8

European Policies Influencing

Pharmaceutical Innovation

MICHAEL L. BURSTALL

The goals of this chapter are (1) to identify European policies that influence pharmaceutical innovation and (2) to estimate their effect. Every European government is more heavily involved in health care than is the United States government, and the ability of European governments to affect the process of innovation is greater. Most, though not all, European governments have interventionist traditions that make them willing to use their powers. The ways in which they do so, and the degree to which they succeed, is the central theme of this chapter.

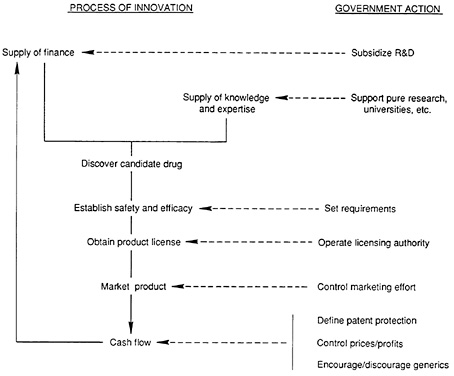

How do government policies toward industry affect pharmaceutical innovation? The relationships are illustrated in Figure 8.1. The first step in the process of research and development (R&D) is to discover new medicinal products. This requires a critical mass of capable scientists and a solid scientific and technical infrastructure. Official policies toward the scientific community, past and present, are therefore important. After its initial discovery, a candidate drug must be shown to be safe and effective; the necessary development process is powerfully influenced by national regulations governing the admission of new products to markets.

To remain successful, pharmaceutical companies need to make a suitable return on their investment in R&D. Those that do not will lack the resources to develop more new medicines. The possibility of making a suitable return—and it should be remembered that most drugs fail commercially—will be influenced by the time that it takes to register a product and the effective patent life remaining. What a manufacturer can charge in its major markets will determine its cash flow; most European countries have price controls, and, in practice, drug prices vary widely. In the longer run,

FIGURE 8.1 How government actions may affect pharmaceutical innovation.

official attitudes toward generic products will also be important. However, what the government takes away with one hand it may give back with the other in the form of preferential pricing and other subsidies for research.

Thus, the effects of government action on pharmaceutical innovation are more extensive and more complex than they might at first appear. This is not all. Europe is fragmented along national lines. The differences in pharmaceutical production and consumption among European countries (as shown in Table 8.2 ) are quite large. Moreover, under the Treaty of Rome, 1 health care is left to the individual member countries. The European Commission has in practice managed to engineer the convergence of national regulations in some areas, but in others (e.g., pricing policies) large differences between one state and another continue to evolve. Thus, it often makes little sense to talk about “Europe ”; rather, one has to talk about the situation in France, West Germany, the United Kingdom, and so on. To overcome this problem, this paper adopts a comparative approach. The salient facts about national markets and industries are summarized in Table 8.1, Table 8.2, and Table 8.3. The following discussion focuses on the major European countries and on current developments.

TABLE 8.1 Pharmaceutical Production and Consumption in the European Community, 1987

