Program Monitoring and Research

Anticipating the need for data collection and research to support the process of updating the essential health benefits (EHB), the committee recommends that planning and development of a research strategy begin now. The Department of Health and Human Services (HHS) in collaboration (1) with groups such as the National Association of Insurance Commissioners (NAIC) can help promote standardization to enhance comparisons of state-based data (such as categories of benefits, design elements, medical necessity processes, and appeals) and (2) HHS component agencies, the Department of Labor (DOL), and others can develop a complementary research agenda to enable updates to the EHB to be more specific, evidence-based, and value-promoting. This chapter explores some aspects of data collection for program monitoring and development of a research agenda, with a call for development of the infrastructure to support the strategy and public access to data for analytic purposes.

An effective strategy for updating the essential health benefits (EHB) will require that HHS be prepared to respond to the changing health care environment. Over time, new medical care technologies will be introduced, clinical research will gain new insights, provider practices and patient needs will change, what is affordable will have to be considered, and societal preferences will shift. Furthermore, the design of insurance company products, employer offer rates, and consumer preferences will all affect the future private insurance landscape. An effective EHB updating process must be able to identify the key changes that are occurring and develop approaches to respond to those changes. This will require coordinated and thoughtful monitoring and research.

The Institute of Medicine (IOM) committee draws a distinction between monitoring—efforts to describe what is occurring as the EHB are implemented into insurance offerings—and research—efforts to create generalizable knowledge about the implications of the varied responses in markets across the states. Additionally, emerging evidence on medical advances needs to be evaluated to determine whether specific changes to the EHB definition are warranted, that is, whether new evidence changes the relative value of a particular drug, device, service, or category of care delivery. The committee envisions that this type of monitoring and research will be used directly by the Secretary in considering updates to the EHB. The committee calls on the Secretary to ensure that the necessary infrastructure is in place to answer the key questions.

The committee recognizes that the Patient Protection and Affordable Care Act (ACA) contains numerous elements that require monitoring, research, and oversight, such as the implementation of health insurance exchanges or expansion of the traditional Medicaid program. The EHB are just one of many areas requiring attention by HHS.

Although the committee focuses here on the monitoring and research needs relevant to the EHB, it recognizes that the optimal strategy within HHS is likely to be a coordinated approach across all areas. With respect to the EHB, monitoring and research can

• Provide input into the process of updating the EHB,

• Contribute to addressing questions in the Section 1302(b)(4)(G) required reports to Congress and the public,

• Monitor for discriminatory practices and balance as a result of initial EHB definition and its implementation, and

• Assess the impact of the EHB on consumers, employers, health care providers, insurers, and governments at the state and local levels.

Congress, in Section 1302 of the ACA in particular, calls out an interest in any problems related to access, methods for incorporating evidence of medical advances into the EHB, ideas about how best to close any gaps observed in access or changes to evidence, and assessing the cost implications of potential changes to the EHB. The committee also believes that HHS will want to know whether initial guidance on the EHB is achieving an appropriate balance between cost and coverage; how specific design elements and medical necessity determination processes can affect care delivered, outcomes, and value; whether rates of participation by consumers, employers, and insurers are affected by the EHB; how the EHB package can be updated to become more evidence-based and value-promoting; and what impact the composition of exchange participation has on premiums (e.g., greater or lesser participation by employers and individuals).

SETTING A RESEARCH FRAMEWORK FOR DATA COLLECTION AND ANALYSIS

The committee believes the monitoring and research strategy related to the EHB should be articulated thoughtfully as soon as possible to enhance planning efforts, allocate necessary resources, and align priorities for collecting comparable data among different stakeholders. A systematic pursuit of this strategy is consistent with creating a learning health care system (IOM, 2007, 2011). Such a strategy should engage stakeholders in ensuring that the right questions are being asked, that the purposes for the collected data are clear, that modifications to the EHB are justified and fair, that the EHB are becoming increasingly evidence-based over time, and that the country is spending its tax dollars (and enrollees their premium dollars) effectively and efficiently.

State oversight is important during approval of plan offerings, implementation, and appeals. The state and federal health insurance exchanges are responsible for determining which health plans are qualified to operate in the exchange and can serve as a primary data source for what is happening across states and over time in response to the Secretary’s guidance. The EHB are also required for incorporation in all non-grandfathered individual and small employer policies offered outside the exchange; such plan oversight would be outside of exchange operations, but under the aegis of state insurance commissioners. Thus, oversight responsibility cannot lay solely with exchanges. Ideally, state departments of insurance will actively take on the responsibility to protect against adverse selection and discriminatory practices in their jurisdiction; it important that health plans, in and out of the exchanges, are complying with requirements of the EHB package and not using benefit design and administration to risk-select or deny access to care. Additionally, the EHB are to be incorporated in new Medicaid benchmark, benchmark-equivalent, and state basic health insurance instruments; these will be under a separate state agency, also reporting to Centers for Medicare & Medicaid Services (CMS).

