___________

Stakeholder Decisions on Health Insurance

This appendix expands upon Figure 1-2 in Chapter 1 through a discussion of how various stakeholder (individual, employer and employee, state, and health insurance company) decisions in the course of the Patient Protection and Affordable Care Act (ACA) implementation might individually, and together, impact the health insurance landscape.

INDIVIDUAL CHOICE

The individual purchaser must decide whether or not to purchase insurance, which type of plan to participate in, and given a choice of plans, what level of out-of-pocket expenditures (premiums, deductible, co-payments) are considered affordable.

Take-up Decisions

Because of the individual mandate, individuals will have to decide whether to purchase insurance or accept the penalty.1 Depending on their financial circumstances, employment status, and attitudes toward having insurance, they will have choices among employer-sponsored insurance, subsidized coverage through the exchange, Medicaid, or even to remain uninsured. The key dollar triggers for individual take-up are outlined in Box B-1.

With implementation of the ACA, those currently uninsured will have to decide if they want to purchase coverage to obtain the financial protection and access that insurance provides, or violate the mandate and pay the penalty. While some parties have criticized the requirement that everyone has to buy insurance, others have been

1 Those without health insurance coverage will be required to pay a penalty in the form of a tax. This penalty will be the greater of $695 per year up to a maximum of three times that amount ($2,085) per family, or 2.5 percent of household income. It will be phased in: $95 or 1.0 percent of taxable income in 2014, $325 or 2.0 percent in 2015, and $695 or 2.5 percent in 2016. Beginning after 2016, the penalty will be increased annually by the cost-of-living adjustment. Exemptions will be granted for financial hardship and religious objections, to American Indians, those without coverage for less than 3 months, undocumented immigrants, incarcerated individuals, those for whom the lowest-cost plan option exceeds 8.0 percent of an individual’s income, and those with incomes below the tax filing threshold (in 2009 the threshold for taxpayers under age 65 was $9,350 for singles and $18,700 for couples) (Patient Protection and Affordable Care Act of 2010 as amended. § 1501 [42 U.S.C. 18091]. 111th Cong., 2d sess.

critical that the imposed penalty amount is too low to motivate many to buy insurance, particularly if the premiums associated with the essential health benefits (EHB) are high (Laszewski, 2010).

BOX B-1

Key Dollar Triggers for Individuals (in 2011 dollars)

Medicaid Eligibility

Eligibility: 138 percent federal poverty level (FPL) ($15,028 for individual, $30,843 for family of four in 2011)

No premium and nominal cost sharing

Penalty for Not Having Insurance in 2016

Is greater of

• $695 per person, up to $2,085 family OR 2.5 percent adjusted gross income share of premium for lowest-cost option

Exemption for financial hardship:

• Share of premium for lowest-cost option. 8 percent of income ($3,551 for median income), AND

• Those with incomes below tax filing threshold ($9,350 for single; $18,700 for couples in 2009)

Exchange Subsidy

Eligibility: 139-250 percent FPL ($15,137-$27,225 for an individual or $31,067-$55,875 for a family of 4 in 2011)

• Sliding scale tax credits limit premium costs to 3-8.05 percent of income; sliding scale cost-sharing credits

Eligibility: 251-400 percent FPL ($27,334-$43,560 for an individual; $56,099-$89,400 for a family of four in 2011)

• Sliding scale tax credits limit premium costs to 8.05-9.5 percent of income; no cost-sharing credits

Exchange Nonsubsidized:

Eligibility: >400 percent FPL

• No sliding scale tax credit and no cost-sharing credits. No annual limit on deductibles specified in legislation

NOTE: The FPL ranges are in current 2011 dollars. The triggers will be in 2014 dollars.

Choice of Insurance

Individual consumers desiring to participate in private plans will retain their choice of insurer and type of plan to be purchased, and they are not required to purchase plans through the health insurance exchanges. The

EHB will set a minimum set of standard benefits for health insurance plans offered to individual purchasers, both inside and outside of the exchange. Plans may add additional benefits beyond those in the EHB package, and an individual can choose to purchase the plan that best suits his or her individual or family needs, although purchasing additional benefits can mean a higher premium.

Out-of-Pocket Costs

Out-of-pocket costs include premiums, deductible payments, co-insurance, and co-payments for covered services in addition to all costs for noncovered services (see Chapter 2 for further discussion of benefit design).