|

Pharmaceutical Consumption |

||||||

|

Country |

Millions of Dollars a |

Dollars Per Capita b |

As Percent GNP |

As Percent Health Care Spending b |

Average Price [UK=100] c |

Implied Per Capita Volume [UK=100] d |

|

Belgium |

1,230 |

125 |

0.86 |

11.7 |

74 |

210 |

|

Denmark |

380 |

75 |

0.38 |

6.6 |

103 |

91 |

|

France |

7,510 |

136 |

0.84 |

10.0 |

58 |

292 |

|

West Germany |

9,350 |

153 |

0.84 |

10.5 |

113 |

168 |

|

Greece |

360 |

36 |

0.76 |

16.5 |

61 |

74 |

|

Ireland |

200 |

56 |

0.66 |

9.1 |

112 |

62 |

|

Italy |

5,940 |

103 |

0.78 |

12.5 |

74 |

174 |

|

Netherlands |

960 |

66 |

0.42 |

5.3 |

109 |

75 |

|

Portugal |

340 |

34 |

1.11 |

16.9 |

66 |

65 |

|

Spain |

2,040 |

52 |

0.85 |

12.5 |

62 |

105 |

|

United Kingdom |

4,520 |

80 |

0.67 |

10.8 |

100 |

100 |

|

European Community |

33,000 |

102 |

0.78 |

10.9 |

85 |

149 |

|

United States |

24,000 |

100 |

0.65 |

5.5 |

n/a |

n/a |

|

Japan |

23,000 |

215 |

0.90 |

18.7 |

n/a |

n/a |

|

Percent Market Held by Local Firms |

||||||

|

Pharmaceutical Production (Millions of Dollars) |

Net trade (Millions of Dollars) |

Home |

World |

Innovatory Capacity |

||

|

Belgium |

1,250 |

+160 |

10 |

<1 |

Moderate |

|

|

Denmark |

920 |

+430 |

50 |

<1 |

Moderate |

|

|

France |

10,520 |

+1,310 |

51 |

6 |

Moderate |

|

|

West Germany |

11,750 |

+2,240 |

54 |

11 |

High |

|

|

Greece |

310 |

-60 |

16 |

<1 |

Low |

|

|

Ireland |

400 |

+120 |

10 |

<1 |

Low |

|

|

Italy |

8,450 |

-550 |

42 |

3 |

Moderate |

|

|

Netherlands |

1,170 |

+45 |

12 |

1 |

Moderate |

|

|

Portugal |

450 |

-60 |

17 |

<1 |

Low |

|

|

Spain |

3,360 |

-80 |

30 |

<1 |

Low |

|

|

United Kingdom |

8,000 |

+1,370 |

37 |

8 |

High |

|

|

European Community |

46,500 |

+5,100 |

66 |

30 |

Mixed |

|

|

Switzerland |

3,360 |

+2,030 |

40 |

7 |

High |

|

|

United States |

26,500 |

+960 |

80 |

37 |

High |

|

|

Japan |

22,500 |

-1,500 |

80 |

20 |

High |

|

|

a At manufacturers' prices and 1987 average exchange rates b 1986 c At manufacturers' prices d Per capita consumption/average price |

||||||

THE PROCESS OF INNOVATION

Discovery

The first—and in many ways the crucial—stage in developing a new product is to find new chemical entities (NCEs) with clinical potential. Today, this depends more on advances in scientific knowledge than on serendipity or large-scale screening. In principle, such knowledge is freely available and the discovery stage could be carried out anywhere. In practice, substantial numbers of specialized personnel are needed, together with access to local sources of scientific and technical expertise and the vital infrastructural services, ranging from instrument maintenance to laboratory construction. Accordingly, the size and quality of the local scientific community are central factors. Some qualitative measures of innovative strength and weakness are shown in Table 8.2 and Table 8.3. They are of varied nature, those of Table 8.2 referring specifically to the pharmaceutical industry and those of Table 8.3 to national indicators of scientific inputs and outputs. As far as pharmaceutical innovation is concerned, they show that no single European country has the strength of the United States or, less certainly, Japan. The United Kingdom seems to be in the strongest position at the moment, followed by West Germany and, outside the European Community, Switzerland. France has slipped into the second rank, where it is accompanied by Italy. Belgium, Denmark, and the Netherlands have elements of strength

TABLE 8.2 Measures of the Innovatory Strength in Pharmaceuticals of Various Countries

|

Country |

NCEs Introduced |

Top 50 Drugs in World by Sales, 1987 |

Share of Various Markets, 1987 (Percent) |

||||

|

1974–1980 |

1981–1987 |

EEC |

USA |

Japan |

World |

||

|

Belgium |

11 |

6 |

4 |

<1 |

<1 |

<1 |

|

|

Denmark |

1 |

1 |

1 |

<1 |

<1 |

<1 |

|

|

France |

97 |

26 |

16 |

<1 |

<1 |

6 |

|

|

West Germany |

91 |

30 |

5 |

21 |

4 |

3 |

11 |

|

Italy |

72 |

28 |

1 |

8 |

<1 |

<1 |

3 |

|

Spain |

15 |

1 |

3 |

— |

— |

<1 |

|

|

United Kingdom |

29 |

16 |

10 |

10 |

7 |

3 |

8 |

|

Switzerland |

45 |

26 |

6 |

10 |

8 |

3 |

7 |

|

United States |

153 |

82 |

21 |

22 |

80 |

10 |

37 |

|

Japan |

75 |

92 |

7 |

<1 |

<1 |

80 |

20 |

|

SOURCE: These estimates are based on data from Scrip, various issues, information from IMS Inc., and national governmentsources. |