Leveraging these potential state-level data resources will require providing clarity and standardization in data collection (e.g., categorization of included benefits; descriptions of plan limits, types of treatments and conditions that are the subject of appeals), which will in turn improve opportunities for the analysis of comparative data. State collection and reporting of data can be a condition of states receiving federal funding to establish the exchanges; notably though, federal funding of state exchanges is time limited. Insurer reporting of plan content, however, will remain a condition of being certified a qualified health plan. This information will also provide insight beyond the exchange because of the requirement for insurers to offer the same plans outside as inside. Insurers will likely be

contracting with one or more external independent review organizations; these could be required to report appeals data in specific ways. If state regulatory systems will not already compile and publicly report appeals data in a way that is useful for evaluating EHB implementation and nondiscrimination, then additional support may be necessary for data provided to the Secretary. There is urgency in having guidance on required data collection for exchanges, regulatory agencies, and insurance companies. These expectations must be incorporated into planning in preparation for operations starting on January 1, 2014.

Tradeoffs are inevitable in setting the degree of data mining against the available resources (both cost and administrative burden) to collect and analyze data in order to ensure that implementation is achieving its goals and consumers are protected. Thus, priorities need to be set for available state and federal spending on monitoring and analysis. Some of the data collection and reporting would be part of normal state operations, but others, as noted above, might require additional resources. The exchanges and state insurance regulators will not be the only repositories of pertinent data; other state and federal sources might have to be mined to assess factors such as the size of the uninsured population, consumer satisfaction, health care utilization, quality of care, health status, and employer characteristics.

In Recommendation 2a, the committee calls on the Secretary to establish a framework for data collection and research; this framework should be developed with advice from the National Benefits Advisory Council (Recommendation 5 in Chapter 9).

Recommendation 2a: By January 1, 2013, the Secretary should establish a framework for obtaining and analyzing data necessary for monitoring implementation and updating of the EHB. The framework should account for

• Changes related to providers such as payment rates, contracting mechanisms, financial incentives, and scope and organization of practice;

• Changes related to patients and consumers such as demographics, health status, disease burden, and problems with access; and

• Changes related to health plans such as characteristics of plans (inclusions, exclusions, limitations), cost-sharing practices, patterns of enrollment and disenrollment, network configuration, medical management programs (including medical necessity determination processes), value-based insurance design, types of external appeals, risk selection, solvency, and impact of the ACA-mandated limits on deductibles, co-payments, and out-of-pocket spending on the ability of plans to offer acceptable products.

Creating a Responsive and Efficient Research Infrastructure

Furthermore, the committee recommends that the Secretary establish an infrastructure for this enterprise by engaging appropriate HHS components (e.g., CMS, Agency for Healthcare Research and Quality [AHRQ], Food and Drug Administration [FDA], National Institutes of Health, Office of the Assistant Secretary for Planning and Evaluation, Centers for Disease Control and Prevention) and other federal agencies (e.g., DOL, Office of Personnel Management, U.S. Census Bureau) and coordinating their expertise, data, and resources to fulfill research needs within and outside government (IOM, 2002, 2009a). CMS is the likely repository for exchange data as well as data from benchmark plans. Others such as the Kaiser Family Foundation and HRET Employer Health Benefits Annual Survey monitor employer benefit changes over time (KFF and HRET, 2010). Additionally, these activities will generate many questions of comparative effectiveness (IOM, 2009b). Close collaboration with the Patient-Centered Outcomes Research Institute (PCORI) will help to ensure that its research agenda considers these questions.

The Secretary must make the essential information needed for research by outside parties, including the standardized data collected from the EHB implementation processes as well as utilization and outcomes data from federal payers (Medicare, Medicaid), available in a timely, open, and streamlined way, just as HHS has sponsored access to other departmental data (e.g., http://www.health.data.gov). Private insurers must be encouraged and incentivized to collaborate in a similarly streamlined and open fashion. Strict attention to issues of data security

and confidentiality, including compliance with all federal and state laws and regulations, must be maintained throughout the process.

To ensure research is conducted in accordance with the highest scientific standards, the committee suggests that the Secretary charge the Agency for Healthcare Research and Quality with responsibility for managing the processes of soliciting, reviewing, funding, and overseeing this research agenda.

Recommendation 2b: The Secretary should establish an appropriate infrastructure for implementing this framework that engages and coordinates the efforts of all of the appropriate HHS and other federal in producing and analyzing the necessary data in a timely manner. These data should be made easily accessible and affordable for public use.

PROGRAM MONITORING AND RESEARCH

The committee offers some guidance for the implementation of these recommendations in terms of data collection via the exchanges and other sources, as well as some illustrative research questions.

Learning from the Exchanges and State Regulators

The EHB package will become a standard setter for the content of health insurance beyond the health exchange, but HHS can learn from those operating exchanges and from state regulators how the EHB are incorporated into health insurance products, what benefit design components are utilized to meet the coverage and premium requirements, how consumer preferences in the market (e.g., for high deductible plans) would relate to the scope and inclusiveness of the benefit package and its associated benefit design and premiums, and through the benefit determination and appeals process, concerns about access to specific benefits or for diverse segments of the population. Standardized approaches to defining data elements and collecting data from insurers will be essential for HHS to be able to analyze trends. The health insurance exchanges will also be better able to understand and improve the benefit design and administration processes if they can compare their experiences with those of other exchanges.