Just as how insurance currently functions, insurers will offer a variety of consumer plan options in 2014; having a more standardized benefit set should help consumers more easily comparison shop for the best value for themselves and their families.

Besides the initial premium, most plans have a deductible that the consumer must pay before insurance coverage begins. If enrolled in a plan that is a health maintenance organization (HMO), the consumer would likely have a primary care physician, be limited to the health care providers in that network, and would need a referral from the assigned primary care physician to see a specialist. If consumers choose a preferred provider organization (PPO), they can see those providers within the PPO network and only be responsible for the deductible and co-payment. It is possible to see an out-of-network provider, but it will cost the consumer more if there is a difference between the provider’s bill and the approved level of coverage for in-network providers. Prospective patients have to consider, when seeking care, whether the “value of the care exceeds the out-of-pocket costs” (Baicker and Chandra, 2008, p. w536).

Research has shown that individuals without health insurance are more likely to experience financial burdens associated with utilization of health care services or avoid needed care due to cost. Yet, even among the insured, underinsurance has emerged as a barrier to care because out-of-pocket costs take a substantial percentage of income. For the healthy uninsured, those medical out-of-pocket (MOOP) costs may be minimal, but for the less healthy person they can be substantial, whether insured or not. For example, about one-quarter of those with chronic conditions spend more than 10 percent of their family income on MOOP expenses, whether insured or not; 52.9 percent of persons with private non-group insurance coverage spend more than 10 percent of family income on MOOP. Additionally, 29 percent those who are poor (<100 percent federal poverty level [FPL]) spend more than 10 percent on MOOP expenses (Banthin, 2011; Banthin et al., 2008).2

About 80 percent of individuals using the exchanges will be lower income and will qualify for subsidies when their income falls between 139 and 400 percent of the federal poverty level (see Box B-1) (KFF, 2011c).3 The subsidies are designed to hold enrollee spending on premiums at 3.0-9.5 percent of their household income, in the form of an advanceable tax credit available at the time of purchase and paid to the insurer monthly rather than as a refund on a person’s tax return after the year is over (KFF, 2011a).4 Households with incomes from 139-250 percent of the FPL will also receive subsidies for cost sharing. The poorest citizens with incomes up to 138 percent of the FPL will qualify for Medicaid. Persons who buy coverage outside of the exchange will pay the entire premium, as will those buying in the exchange whose income is over 400 percent of the FPL.

The Congressional Budget Office (CBO) estimated the impact of health reform on premiums under bill H.R. 3590, which is similar to the final ACA provisions, based on an average employer premium. The cost for individuals to purchase insurance in the exchange is likely to result in a premium that is 10-13 percent higher than without ACA requirements, given the more comprehensive nature of the required essential health benefits and the constraints on OOP. On the other hand, premiums would be effectively reduced by 56-59 percent for individuals who qualify for premium subsidies (CBO, 2009).

2 Note: Medical Expenditure Panel Survey (MEPS) data include premiums in MOOP calculations (Banthin et al., 2008).

3 The Medicaid eligibility level is set at 133 percent of the FPL, but a 5 percent disregard effectively raises it to 138 percent (Health Care and Education Reconciliation Act § 1004(e) amendment of ACA).

4 ACA as amended § 1412(c)(2)(A).

EMPLOYERS AND EMPLOYEES

Employers must decide whether or not to offer insurance, which type of plan to offer, and what level of premiums, deductible, and co-payments are considered affordable for both the firm and its employees.

Decision to Offer

Before deciding to offer health insurance, employers small and large must first consider the value of offering insurance, not only in terms of recruiting and retaining their workforce, but also as a mechanism to meet employee expectations while promoting wellness and productivity. Uninsured employees who do not want to pay a penalty will be required to acquire insurance. Thus, employers must also consider the law’s individual mandate requirement, the subsequent increased demand for insurance by their employees, and the impact of requiring the EHB in insurance packages offered by small employers (Eibner et al., 2010).

Similarly, although not explicitly a mandate, beginning in 2014, firms with 50 or more employees that do not offer insurance and have 1 or more employee who obtains a tax credit on the exchange, will have to pay a “fee” (or a penalty) of $2,000 per employee.5 If employees are a riskier population (i.e., of older age and in poorer health), an employer may find it more financially advantageous to pay the penalty than to offer health insurance. Key dollar considerations for employers and employees are outlined in Box B-2.