|||||||

TABLE 8.3 Trends in Pure Scientific Spending and Output

|

Country |

Percent Share of World Scientific Publication, 1984 |

Percent Change, 1975–1984 |

Government Spending (Millions of U.S. Dollars) on Academic Research |

|||

|

Papers |

Citations |

Papers |

Citations |

1982 |

Percent Change, 1975–1982 |

|

|

France |

5.0 |

4.0 |

-14 |

— |

2,590 |

+49 |

|

West Germany |

6.0 |

5.3 |

-7 |

— |

3,300 |

-1 |

|

United Kingdom |

8.1 |

9.9 |

-15 |

-9 |

1,930 |

+6 |

|

United States |

36.6 |

52.8 |

-2 |

+2 |

9,370 |

+13 |

|

Japan |

7.6 |

5.0 |

+41 |

+22 |

3,170 |

+53 |

|

All other |

36.7 |

23.0 |

+3 |

— |

n/a |

n/a |

|

SOURCE: Martin BR, Irvine J, Narin F, Sterrin C. The continuing declineof British science. Nature 1987;330:123–126, and Irvine J, MartinBR. Is Britain spending enough on science? Nature 1986;323:591–593. |

||||||

but are handicapped by their small size. Greece, Portugal, and Spain are frankly weak, although Spain is making serious efforts to overcome her problems.

Such measures of scientific vitality, however, reflect to no small extent the strengths and weaknesses of the past. Given the time that it takes to develop a new drug to the point at which it is marketed, currently over 10 years, the products of the 1980s reflect the scientific strengths and weaknesses of the 1970s. What has happened since? Comprehensive data are lacking, but the numbers of Table 8.3 suggest that there was a substantial decline in the relative position of the United Kingdom in the 1970s and 1980s. West Germany, France, and the United States have held their own, while Japan has improved dramatically. These changes are becoming apparent to U.S. pharmaceutical firms operating in Europe.2

To no small extent these trends are linked to government spending on academic and related research in the several countries. Funding has grown only slowly in the United Kingdom since the early 1970s and is now well below that in comparable countries. The Thatcher administration chose to stress the applications of science and was less sympathetic to the needs of basic research. It also urged industry to pick up a larger share of the basic science bill, a suggestion firmly rejected by the pharmaceutical companies (2). That said, the United Kingdom is still the first choice as a location for foreign pharmaceutical companies setting up R&D centers in Europe. For the time being it continues to provide good—and relatively cheap—scientific manpower and access to high-quality pure research. Whether this happy situation will continue is doubtful (3).

Development and Regulation

The impact of government policies on the discovery phase is indirect. That on the development phase is immediate. In all European countries the admission of medicinal products to national markets is controlled by national agencies that provide guidance about the evidence they need to reach a regulatory decision. The requirements of national authorities have converged gradually as a result of directives by the European Commission, and there is a high degree of apparent uniformity within the Community. Common standards for pharmacological and toxicological tests in animals and for the conduct of clinical trials have been adopted, together with common forms of documentation. Products may be rejected only on the grounds of safety, efficacy, and quality. Abbreviated, less rigorous applications are sufficient for products based on known ingredients.

In practice, however, there are still substantial differences between one country and another. Some are minor and essentially residual, but others are more serious. Some reflect variations in administrative arrangements. The United Kingdom, for instance, relies entirely on the employees of the official agency to make the decisions, whereas France depends on nongovernmental assessors. Differences in regulatory policies also reflect national differences in the practice of medicine and in approaches to clinical assessment.3 Thus, in the United Kingdom and in Scandinavia, the main emphasis is on the large-scale clinical trial. In West Germany it is the pharmacological profile of the product that is most critical. The result is a fragmented European drug approval system. A product has to make its way through 12 national authorities, each of which will apply somewhat different criteria of evaluation (4).

This is expensive and time consuming. How does it affect the process of innovation? Perhaps surprisingly, the answer is “only to a limited extent.” Innovative companies are large and by their very nature sell their products worldwide. Accordingly, they carry out the necessary development work with the world market in mind. Most of them work to meet the regulatory standards of the United States, since commercial success in the U.S. market is highly desirable if not essential and since American standards are the most rigorous to be found anywhere. Accordingly, research-oriented firms prepare new drug approval applications with the Food and Drug Administration (FDA) in mind. Thus, pivotal clinical trials will be undertaken in countries whose clinical practices and regulatory procedures most approximate those of the United States. The United Kingdom and Scandinavia are favored for this reason. The former is especially popular because costs are low; hospitals will generally arrange studies free of charge. Some clinical work will be carried out elsewhere, primarily to familiarize local clinical leaders with the new product. A master dossier will then be prepared from which the new drug application for each individual country may be drawn.