A second objective for the exchanges is to determine whether consumers understand the choices they are being offered. The ACA calls for designing plan materials that are simple and easy for most people to understand.1 A key aspect of the information that is to be communicated in these materials is the scope of benefits, inclusions and exclusions, and premiums.

Improving Standardization

The EHB definition process offers HHS an opportunity to lead the standardization of categories of benefits and to increase the specificity with which inclusions and exclusions of services are presented. The methods of data collection and EHB articulation can and will set standards for commercial industry practices—which will be subject to intense scrutiny and pressure. Like the DOL, the committee found it difficult to make side-by-side comparisons among plans because of a lack of consistency in categories and degree of specificity. This is the same challenge faced by consumers who are trying to choose between health plans and was likely part of the impetus for the ACA requiring work to improve consumers’ ability to understand their choices.

If reporting by the 10 categories is considered desirable (e.g., utilization or expenditures patterns), then several issues arise. First, the EHB list would have to identify what services fall within each category. Second, the 10 ACA categories do not match other payer methodologies, such as those used by Medicare or commercial providers. For example, insurance contracts, provider agreements, and current data tracking typically are based on location (e.g., inpatient vs. ambulatory) and type of provider (e.g., hospital vs. physician). However, the 10 EHB categories also include treatment-, condition-, and age-based categories; as a result, services and items will bridge

1 Patient Protection and Affordable Care Act of 2010 as amended. § 2715 of the Public Health Service Act, 111th Cong., 2d sess. [42 U.S.C. 300gg–15].

multiple categories. It may prove difficult within the current coding conventions used by public and private payers to categorize services offered or delivered into the 10 EHB categories reliably.

The Secretary, in conjunction with the National Benefits Advisory Council (NBAC), should engage state insurance commissioners and the National Association of Insurance Commissioners (NAIC) to facilitate setting standards for collection and uniform reporting of state-based data from subscriber (enrollee) contracts approved by states, just as HHS is working with insurance commissioners, health plans, and actuaries to standardize the collection of premium information and the disclosure of insurance contract information to consumers.2

Types of State-Based Data for Oversight

States currently review subscriber contracts (or “forms”) to ascertain whether licensed health insurers are complying with state laws. The scope and nature of those reviews vary by state. HHS should work with states to standardize and collect information from these contracts, including at a minimum

1. Benefits covered and excluded at the plan level, with particular attention to the level of specificity at which those services and items are described, future approaches to categorization as specificity increases, and how the specificity of coverage varies across insurers now and over time;

2. Objective limits to services within covered categories—usually defined as service limits (e.g., number of office visits) to reveal general norms;

3. Exception language;

4. Coverage of new approaches to prevention, diagnosis, treatment, and management;

5. Categories and levels of cost sharing and state or health insurer innovations such as value-based insurance design;

6. Terms and conditions including medical necessity,3 network limitation, and prior authorization; and

7. Rates of review and approval related to medical necessity, and specification of types of medical necessity review (e.g., by condition, treatment, coverage categories).

Items 1 through 4 will assist the Secretary in updating the EHB definition and ensuring balance and nondiscrimination by describing current variation in EHB implementation, coverage limits, exceptions, and trends in covering new technologies or other interventions. Items 5 and 6 will make clearer the landscape in benefit design, an important consideration in understanding trends in premium prices related to the EHB and measuring the impact of such benefit designs. Although the Secretary is not to preclude insurers from using various utilization management techniques, there is a requirement in Section 1302 to ensure that coverage decisions, reimbursement rates, incentive programs, or designs of benefits are not discriminatory on the basis of age, disability, or expected length of life, while Section 1557 explicitly pertains to nondiscrimination based on race, national origin, and gender. Furthermore, item 7 uses the strengthened appeals process in the ACA as a source of information for monitoring the various nondiscrimination factors in the required elements for consideration of Section 1302. Finally, to the extent feasible, any information collected in the monitoring and oversight process should include demographic data so that disparities and discrimination can be identified and rectified. Box 2-2 in Chapter 2 additionally elaborates on the type of data that should be collected from plans, including quality, utilization, and outcomes data to fully understand benefit design as implemented.

2 The Center for Consumer Information and Insurance Oversight (CCIIO) oversees ACA Consumer Assistance Program Grants, grants to assist states in establishing, expanding, or supporting consumer assistance programs. These grant funds must be used to support activities such as assisting consumers in filing complaints and appeals, collecting data on problems and inquiries encountered by consumers, educating consumers regarding their rights and responsibilities in health plans and insurance coverage, and resolving problems with obtaining the tax credits specified by the law (CCIIO, 2010). NAIC has an online portal, Insure U, which provides consumers with an array of easily understandable resources for assistance in purchasing health insurance (NAIC, 2011).