Level of Tax Credit

In making decisions to offer health insurance and/or to self-insure, employers will have to take into account tax credits, the applicable fees or penalties for not participating, and the availability of tax credits for employees, currently and into the future. The ACA authorized a temporary tax credit beginning in tax year 2010 for businesses with less than the equivalent of 25 full-time employees with average annual wages of $50,000 or less6 (IRS, 2011b; Peterson and Chaikind, 2010). These small firms will receive a tax credit up to 35 percent of the employer premium contribution (employers must be contributing at least half of the premium), and this tax credit portion will rise to 50 percent in 2014 at the time employers are required to offer health plan options through the exchange. How small the firm is (e.g., 10 or fewer, or larger), the average salary of the workforce, and whether the firm is a for-profit or nonprofit entity will determine the actual amount of the credit and how long the credit is available.

Self-Insure vs. Fully Insure

Another decision facing employers is whether to self-insure or fully insure. Under the Employee Retirement Income Security Act (ERISA) law, self-insured employers are already exempt from state-mandated benefits, and even following passage of the ACA, they are similarly exempt from EHB requirements. Self-insured means that firms provide health benefits to their employees with their own funds; these are typically, but not always, larger employers. In fully insured employer-sponsored insurance (ESI), on the other hand, an employer contracts for insurance coverage through an insurance company rather than taking the risk directly. About half of the employees participating in fully insured ESI are considered likely to purchase insurance through state-based health insurance exchanges because of a combination of better coverage options and lower costs (CBO, 2010; Eibner et al., 2010).

With the implementation of the ACA, RAND estimates little impact in terms of the proportion of employers that self-fund their health insurance (6 percent) (Eibner et al., 2011). However, the percentage rises to about a third of businesses being inclined to self-insure if very-low-risk stop-loss plans are allowable as a form of self-insurance

5 § 1513. Note: The penalty does not apply to the first 30 employees.

6 § 1421.

in the market,7 thus enabling employers to avoid the EHB and other requirements if they so desire. This steep increase in the share of employers self-insuring would be “driven almost entirely by small businesses (100 or fewer workers)” (Eibner et al., 2011, p. 83).

BOX B-2

Key Dollar Considerations for Employers and Employees

Employer “Fees”

• Firms with more than 50 employees that do not offer coverage are subject to a “fee” of $2,000 per employee if 1 or more employees obtains a tax credit on the exchange (excludes first 30 employees).

• Firms with more than 50 employees that DO offer coverage are subject to a “fee” of the lesser of $3,000 per employee receiving a tax credit on the exchange or $2,000 per full-time employee.

Employee Eligibility for Tax Credit

• Employees are eligible for tax credit if actuarial value of employer plan is less than 60 percent OR if employee share of premium exceeds 9.5 percent of income.

Employee Deductible Limit in ESI

• Maximum deductible of $2,000 for individual and $4,000 for others (§ 1302(c)(2)(A)).

Insurer Cadillac Tax

• Excise tax on insurers of employer-sponsored health plans with aggregate values greater than $10,200 for individuals and $27,500 for families starting in 2018.

Even though exchanges are not open to large employers initially, the National Business Group on Health, which represents large employers, still expressed concern about the content of the EHB because “many employers will see anything the federal government does to define essential benefits as the floor for all benefits and that will have the effect of driving up costs” (Darling, 2011, p. 2).

Costs

CBO analyses suggest that small firms with fewer than 50 employees could experience a range of premium change by 2016 from a 2 percent decrease to a 1 percent increase without the small business tax credit; however, the tax credit would reduce premiums 8-11 percent for eligible firms (CBO, 2009).

7 Stop-loss insurance is a “form of reinsurance that provides protection for annual medical expenses above a certain limit. It can take the form of specific stop loss, where the insurance coverage reimburses all claims above a certain deductible (such as $100,000 per individual); or aggregate stop loss, where the coverage reimburses a percentage of claims if a group’s claims exceed a certain percentage of the expected level (such as 120 percent)” (SOA, 2009, p. 88). Sixteen states have regulations that prohibit insurers from selling stop-loss policies with attachment points below specified limits, which range from $5,000 to $25,000 (Eibner et al., 2011). Jost further comments, “when small employer packages purchase ‘self-insured’ packages from insurers, including stop-loss coverage with very low attachment points and administrative services, they are essentially purchasing conventional health insurance, except that it is free from state regulation” (Jost, 2011, p. 1).