The development process is, of course, still prolonged and expensive, currently taking between 6 and 12 years, depending largely on the nature of the drugs.4 Obtaining a product license can also consume a good deal of time, although generally less than in the United States. Discussions about a unified system of approval have been in progress for some years. Two basic procedures have been suggested: binding mutual recognition and a centralized authority—a European FDA, as its opponents call it. The latest proposals of the European Commission envisage a complex three-tier system. New biotechnology products would be handled by a central agency. For other NCEs companies would be able to choose between this agency and a process of mutual recognition. The central agency would be the arbiter in the case of disagreements between member countries. How this system would work in practice is as yet far from clear.

The regulatory situation in Europe is therefore much like that in the United States. Differences are of degree rather than kind and increasingly marginal. The fragmentation of the European system is an annoyance rather than a major problem; by one estimate a unified approval procedure would produce a saving of no more than 2 percent for the industry (7). This is hardly surprising. The innovative part of the pharmaceutical sector operates on a world basis, and the impact of national peculiarities is reduced correspondingly. But what of the commercial scene?

RECOVERING THE INVESTMENT

Patent Protection

Effective patent protection is vitally necessary to the research-based drug industry. Without a period of qualified monopoly to recover its costs, no company could face the expenditure necessary for innovation. Since the late 1970s, a unified system of patents has applied to most European countries. Under the European Patent Convention, pharmaceutical products, processes, and uses are protected for 20 years from the date of application. The patentee makes a single application and receives a bundle of national patents; as yet there is no Europatent. All member states of the Community, with the exceptions of Ireland and Portugal, have signed the convention, as have Austria, Sweden, and Switzerland. Spain, where patent protection formerly was weak, has adhered to the convention and has been granted a transitional period to bring its practices into line.5

The main concern, of course, is effective patent life. For good reasons patents normally are taken out toward the end of the discovery phase of a new medicine. Given the length of the development stage, the patent life remaining by the time the product reaches the market typically is between 8 and 12 years, and often less (5,6). The inventor therefore has only a limited time to recover R&D costs and to make a profit before copies appear. This

problem was recognized in the United States by the Drug Price Competition and Patent Term Restoration Act (Waxman-Hatch) enacted in 1984 and by similar legislation in Japan. Some progress along these lines has been made in the Community. Under the High Technology Directive of 1987, six member nations—Belgium, France, West Germany, Italy, the Netherlands, and the United Kingdom—have agreed to a 10-year period of marketing exclusivity for all novel pharmaceutical products (8).

In practice this is a rather modest concession. The added patent protection is to start from the date of first marketing within the Community and not the date of authorization in any particular country. Moreover, as mentioned previously, the average period of effective patent life is not far off 10 years already. The commission therefore has proposed a more radical alternative. They envisage the creation of “supplementary protection certificates,” which would provide 16 years patent protection from the date of first marketing authorization for pharmaceuticals based on new active substances, with a ceiling of 30 years from the date of filing the original patent. This would go a long way to solving the industry 's problem. However, opposition to the measure from consumer groups is building up, and a substantial effort will be needed to get it through the European Parliament. In any case it would not come into force for some time and would be retroactive only to a limited extent.

Prices

All European countries are heavily involved in the provision and financing of health care, and all are anxious to limit their expenditure. Aging

TABLE 8.4 General Methods of Controlling Pharmaceutical Expenditure in the European Community, 1989