3 Ideally, data collection should include data on all medical necessity determinations, or at least on all denials, not just those that result in an appeal, but that may depend on the willingness of insurers to share such data and state requirements. Insurers elect to have a different number of review levels internally; Colorado requires public reporting on all internal second level reviews (State of Colorado, 2010).

The ACA leaves most oversight of health plans to the states, as is true today. As such, the exchanges and regulators are likely to derive considerable utility themselves from the information collected in each of these items. The Secretary will provide a significant service by collecting and compiling this information and supplying analyses back to these local entities. This work should be closely coordinated with other work set forth by the ACA and currently being done by HHS in two areas:

1. Efforts by the HHS Center for Consumer Information and Insurance Oversight (CCIIO), the NAIC, and state insurance departments to articulate standards for disclosure to consumers of subscriber contract elements. These standards should incorporate elements required for EHB specification.4

2. The monitoring of state-based exchanges to be conducted by CCIIO for purposes other than EHB definition, such as governance and administrative operations, certification of qualified health plans, the development of plan levels (e.g., gold, silver metal levels), and risk adjustment. Exchanges should not have to deal with multiple monitoring requests from multiple HHS program areas.

Standardization of terms and classification of services into categories is designed to improve comparisons. The committee anticipates that innovation in insurance products will continue and that classifying and analyzing these changes will be facilitated by the use of standardized definitions. Over time, some innovations may require updates to the nature and detail of the information being collected. As with the EHB, the committee does not believe the research and monitoring enterprises will be static.

External Appeals Information

Although the states are charged with monitoring and taking action with respect to appeals, this information would be useful to the Secretary in signaling whether frequently denied treatments indicate uncertainty due to a lack of evidence, changing medical indications that may require study, or lack of clarity about whether the treatment is included as part of the EHB. In addition, the committee recommends that data on appeals serve as the best approach for monitoring the “required elements for consideration” for nondiscrimination. Given its charge, the IOM committee was most interested in understanding coverage denials and complaints that, in turn, would inform both potential lack of access and questions about the available evidence base for services.

A March 2011 Government Accountability Office (GAO) report evaluated the current national availability of data on coverage denial rates (preauthorizations, denials of payment after service delivered) and found that there is “not yet any comprehensive national information on the extent to which coverage for medical services is being denied when consumers seek care” (GAO, 2011, p. 1). What data were available show that denials are “frequently reversed in the consumer’s favor” if appealed (GAO, 2011, p. 16). GAO reported significant variability in denial rates due to methodological issues in what is counted (billing errors, duplicate claims, missing data, eligibility, satisfaction of deductible amount, and necessity of the service) and methods of reporting (i.e., paper-based vs. electronic claims). Aggregate coverage denial rates varied across four states examined in detail (11 percent in Ohio and 24 percent in California for 2009) and across the largest insurers within a single state (4 percent to 29 percent for the seven largest insurers in Connecticut in 2009). About 1 in 10 of the coverage denials, according to American Medical Association (AMA) and NAIC data, dealt with the appropriateness of services (GAO, 2011).

States will be providing greater consumer protections related to how coverage decisions and medical necessity determinations are made and how they may be appealed. Section 2719 of the Public Health Services Act, added by Section 10101(g) of the ACA, seeks to bring more consistency to what consumers can expect with respect to internal and external claims and appeals processes through new requirements for group health plans and health insurance companies.5 In particular, all subscriber contracts must have a final level of “external appeal” to an

4 § 1001, amending § 2715 of the Public Health Service Act [42 U.S.C. 300gg–15].

5 The NAIC released a model state law that outlines an approach for responding to ACA requirements on grievances and appeals that will apply to insurers (NAIC, 2010). Interim final rules with request for comment were published July 22, 2010, and amendments issued June 24, 2011 (HHS, 2011b; U.S. Department of Labor et al., 2011).

independent outside party. The GAO report also calls attention to the frequency of reversal of coverage denials when such appeals are undertaken: from 39 to 59 percent of internal appeals across four states, and of those then appealed to an external source across six states, from 23 to 54 percent were overturned or revised (GAO, 2011). The GAO report also referenced an earlier study showing a difference in external appeal overturn rates by type of coverage denial in California managed care (42 percent of medical necessity cases overturned vs. 20 percent of experimental and investigational cases in 2002) (Gresenz and Studdert, 2005); more recent data presented to the IOM committee were not so proportionally disparate, showing 40 percent of medical necessity cases and 37 percent of experimental and investigational cases were overturned on independent external review (see Table 7-1). Overall, 661 decisions (out of 1,452 grievances that proceeded through the Independent Medical Review [IMR] process) were in favor of the enrollee; for each of these, the plan was required to authorize the treatment within 5 days of receiving the decision.