STATES

States are concerned about their fiscal picture. They must take into consideration the population that will be newly eligible for Medicaid, any impact the scope of the EHB package might have on their state employee benefit programs, and the extent to which the EHB will include current state mandates.

Medicaid Costs

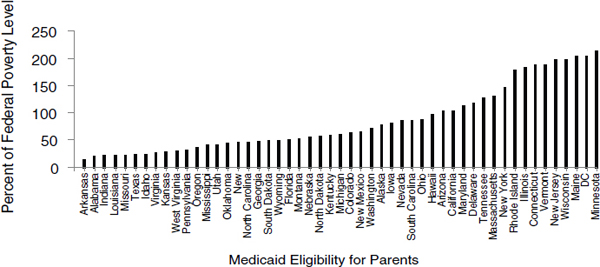

Figure B-1 illustrates how states’ current Medicaid coverage levels stack up against the new ACA eligibility standard of 138 percent of the FPL for adults. All states have begun to consider the future proportion and amount of Medicaid spending that they must cover vs. what portion is paid by the federal government; this will vary considerably by state. Although the EHB do not apply to the traditional Medicaid program, they form the backdrop against which other decisions may affect state financial resources.8 Some states have expressed concern that the Medicaid expansion will be detrimental to their already tight budgets, yet others are finding that there may be choices in how they implement the ACA Medicaid provisions that may be beneficial once they take into account the federal match9 and other provisions. For example, states will have to decide whether individuals newly eligible because of their financial status should enter traditional Medicaid or a benchmark/benchmark-equivalent program (CMS, 2010; KFF, 2011d).

For states operating a state-based exchange, they will also have to make decisions about how their exchange intersects with any existing or other newly planned state programs, as well as how they can best ensure continuity of administration, continuity of care, and alignment of benefits across programs. This is especially important because individuals and families frequently face eligibility changes—“churning” in and out of Medicaid eligibility and enrollment (Sommers and Rosenbaum, 2011; Washington State Health Benefit Exchange Project Health Care Authority, 2010). Sommers and Rosenbaum (2011) estimated that 35 percent will have their eligibility change from Medicaid to the exchanges or the reverse within 6 months, and 50 percent will experience a change within one year.

FIGURE B-1 States vary in the potential increase in size of the newly eligible Medicaid population at or under 138 percent of the federal poverty level.

SOURCE: ACA as amended § 2001(a)(1)(C); KFF, 2011b.

8 Title XIX of the Social Security Act (Social Security Act § 1902(a)(10)(A)).

9 ACA as amended § 2001(y).

EHB Applicability to State Programs

The EHB will apply to the new Medicaid benchmark and benchmark-equivalent plans and state basic health insurance plans for low-income persons not eligible for Medicaid. Traditional Medicaid has its own set of federal mandatory benefits as well as optional benefits states can elect, while benchmark and benchmark-equivalent plans and state basic health insurance plans are modeled more closely on private sector offerings. The EHB will also apply to state employee benefit programs unless states choose to self-insure.

Medicaid benchmark and benchmark-equivalent plans were initiated under the Deficit Reduction Act of 2005 to give flexibility to states to define a different scope of services than those defined in Title XIX. Programs are held to a benchmark (i.e., Federal Employees Health Benefits Program [FEHBP] preferred provider-equivalent coverage, state employee coverage, an HMO with the largest insured commercial population in the state, or any other HHS Secretary’s approved benefits coverage). Certain groups of individuals who are “categorically eligible” for Medicaid are exempt from being enrolled in benchmark plans (CMS, 2010; KFF, 2011d).10 The State Basic Health Program is an optional insurance plan that states can develop to cover individuals whose income falls between 139 and 200 percent FPL as well as for low-income legal immigrants ineligible for Medicaid. States could receive federal subsidies for this type of program at a level equivalent to 95 percent of the federal subsidy if the person had participated in the exchange. In addition to offering the EHB, Section 1331 of the ACA outlines other requirements for this program: the consumer cannot be charged a premium that would exceed what he/she would have been paid in the exchange; the plan, to the extent available in the area, is a managed care system or like a managed care system; and the plan or provider implements innovations for care coordination and care management, incentives for use of preventive services, and maximizes patient involvement in decision making (Dorn, 2011).