|

Country |

Positive List |

Negative List |

Patient Copayment System |

Percent Bill Met by Patient |

Generics Promoted |

|

Belgium |

Yes |

Yes |

0/25/50/60 percent of price |

35 |

Yes but |

|

Denmark |

Yes |

No |

25/50/100 percent of price |

33 |

Yes |

|

France |

Yes |

No |

0/30/60/100 percent of price |

30 |

Yes but |

|

West Germany |

No |

Yes |

Flat rate |

10 |

Strongly |

|

Greece |

Yes |

No |

20 percent of price |

n/a |

Yes |

|

Ireland |

No |

Yes |

Varies with patient |

n/a |

No |

|

Italy |

Yes |

No |

30 or 40 percent of price + flat rate |

19 |

Yes but |

|

Netherlands |

No |

Yes |

Flat rate |

12 |

Strongly |

|

Portugal |

Yes |

No |

0/20/50 percent of price |

25 |

Yes |

|

Spain |

Yes |

Yes |

40 percent of price |

14 |

Yes |

|

United Kingdom |

No |

Yes |

Flat rate |

13 |

Strongly |

TABLE 8.5 Price Control Systems in the European Community, 1989

|

Country |

Individual Drug Prices Controlled |

Basis |

Better Price for Local Activities |

Average 1988 Drug Prices [UK = 100] |

||

|

[1] |

[2] |

[3] |

||||

|

Belgium |

Yes |

Internal comparison |

Yes |

74 |

77 |

62 |

|

Denmark |

Effectively no |

No |

103 |

128 |

86 |

|

|

France |

Yes |

Internal comparison |

Yes |

58 |

62 |

48 |

|

West Germany |

Some are |

Flat rate |

No |

113 |

133 |

92 |

|

Greece |

Yes |

Cost plus |

Perhaps |

61 |

65 |

83 |

|

Ireland |

No |

Tied to United Kingdom prices |

No |

112 |

107 |

93 |

|

Italy |

Yes |

Internal comparison |

Yes |

74 |

72 |

63 |

|

Netherlands |

No |

None yet |

No |

109 |

119 |

96 |

|

Portugal |

Yes |

External comparison |

Perhaps |

66 |

55 |

87 |

|

Spain |

Yes |

External comparison |

Yes |

62 |

63 |

70 |

|

United Kingdom |

No |

Profits controlled |

Yes |

100 |

100 |

100 |

populations and the advance of medical science make cost containment politically difficult. Economies are sought, and the first and favorite target is the drug bill. Accordingly, all these nations take steps to limit pharmaceutical spending. Such measures are permitted under the Treaty of Rome. The methods used are summarized in Table 8.4 and Table 8.5. They include positive lists, which name the drugs that will be paid for, and negative lists, which identify products excluded from reimbursement. Patients everywhere are expected to pick up part of the bill, although exemptions for those in the hospital and the chronically sick are normal. The use of generics may also be encouraged. Over-the-counter medicines are everywhere excluded, although the same products often qualify for reimbursement if they are prescribed. The main emphasis, however, is on direct control of pharmaceutical prices.

The majority of states in the European Community regulate the prices of individual drugs. Cost-plus, in which the permitted price is based on the cost of production, together with allowances for the R&D content and for marketing expenditure, was formerly the favored method for fixing prices. It is, however, cumbersome to apply and has been replaced generally by other approaches. Internal comparison is now used by several countries. Here the price of a new medicine is fixed by reference to existing products in the same therapeutic category; an improved tolerance/efficacy profile or other clinical advantages will result in a better price. Yet other nations rely on external comparison, in which prices are related to those in other European countries.6

However, measures of this kind are not universal. Denmark and the

Netherlands do not control prices at all. Until very recently, West Germany also followed a policy of free prices; now, though, it restricts reimbursement under the health insurance scheme for identical multisource drugs to a fixed sum that is related to the generic price. At some future point it intends to extend this scheme to medicines that share a common mode of physiological action. Uniquely, the United Kingdom controls profits on sales to the National Health Service. Companies are allowed to set their own prices, provided that their return on capital does not exceed a certain specified level (9).

The main effect of these controls is that prices differ widely between one country and another. The average price level in Spain, for example, is about half that in West Germany. Nor are low prices necessarily related to low per capita incomes. France is a country appreciably richer than the United Kingdom, yet because of government controls, drugs are much cheaper there. This leads to serious problems for the research-based pharmaceutical companies.

In some countries prices are barely sufficient to support the costs of innovation. France again is an example. During their formative years, French companies were granted an extensive degree of protection from outside competition, which has led to them being abnormally dependent on sales in the French domestic market and the former French colonies. Several of their innovative firms clearly are suffering from low domestic prices (10). Companies with a world wide perspective, such as those of West Germany, Switzerland, and the United Kingdom, are less affected by low prices in any particular country but cannot welcome the example that they set to regulators elsewhere.