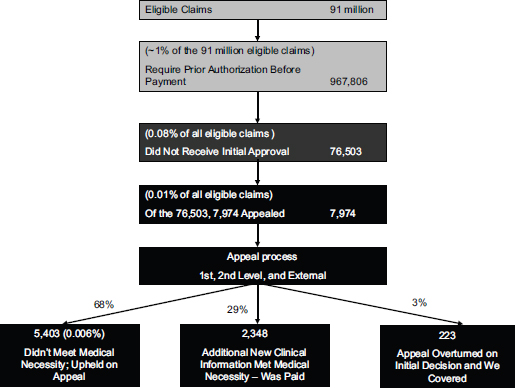

Notably, the Director of the California Department of Managed Health Care (DMHC), when testifying before the committee, pointed out another compelling statistic—the percentage of reversals by health plans of externally appealed cases even before they were reviewed (324 of 1,776 cases): 19 percent of medical necessity cases, 13 percent of experimental and investigational, and 34 percent of emergency room reimbursements. Staff of the DMHC felt these reversals were not the result of new clinical information because the pertinent clinical information should have surfaced during the insurer’s internal review (DMHC, 2011). To help visualize the overall degree of claims overturned, one insurer provided a figure with self-reported data showing of 91 million claims in the United States, approximately 99 percent of those were paid without a required preauthorization (Figure 7-1). At intermediate steps, 1 in 10 denials was appealed by patients, and 29 percent of the initial denials that were appealed were overturned as additional clinical information was obtained, and 3 percent were overturned on the same clinical information. Overall, 0.006 percent of total eligible claims were not ultimately approved.6

The committee agrees with HHS’s observation on the GAO report that “very little information is available to help analysts understand the causes or sources of variation in the data” (GAO, 2011, p. 26). Besides helping consumers shopping for insurance, improved data, including developing a standardized appeals database and requirements for reporting of these data, would facilitate recognition of potential problem areas in EHB definition. Once collected, the information should be analyzed to detect and understand meaningful trends, thus effectively also serving to monitor the changes in insurer behavior as part of the monitoring recommended in this chapter.

Standardization includes classifying individual appeals in a way that facilitates analysis. For example, appeals could be classified by condition and treatment, by groupings such as types of contractual coverage exclusions (e.g., cosmetic, experimental), and by reasons of medical necessity), as well as by characteristics of the individual making the appeal (e.g., age, disability, English language ability, race, income). The California DMHC, which currently classifies and analyzes appeals in multiple ways, showed that most treatment-related appeals in descending order were for pharmacy, mental health, durable medical equipment, autism, cancer care, and surgery. DMHC also gave the committee a report on the frequency of appeals by condition: orthopedic, mental disorders, central nervous system or neuromuscular, and cancer (DMHC, 2011). Discussion with other states suggests that the reasons for appeals may vary by state and over time.7

TABLE 7-1 Comparison of 2010 Independent Medical Review (IMR) Results in California Managed Care

|

|

||||

| Upheld by Review Number (%) |

Overturned by Review Number (%) |

Reversed by Plan Before Review Number (%) |

Qualified IMRs Total Number |

|

|

|

||||

| Medical Necessity | 467 (41%) | 452 (40%) | 222 (19%) | 1,141 |

|

|

||||

| Experimental and Investigational |

269 (51%) | 195 (37%) | 67 (13%) | 531 |

|

|

||||

| Emergency Room Reimbursement |

55 (53%) | 14 (13%) | 35 (34%) | 104 |

|

|

||||

| TOTALS | 791 | 661 | 324 | 1,776 |

|

|

||||

SOURCE: DMHC, 2011.

6 Personal communication with Jeffrey Kang, Chief Medical, Officer, CIGNA, February 17, 2011.

7 Personal communication with Mary Kempker, Missouri Department of Insurance, February 18, 2011.

FIGURE 7-1 CIGNA coverage decisions and appeals for preauthorization of health benefits (2010).

SOURCE: Provided to the IOM in response to its question about preauthorization and appeals volume by Dr. Jeffrey Kang, CIGNA’s Chief Medical Officer, February 17, 2011.

Collection of these data can point to the areas of care that are most contentious and require more detailed investigation into the specific services and conditions that need clarification in the EHB set. It is yet unclear the extent to which recent amendments to the interim final external review rules would present a barrier to accessing more detailed diagnostic and treatment code data for analysis of adverse benefit determinations; plans are only required to provide diagnostic and treatment code data for individual cases on request (HHS, 2011a,b; Jost, 2011). Administrative burden and confidentiality concerns were identified as reasons for limiting this specific data. While it would be advisable for insurers to make their clinical policies available in advance, for example, on the Web as multiple insurers do, the committee would support having, at least during the appeals process, the applicable clinical policies be made transparent. Enhanced transparency of clinical policies would allow analysis of whether interpretation of the existing evidence base is similar or different across insurers and what areas need advancement.

Other Types and Possible Sources of Data

Research related to the EHB is likely to include developing explanatory and predictive analyses of the relationship between the nature and characteristics of the benefit package and the decisions made by consumers about which plans to select, which services to use, the cost trends associated with these plans, and the effects on individual and population health. The data mentioned above, if well standardized, provide a necessary starting point for these types of studies. However, many research questions will require linking these data with other sources of information such as claims, hospital discharge data, and enrollee surveys, such as the Consumer Assessment of Healthcare Providers and Systems (CAHPS) survey. For specific questions, researchers may require additional data

sources such as clinical data from electronic health records or primary data collected via interviews or surveys. These data sources would be more useful if they could be linked at the individual enrollee level. Individual-level data provide greater opportunities to adjust and control for potential case-mix differences between the covered populations being compared. However, if individual-level data are not available or cannot be accessed, analyses relating aspects of EHB definition or benefits design across multiple population units (e.g., exchanges, insurers) to aggregate population measures such as utilization rates, appeal rates, or average costs for those same population units will sometimes be helpful.

