; in Figure 2, the same rate appears to drop slowly.65 The moral is simple: Pay attention to the markings on the axes to determine whether the scale is appropriate.

2. How are distributions displayed?

A graph commonly used to display the distribution of data is the histogram. One axis denotes the numbers, and the other indicates how often those fall within

65. Florida Statistical Analysis Center, Florida Department of Law Enforcement, Florida’s Crime Rate at a Glance, available at http://www.fdle.state.fl.us/FSAC/Crime_Trends/domestic_violence/index.asp. The data are from the Florida Uniform Crime Report statistics on crimes ranging from simple stalking and forcible fondling to murder and arson. The Web page with the numbers graphed in Figures 1 and 2 is no longer posted, but similar data for all violent crime is available at http://www.fdle.state.fl.us/FSAC/Crime_Trends/Violent-Crime.aspx.

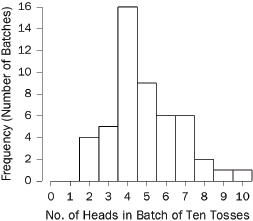

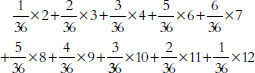

specified intervals (called “bins” or “class intervals”). For example, we flipped a quarter 10 times in a row and counted the number of heads in this “batch” of 10 tosses. With 50 batches, we obtained the following counts:66

7 7 5 6 8 4 2 3 6 5 4 3 4 7 4 6 8 4 7 4 7 4 5 4 3

4 4 2 5 3 5 4 2 4 4 5 7 2 3 5 4 6 4 9 10 5 5 6 6 4

The histogram is shown in Figure 3.67 A histogram shows how the data are distributed over the range of possible values. The spread can be made to appear larger or smaller, however, by changing the scale of the horizontal axis. Likewise, the shape can be altered somewhat by changing the size of the bins.68 It may be worth inquiring how the analyst chose the bin widths.

Figure 3. Histogram showing how frequently various numbers of heads appeared in 50 batches of 10 tosses of a quarter.

66. The coin landed heads 7 times in the first 10 tosses; by coincidence, there were also 7 heads in the next 10 tosses; there were 5 heads in the third batch of 10 tosses; and so forth.

67. In Figure 3, the bin width is 1. There were no 0s or 1s in the data, so the bars over 0 and 1 disappear. There is a bin from 1.5 to 2.5; the four 2s in the data fall into this bin, so the bar over the interval from 1.5 to 2.5 has height 4. There is another bin from 2.5 to 3.5, which catches five 3s; the height of the corresponding bar is 5. And so forth.

All the bins in Figure 3 have the same width, so this histogram is just like a bar graph. However, data are often published in tables with unequal intervals. The resulting histograms will have unequal bin widths; bar heights should be calculated so that the areas (height × width) are proportional to the frequencies. In general, a histogram differs from a bar graph in that it represents frequencies by area, not height. See Freedman et al., supra note 12, at 31–41.

68. As the width of the bins decreases, the graph becomes more detailed, but the appearance becomes more ragged until finally the graph is effectively a plot of each datum. The optimal bin width depends on the subject matter and the goal of the analysis.

D. Is an Appropriate Measure Used for the Center of a Distribution?