A further problem arising from variations in price between one country and another is parallel importing. This is a form of arbitrage. A company in a country where prices are high exports a drug to one where prices are low. A wholesaler buys it there at the local price and exports it back to its country of origin, where it is sold at the normal higher price. The reexporter and the pharmacist divide the profit. Parallel exports are entirely legal within the Community, even when the price differences that make them worthwhile are due to government action. This form of trade is rising and threatens to exert constant downward pressure on drug prices in those countries where they are currently high. The major companies operating in Europe see this as a serious threat.7

Uniform pan-European prices are unlikely. Under the Treaty of Rome, such matters are left to individual governments, each of which has its own ideas about the balance between the interests of producers and consumers. Thus, despite continued pressure from the international industry, successive French governments have kept drug prices low, arguing that the French propensity to consume drugs is so great ( Table 8.1 ) and so price inelastic that higher prices would bankrupt the national health insurance scheme.8 In con

trast, the British government generally has tolerated fairly high prices because, by European standards, British consumption of medicines is modest. The possible effects of the recent transparency directive are discussed later.

Generics

The United States has chosen to promote competition in the out-of-patent drug market by encouraging the use of generic products. This has been successful in that generics now account for a large minority of total sales. It has been less successful in controlling total expenditure, since average price levels have risen sharply in recent years as innovative firms have charged the very highest prices the market will bear for novel products.

Generics have made less impact in Europe. They probably have no more than 5 percent by value of the Community market. In only two major countries—West Germany and the United Kingdom, both of which have high prices—do generics have as much as 10 percent of the market. Elsewhere they are much less important. In part, this is because prices are too low in some countries—Belgium, France, Italy, Spain —to make competition by price commercially attractive. In part, it is because only West Germany permits generic substitution, although that measure is now under discussion in Italy and being mentioned in France, and, in part, it is because governments have preferred to control pharmaceutical expenditure by the means already discussed in the previous section (11).

This situation is likely to change in the not-too-distant future. European governments are keenly interested in each other's cost-containment programs, and if generic substitution were to prove successful in West Germany, it might be widely adopted. Once again, this could have serious consequences for the income of research-based companies, unless concessions such as extended patent lives were to be granted. European firms fear that the use of generics would be combined with price controls and that their combined effect would therefore be larger than in the United States.9

SUBSIDIES FOR R&D

Many European governments have wished to encourage the development of a strong domestic pharmaceutical industry. At first, the objective was import substitution, especially in the remote days of the dollar shortage.10 Later, a modern, science-based drug industry was seen as desirable in itself, generating a substantial contribution to the national income, the balance of payments, and employment opportunities for skilled and highly educated personnel.

What methods were used to this end? In the early days tariff or nontariff barriers were common; they survived in Spain and Portugal until their accession to the Community in 1986.11 Ireland used subsidies and tax exemptions as

incentives for high-technology, export-oriented industries, such as pharmaceuticals. At present, the main role is played by controls over prices and profits discussed above. An important if latent characteristic of regulations is flexibility—the ability to be relaxed on occasion. For example, a better price for a new wonder drug or a price increase for an existing one may be the reward for increased local investment.

Financial incentives such as preferential pricing have had some effect on the location of R&D facilities. At first, they tended to follow manufacturing investment. Local laboratories were set up for local development work. More recently, major centers undertaking basic research have been set up by foreign companies in several countries, especially in France and the United Kingdom. The French have been particularly aggressive in this respect, offering substantial improvements on product prices determined by the process of internal comparison in return for R&D investment in France. Since French prices are low, such trade-offs can be attractive. Italy and Spain offer similar rewards. The United Kingdom explicitly takes local R&D into account in fixing the permitted profit levels for individual companies. Only West Germany, the Netherlands, and Denmark stand aloof (12).

Such incentives discriminate between companies. They naturally favor indigenous firms above all, since all multinational pharmaceutical enterprises do their most fundamental and sensitive research in their country of origin. They also have a distorting effect on trade. Their legality under the Treaty of Rome therefore is uncertain. Previous Belgian and Italian schemes were struck down by the European Court of Justice, 12 but the French system has so far survived because it is entirely informal in nature. The incentives provided by the United Kingdom appear to be permissible: the concessions offered are not directly connected to any particular investment; they are, in effect, made retrospectively, and they amount to no more than a chance to make a particular level of profit. There is no guarantee that such a profit will be obtained.13

The recent Transparency Directive of the European Commission, which came into force on January 1, 1990, will probably have a significant effect on incentives for R&D. Put briefly, it stipulates that member countries must publish full details of the methods they use to classify products for reimbursement, to control pharmaceutical prices and profits, and to operate positive and negative drug lists. A 180-day period for the approval or disapproval of prices or price increases is laid down. If such a price proposal is rejected, the applicant must be given a statement of the reasons based on “objective and verifiable criteria.” In the absence of a decision, the company may apply its price forthwith (13).