New Approaches to Delivering Health Services

New approaches to prevention, diagnosis, treatment, and management are continually emerging. Health insurers have developed greatly varying methods for assessing the safety and efficacy of these interventions. Similarly, many have coverage policies for when they will pay for participation in clinical trials. Although the focus of most current work relates to new technologies, the committee believes it is important to consider the broader range of changes in the ways services are delivered. The committee heard testimony on these coverage components and the importance of developing policies prospectively to guide complex coverage decisions for vulnerable enrollees (Hole-Curry, 2011; Levine, 2011; Nussbaum, 2011). Some evaluations of the effectiveness of new approaches are public—such as the state of Washington’s—and some are proprietary. The results of these assessments and the resulting clinical policies may prove useful for the Secretary in updating the EHB, and the committee recommends they be systematically collected for that purpose.

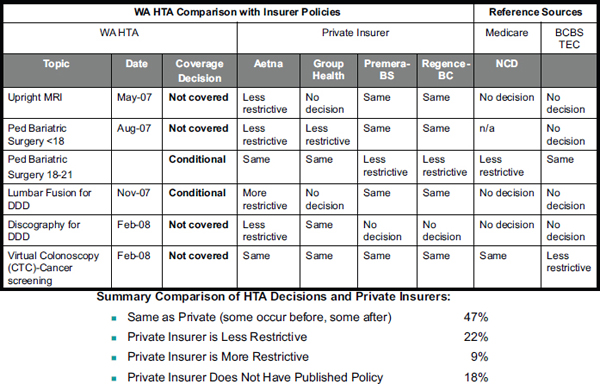

A variety of existing organizations routinely produce systematic reviews of emerging technologies; the comparative effectiveness of alternative approaches to diagnosis, treatment, or management; and the methods for ensuring that care is delivered safely. Using clear and transparent methods for assessment according to a hierarchy of evidence, they provide physicians, health plans, policy makers, and the public with evidence syntheses on which to consider changes in medical practice and coverage policy. However, different insurers, whether private or public, often using the same evidence, after consideration of other criteria may reach different conclusions about whether a specific service should be covered (Figure 7-2). Factors might involve criteria related to the specific population served or to budget constraints, or even different degrees of pressure received from stakeholders depending on the nature of the process employed. HHS can facilitate access to and understanding of a common evidence base for states, insurers, practitioners, and consumers, particularly as it applies to the EHB package.

Medical Cost and Premium Information

In Chapter 9, the committee calls for updates to the EHB to fit within a budget that is defined by the average national silver plan premium for the current EHB package in the next year. In that recommendation, the committee anticipates that the premium costs will increase based on medical inflation, demographic changes in the population, the inclusion of new technologies, and other factors. The Chief Actuary of CMS produces the standard trend data used in tracking these trends. If the Secretary or the Chief Actuary determines that additional, more detailed data can be obtained from the experience of the states with certain elements of the cost calculations that will be required, these data should be specified. In particular, costs associated with new services that are being considered for inclusion in the EHB might be obtained from this process.

Here the committee mentions four broad areas of a comprehensive research agenda, recognizing that within each area a rich set of questions will arise.

Understanding EHB definitions and their relationship to benefit design. The committee expects variation in the implementation of the EHB by different insurance companies and in different states, and this variation can be useful for evaluating what is working and what is not.

SOURCE: Hole-Curry, 2011.

This may be useful for understanding the impact of variations in the EHB package on subsequent benefit design decisions and costs. Does specifying a more expansive EHB package lead to greater use of limits or caps on visits or other services, to higher premiums and cost-sharing requirements, or to more restrictive networks of care? Are there specific inclusions or exclusions to the EHB that are particularly costly when offered in real-world settings? Is the relationship between benefits and premium costs consistent across settings, or does it vary widely? If it varies, how are some exchanges managing to offer broader benefits without driving prices up? How will the addition or expansion of benefits influence the actuarial value of benefit packages—and the availability of existing covered benefits?

Sources of data for addressing these questions include the standardized data on benefit content and design collected from insurers and from state health insurance exchanges. Information on benefits and benefit design being offered by employers (e.g., DOL survey), from the Medical Expenditures Panel Survey’s Insurance/Employer Component (MEPS-IC), and from surveys conducted by Kaiser Family Foundation, Mercer, and others, although currently limited for this purpose, can track changes in employer practices across a wider employer landscape than the exchanges alone unless statewide data are forthcoming on all forms of coverage. Data on costs and utilization patterns could be provided by national insurers active in multiple exchanges and by Medicaid, as well as data collected directly by state exchanges. Additional primary data collection, including patient and provider surveys and qualitative patient interviews in selected settings, would be needed to fully address some questions. In addition to these empirical studies, studies that blend empirical data with modeling approaches may also be valuable.