State Mandates

States are also concerned about what the relationship will be between mandates required by each state’s own legislature and the EHB. States must pay the cost of mandates that are above and beyond the EHB, thus having repercussions for state budgets when a state has many pre-existing mandates that are not folded into the EHB.11 On the other hand, if the EHB package was set to mirror the requirements of a state with many mandates, then a state with a history of few mandates would expect that newly resulting commercial insurance products might far exceed what the state thinks is an acceptable premium for its residents. For example, if the EHB package is more comprehensive than that currently offered for state employees, the state will incur additional expenses.

HEALTH INSURANCE COMPANIES

Insurers must decide which markets to enter, which products they will offer, and at what premium price levels.

Products

Insurers participating in the exchanges must offer at least one gold and one silver plan,12 each of which must meet certain standards regarding benefits,13 providers (including essential community providers),14 cost-sharing,15

10 These exempt individuals include mandatory categories of pregnant women; blind or disabled individuals; dual eligibles; terminally ill hospice patients; those eligible on basis of institutionalization; medically frail and special needs individuals; beneficiaries qualifying for long term care services; children in foster care receiving child welfare services and children receiving foster care or adoption assistance; TANF (Temporary Assistance for Needy Families) and Section 1931 parents; women in the Breast or Cervical Cancer Program; and limited services beneficiaries (Social Security Act § 1937(2)(B)).

11 ACA as amended § 1311(d)(3).

12 § 1301(a)(1)(C)(ii).

13 § 1302(b)(1)(A)-(J).

14 § 1311(c)(1)(B)-(C).

15 § 1402.

premiums,16 rating restrictions,17 uniform quality improvement strategy,18 and measurements of plan performance19—the same for new enrollees whether the plan is offered inside or outside of the exchange.20 Prior to health reform, it has been at the discretion of insurance companies to decide what benefits to offer in their policies or plans and to adjust benefits and prices according to market demand. The ACA requires individual and small group plans to incorporate the EHB and stipulates that nothing prohibits plans from “providing benefits in excess of the essential health benefits.”21

Pricing

Under the ACA, there is guaranteed issue, meaning an individual cannot be turned down based on health or risk status, nor can an employer be turned down for the health status of its employees. That aside, a few demographic characteristics can still be factored into the premium rates, including geographic location, age, and tobacco use (the latter two have restrictions—that is, premiums for older individuals can only be three times higher than the premium for younger individuals and 1.5 times higher for users of tobacco22). The ACA still allows insurers to employ utilization management practices in common use by group health plans and health insurance issuers at the time of enactment and bars the issuance of regulations that would prohibit their use.23

Deductibles and cost-sharing arrangements are other elements factored into premium prices. For example, when two policies have the same benefits, typically the one with the higher deductible and higher cost-sharing provisions will have a lower premium, although some exceptions exist. The ACA sets limits on deductibles for employer plans ($2,000 for single coverage, $4,000 for others) but not for individual plans, as well as annual limits on cost sharing for both employer and individual plans. Annual cost sharing cannot exceed thresholds applicable to Health Savings Account (HSA)–qualified high-deductible health plans ($6,050 for individuals and $12,100 for families for 2012) (IRS, 2011a). The scope of benefits as well as other benefit design and administration elements will have an impact on the ultimate premium; these are discussed further in Chapter 2.

REFERENCES

Baicker, K., and A. Chandra. 2008. Myths and misconceptions about U.S. health insurance. Health Affairs 27(6):w534.

Banthin, J. S. 2011. High out-of-pocket financial burdens for health care. PowerPoint Presentation to the IOM Committee on the Determination of Essential Health Benefits by Jessica Banthin, Economist, Center for Financing, Access and Cost Trends, Agency for Healthare Research and Quality, Costa Mesa, CA, March 2.

Banthin, J. S., P. Cunningham, and D. M. Bernard. 2008. Financial burden of health care, 2001-2004. Health Affairs 27(1):188-195.

CBO (Congressional Budget Office). 2009. Letter to the Honorable Evan Bayh, U.S. Senate from Douglas W. Elmendorf, Director, Congressional Budget Office, November 30, 2009.