In principle the directive might expose the use of price concessions as incentives. The initiative would, however, have to be taken by a company or companies that felt unfairly treated. To do so might risk compromising relations with the government in question. To be the first to sue would be to put oneself in an uncomfortably exposed position.

THOUGHTS

What has been the impact on pharmaceutical R&D in Europe of the various forms of government regulation outlined in this chapter? Specifically, how have they affected the European environment for innovation compared to that in the United States?

Is the United States a Better Place for Pharmaceutical Innovation?

By and large, the answer is yes. In some areas there is little difference between Europe and the United States. In both the development stage of product innovation is prolonged and expensive. On the whole, it still seems to be rather easier to get a new medicine to the market in Europe. The differences are not large, however, and are tending to become smaller with time. In any case, if drug approval delays in the United States are greater than those in Europe, it is the American consumer who suffers rather than the American pharmaceutical industry. To be denied effective drugs for whatever reason is a loss in welfare. Similarly, differences in patent protection are small. The Drug Price Competition and Patent Term Restoration Act has given the United States a slight edge, but, when implemented, the proposals of the European Commission should shift the advantage back to Europe.

The United States does, however, have a real advantage in two areas. The first is the fundamental resource of basic science. Crude as they are, the data presented in Table 8.3 show the dominance of the United States over all other countries. In terms of both publications and citations, it is clearly much more prolific than the entire European Community. This is equally true when one considers the branches of science that are directly relevant to the pharmaceutical industry, such as cell biology, genetics, immunology, and computer modeling. In a science-driven industry like pharmaceuticals, this gives the United States a substantial lead over others when radically new approaches and techniques are required. In this light the continued American dominance of pharmaceutical innovation is hardly surprising.

The other advantage of the United States lies in free and relatively high drug prices. Innovation is expensive and, as previously shown, price levels in some European countries are too low to provide adequate support. Does this matter? After all, new medicines have to sell worldwide, and the income from any one country is only a minor part of the whole. In practice, however, all companies depend to a quite disproportionate degree on their own local markets or regions (Table 8.2 ). If local prices are low, profits and return on investment will be low. Once again, the position of the French companies illustrates this problem.

The R&D incentives provided by several European countries are significant but do not provide a sufficient stimulus for innovation. Their impact is

relatively small. In a recent inquiry American firms operating in Europe rated these incentives as not very important. They have had only a modest effect on the location of R&D facilities. As has been seen, the future of such schemes is in any case problematic. From the standpoint of the European pharmaceutical industry as a whole, this is all to the good. Incentives in the form of better prices for local investment discriminate between companies and may distort policies concerning the location of R&D facilities. Opportunities to exploit economies of scale and scientific critical mass may be lost. In addition, companies may be led to neglect scientific opportunities outside their own countries or outside the community.

Are There Lessons for the United States from the European Experience?

One can look on the European experience of pharmaceutical regulation as a series of large-scale natural experiments. What lessons could the United States learn from them that might improve the efficiency of the innovatory process? As the previous section has suggested, most of these policies inhibit innovation. Where European regulatory practice has differed from that of the United States, it has usually been for the worse. Nevertheless, it is worth considering whether there are any exceptions to this gloomy conclusion.

One area that has already been mentioned is marketing authorization for new products. The procedures used in the various European countries appear to be rather more rapid and appreciably more flexible than those of the FDA. This owes something to differences in the position of the regulators. Despite considerable variations between one European country and another, the senior decision makers are always independent, high-status professionals rather than career bureaucrats. Unlike their American colleagues, they are generally sheltered from the blasts of political controversy and are freer to exercise their judgment.

Moreover, the legal situation is probably more favorable in Europe. Europeans seem to be less litigious than Americans. Class action suits generally are illegal, as are contingency fees. Although strict liability for manufacturers has now been agreed upon by the Community, most member countries have introduced or are expected to introduce a development risk proviso, which will exclude damages from causes that could not have been foreseen at the time a drug was introduced. Several countries—most notably Sweden— have experimented with no-fault compensation schemes, with encouraging results in relations between the industry and the public.