Relationships of EHB content and benefit design to patient outcomes and cost. Decisions related to the content and administration of the EHB package will affect the care that is offered to enrolled patients and may in

turn affect clinical outcomes. A decision by some states or exchanges to include additional types or categories of services to the 10 categories (e.g., adult dental, hospice if they are not in the initially defined package) would create natural experiments that could quantify the costs of adding such coverage for a population, as well as the consequences—both monetary and clinical—to patients. Such information will be needed by the NBAC and the Secretary as refinements to the EHB are contemplated.

In the process of updating the EHB, questions about specific therapies and services within covered categories will arise. Decision making on coverage of specific treatments typically starts with consideration of evidence from randomized controlled trials (RCTs) and syntheses of results when multiple trials have been conducted. Because controlled trials minimize risks of selection bias, they are essential for establishing treatment efficacy, as well as superiority, and are foundational in making coverage decisions. However, RCTs often leave questions remaining about the effect of these treatments in typical patients getting care from community practice settings. Trials generally do not include the entire spectrum of patients who are subsequently offered the treatment. Trials may not include all relevant outcomes, including monetary outcomes or satisfaction for patients, and they may not have followed patients long enough to observe longer-term outcomes. Thus, if insurance exchanges or specific insurers systematically differ in coverage of specific treatments, rigorous evaluation of patient outcomes and costs related to this variation would provide a valuable addition to the public deliberative process.

Many historical benefit design strategies, including cost sharing and restricted provider networks, lower costs to insurers and purchasers. Others, such as pay-for-performance initiatives and centers of excellence, can drive quality improvement efforts. Some of these approaches, however, can adversely affect patients. High prices for needed medications through cost sharing lead to decreases in adherence to chronic medications, with subsequent deterioration of disease control and increased utilization and adverse events. Refinements such as value-based insurance designs endeavor to use evidence on the health benefits of different interventions in designing financial incentives that encourage patients to make the most effective and cost-effective treatment choices by removing financial barriers to those choices and/or by raising these or other barriers to less appropriate options. They hold great promise for improving the effectiveness and efficiency with which health insurance dollars are spent. The emphasis on cost restraints under the ACA will undoubtedly lead to a proliferation of new insurance products with further evolution in benefit design. Systematic evaluation of this variation will ensure that good practices are recognized and spread quickly and that adverse effects are minimized.

Data for studying the impact of EHB content and benefit design on patient outcomes come from the same sources mentioned above. Specific research questions will require augmentation through linkage of these data sources with insurer data on health care utilization (e.g., from Medicaid and private insurers), clinical information from electronic health records and other data sources of health care delivery systems, or data collected from surveys or qualitative interviews with patients selected for specific characteristics such as the presence of a chronic condition.

Possible impact of EHB and benefit design decisions on the required elements for consideration. The ACA includes a number of “required elements for consideration” that must be monitored and may thus require updating of the EHB. These include concerns that there be balance among the covered categories; that there be no discrimination based on age, disability, or expected length of life; that benefits take into account and cover the diverse needs of various population segments; and that emergency care not be restricted (e.g., by requirements for prior authorization).

The monitoring process should include assessing the required elements for consideration specified in the ACA. However, further research will be required to determine whether trends identified in monitoring require action. If variation is found across states or exchanges, not only in appeals but also in other areas, outcomes studies based on utilization and clinical data as well as patient survey data may be needed to establish links between practices and outcomes and to identify best practices.

Attention may focus initially on variation in the absolute and relative expenditures by category across jurisdictions. Outliers, especially on the low side, may signal problematic coverage or implementation. Areas of particular complexity include issues such as mental health services, habilitative services, and orphan diseases. Research approaches of particular value here would include analyses of appeals; the impact of state mandates for services not broadly included in the EHB; and surveys of beneficiaries from various population segments and the providers who care for them.

Comparative effectiveness of specific preventive and therapeutic options. The research discussed above, which uses implementation data to study variation in EHB content and benefits design, will contribute greatly to understanding how inclusion or exclusion of broad categories of services affects patient outcomes and costs. It will also deepen understanding of the effects of various benefits design strategies on these outcomes. However, as the Secretary and the NBAC seek to define EHB more specifically over time, more information will be needed on specific treatments and preventive and diagnostic services, including newly introduced pharmacotherapies, procedures, and devices. These therapies may not yet be covered by any policies in the exchanges, and definitive information on their effectiveness can therefore not come from these data.