______. 2010. Letter to Speaker Nancy Pelosi from Douglas W. Elmendorf with spending estimate of the Reconcilation Act of 2010, March 20, 2010.

CMS (Centers for Medicare & Medicaid Services). 2010. Re: Family planning services option and new benefit rules for benchmark plans. https://www.cms.gov/smdl/downloads/SMD10013.pdf (accessed November 14, 2011).

Darling, H. 2011. Recommendations on criteria and methods for defining and updating individual mandates and packages: Purchaser perspectives. PowerPoint Presentation to the IOM Committee on the Determination of Essential Health Benefits by Helen Darling, President and CEO, National Business Group on Health, Washington, DC, January 13.

Dorn, S. 2011. The basic health program option under federal health reform: Issues for consumers and states. Washington, DC: AcademyHealth.

Eibner, C., F. Girosi, C. C. Price, A. Cordova, P. S. Hussey, A. Beckman, and E. A. McGlynn. 2010. Establishing state health insurance exchanges: Implications for health insurance enrollment, spending, and small businesses. Santa Monica, CA: RAND Corporation.

16 § 1401.

17 § 1311(c)(3).

18 § 1311(c)(1)(E).

19 § 1311(c)(1)(D)(i).

20 Health insurance coverage already in force before January 1, 2014, will be grandfathered and not subject to the restrictions.

21 § 1302(b)(5).

22 § 1201, amending § 2701(a)(1)(A)(iii)-(iv) of the Public Health Service Act. [42 U.S.C. 300gg].

23 § 1563(d)(1). [42 U.S.C. 18120].

Eibner, C., F. Girosi, A. R. Miller, A. Cordova, E. A. McGlynn, N. M. Pace, C. C. Price, R. Vardavas, and C. R. Gresenz. 2011. Employer self-insurance decisions and the implications of the Patient Protection and Affordable Care Act as modified by the Health Care and Education Reconciliation Act of 2010 (ACA). Santa Monica, CA: RAND Corporation.

IRS (Internal Review Service). 2011a. 26 CFR 601.602: Tax forms and instructions. http://www.irs.gov/pub/irs-drop/rp-11-32.pdf (accessed July 22, 2011).

______. 2011b. Small business health care tax credit for small employers. http://www.irs.gov/newsroom/article/0,,id=223666,00.html (accessed July 5, 2011).

Jost, T. S. 2011. The Affordable Care Act and stop-loss insurance: Statement to the NAIC ERISA(b) subgroup by Timothy Stoltzfus Jost, NAIC funded consumer representative. http://www.naic.org/documents/committees_b_erisa_110908_jost.pdf (accessed September 22, 2011).

KFF (Kaiser Family Foundation). 2011a. Determining income for adults applying for Medicaid and exchange coverage subsidies: How income measured with a prior tax return compares to current income at enrollment. Focus on health reform. Washington, DC: Kaiser Family Foundation.

______. 2011b. Income eligibility limits for working adults at application as a percent of the federal poverty level (FPL) by scope of benefit package, January 2011. http://www.statehealthfacts.org/comparereport.jsp?rep=54&cat=4&sortc=1&o=a (accessed July 28, 2011).

______. 2011c. A profile of health insurance exchange enrollees. Washington, DC: Kaiser Family Foundation.

______. 2011d. Medicaid policy options for meeting the needs of adults with mental illness under the Affordable Care Act. http://www.kff.org/healthreform/upload/8181.pdf (accessed November 14, 2011).

Laszewski, R. 2010. Is the individual mandate really a lynchpin in the new health law? http://www.kaiserhealthnews.org/Columns/2010/December/121410laszewski.aspx (accessed June 30, 2011).

Peterson, C. L., and H. Chaikind. 2010. Summary of small business health insurance tax credit under PPACA (P.L.111-148). Washington, DC: Congressional Research Service.

SOA (Society of Actuaries). 2009. Glossary. http://www.soa.org/library/essays/health-essay-2009-glossary.pdf (accessed September 26, 2011).

Sommers, B. D., and S. Rosenbaum. 2011. Issues in health reform: How changes in eligibility may move millions back and forth between Medicaid and insurance exchanges. Health Affairs 30(2):228-236.

Washington State Health Benefit Exchange Project Health Care Authority. 2010. Issue brief #3: Health benefit exchange functions and responsibilities: November 24, 2010. Olympia, WA: Washington State Health Care Authority.