The needed information will come from a variety of sources. These include the ongoing publication of original research studies, especially clinical trials; syntheses of previously reported research; recent technology assessments from sources such as BlueCross BlueShield Association’s Technology Evaluation Center, AHRQ’s Evidence-Based Practice Centers and Developing Evidence to Inform Decisions about Effectiveness (DEcIDE) research program, and the U.S. Preventive Services Task Force (for screening and prevention services), as well as the Medicare Evidence Development and Coverage Advisory Committee (MEDCAC) and professional society guidelines. PCORI is expected to fund comparative effectiveness research (CER) and summaries with a particular emphasis on patient perspectives—yet cannot employ a dollars per quality adjusted life-year threshold in its determinations.8 These studies will evaluate both specific preventive and therapeutic choices as well as system-level interventions for improving care. The FDA, Department of Defense, CMS, and state Medicaid agencies also generate reports that will deserve consideration. The Secretary and the NBAC will require staffing and a process for ensuring that all relevant data are identified and considered.

In this work, studies that follow the principles of CER will be particularly valuable and should be emphasized. CER principles include comparisons between meaningful therapeutic alternatives, conduct of studies in typical clinical settings and involving a broad range of patients, consideration of multiple outcomes including outcomes of particular importance to patients, and attention to possible differences in treatment effectiveness in patient subgroups.

CCIIO (Center for Consumer Information and Insurance Oversight). 2010. The Center for Consumer Information & Insurance Oversight. Initial announcement: Invitation to apply for FY 2010. http://cciio.cms.gov/resources/fundingopportunities/consumer_assistance_program_grant_foa.pdf (accessed July 22, 2011).

DMHC (California Department of Managed Health Care). 2011. Independent State Review Processes. PowerPoint Presentation to the IOM Committee on the Determination of Essential Health Benefits by Cindy Ehnes, Director, Maureen McKennan, Acting Deputy Director for Plan and Provider Relations, and Andrew George, Assistant Deputy Director, Help Center, Department of Managed Health Care, Costa Mesa, CA, March 2.

GAO (Government Accountability Office). 2011. Private health insurance: Data on application and coverage denials. Washington, DC: Government Accountability Office.

Gresenz, C. R., and D. M. Studdert. 2005. External review of coverage denials by managed care organizations in California. Journal of Empirical Legal Studies 2(3):449-468.

HHS (Department of Health and Human Services). 2011a. Interim final rules for group health plans and health insurance issuers relating to internal claims and appeals and external review processes under the Patient Protection and Affordable Care Act. http://www.cq.com/flatfiles/editorialFiles/healthBeat/reference/docs/072301.pdf (accessed September 13 2011).

______. 2011b. Rules and regulations: Group health plans and health insurance issuers: Rules relating to internal claims and appeals and external review processes. Federal Register 76(122):37208-37234.

Hole-Curry, L. 2011. Transforming health care: Using evidence in benefit decisions. PowerPoint Presentation to the IOM Committee on the Determination of Essential Health Benefits by Leah Hole-Curry, Program Director, Washington State Health Technology Assessment Program, Costa Mesa, CA, March 2.

IOM (Institute of Medicine). 2002. Leadership by example: Coordinating government roles in improving health care quality. Washington, DC: The National Academies Press.

______. 2007. The learning healthcare system: A workshop summary. Washington, DC: The National Academies Press.

______. 2009a. HHS in the 21st century: Charting a new course for a healthier America. Washington, DC: The National Academies Press.

______. 2009b. Initial national priorities for comparative effectiveness research. Washington, DC: The National Academies Press.

8 § 6301, amending § 1181 of the Social Security Act.

______. 2011. The learning health system series: Continuous improvement and innovation in health and health care. Washington, DC: The National Academies Press.

Jost, T. S. 2011. Health Affairs blog. http://healthaffairs.org/blog/2011/06/23/implementing-health-reform-the-appeals-process-amended-rule/ (accessed September 23, 2011).

KFF (Kaiser Family Foundation) and HRET (Health Research Education Fund). 2010. Employer Health Benefits 2010 Annual Survey. Menlo Park, CA and Chicago, IL: Kaiser Family Foundation and Health Research Education Trust.

Levine, S. 2011. PowerPoint Presentation to the IOM Committee on the Determination of Essential Health Benefits by Sharon Levine, Associate Executive Medical Director, The Permanente Medical Group, Costa Mesa, CA, March 2.

NAIC (National Association of Insurance Commissioners). 2010. Uniform Health Carrier External Review Model Act. Washington, DC: National Association of Insurance Comissioners.

______. 2011. Library: Consumer resources & guides. http://www.insureuonline.org/ (accessed July 22, 2011).

Nussbaum, S. 2011. Health insurance plan variance in coverage (inclusions, exclusions, networks) and benefit design for quality improvement. PowerPoint Presentation to the IOM Committee on the Determination of Essential Health Benefits by Sam Nussbaum, Executive Vice-President, Clinical Policy and Chief Medical Officer, Wellpoint, Inc., Costa Mesa, CA, March 2.

State of Colorado. 2010. Report of second level appeal and independent external reviews calendar year 2010. http://hermes.state.co.us/insurance/consumer/2011%20docs/cons2010ReportSecondLevelAndIndependentExternalReviews042111.pdf (accessed November 1, 2011).

U.S. Department of Labor, Treasury, and HHS. 2011. Group health plans and health insurance issuers: Rules relating to internal claims and appeals and external review processes; correction. Federal Register 76(143):44491-44493.