Finally, there are promising developments in the field of post-marketing surveillance of drugs in Europe. For instance, new computer-based systems being introduced in the United Kingdom will make it possible to track indefinitely the effects of particular drugs on particular patients. An effective system of surveillance is at hand and, in principle, could even replace to some extent the lengthy pre-marketing clinical trials now required.14

Such developments could have an appreciable effect on the time it takes to bring a new drug to the market. There is a reasonable chance that such practices will be adopted widely in Europe during the next few years. Whether they could be transferred to the United States is more doubtful. As already suggested, the advantages the European countries enjoy are the result of cultural factors as much as anything. Ambulance-chasing lawyers and acrimonious congressional hearings are as permanent a feature of American life as obsessional anxiety about health. All would make a general relaxation of drug regulation difficult.

1992 and After

During 1992, the member countries of the European Community will form a single unified market, with all that implies. As far as the European pharmaceutical industry is concerned, this will initiate yet another stage in a process of changing economic dynamics. Many issues, notably prices, remain unresolved. At the same time the trend toward ultimate unification is both clear and unstoppable. What are the implications for pharmaceutical R&D?

A unified system of marketing authorization is likely to be in place by 1993. It could reduce approval times or lengthen them, depending on the policies followed. In the long run prices might be harmonized, but would the revision be upwards or downwards and where would it be felt? Longer effective patent lives and the phasing out of local incentives for R&D seem both probable and beneficial. If the European Commission were to play a larger part in health policy—and this cannot be ruled out if there is further progress toward a federal Europe —this might mean either more or less regulation. Much remains to be determined.

Who is likely to benefit? Increased competition will impact adversely on the smaller and more marginal research-based firms, to the benefit of the larger and stronger ones. Unified marketing authorization and longer patent lives will benefit those who have new products to introduce. The decline of incentives will benefit those who can stand on their own. It will also help those firms that have been forced in the past to fragment their European activities. Concentration will be the policy of the future. The strong will become stronger and the weak weaker.

American companies stand to benefit from 1992. By international standards they are large and innovative. Their competitive position is already very strong. They are firmly entrenched in Europe, where they have more than 20 percent of the market by value; virtually all they sell is produced locally. They will gain considerably from the opportunity to concentrate their European activities. They are well placed to exploit their existing contacts with the European scientific community.

It is difficult to be as optimistic about the competitive position of the European drug companies. In terms of innovative capacity, the French companies are now in the second rank; the Italian ones have always been

there. There are signs that the Swiss and German firms are losing their edge. The British companies are still riding high, but it is distinctly possible that the foundation of their success is being eroded. As the nature of innovation changes, all will have to adapt or vanish. Whether they will be able to do so remains to be seen.

NOTES

1. The Treaty of Rome is the basic law creating and governing the European Community. The provisions particularly affecting the pharmaceutical industry are articles 30, forbidding quantitative restrictions on imports; 85, prohibiting restrictions on competition; 86, relating to abuse of a dominant market position; and 92, governing the provision of state aid to industry. The European Court of Justice is the Supreme Court of the Community. Its decisions are binding on member nations. It has been very active and has consistently interpreted article 30 in particular in the broadest way.

2. In the case of the United Kingdom the decline between 1973 and 1982 was especially marked in the case of chemistry but less so in biomedical research and clinical medicine. This trend seems to have continued in the 1980s but at a slower pace (2).

3. These differences appear to be related to the way in which physicians are trained. There are basically three medical cultures in Europe —one common to the United Kingdom, Ireland, the Netherlands, and Scandinavia, one common to Belgium, France, Italy, and Spain, and one unique to Germany and Switzerland. Both the volume of drugs consumed and their nature vary markedly between the three areas.

4. In the United Kingdom drug development time peaked at 13 years in 1984, subsequently falling to 10 years in 1987. The largest element was clinical testing, which accounted for two-thirds of the total. Central nervous system drugs spent twice as long in the development phase as anti-infective products (6). An earlier estimate (7) suggested 1982 figures of seven years for France, nine for Switzerland, 11 for Italy, and 12 for the United Kingdom (3).

5. Ireland has adhered to the Convention but has failed to give it effect by national legislation. Both Portugal and Spain were obliged to adhere to the Convention before 1992 as a condition of entering the Community in 1986. While Spain has done so, Portugal has not and continues to offer only process patents with a life of 15 years from the date of grant.

6. Countries such as Spain which use external comparison to fix prices naturally tend to use the countries where drugs are cheapest—usually France or Greece— as their point of reference.

7. Pharmaceutical companies market their products themselves but do not distribute them, since the number of outlets to be supplied is very large. Instead, they sell to specialist wholesalers who in turn supply retail pharmacies. National health services and insurance schemes normally reimburse retailers at prices based on manufacturers ' list prices for the prescription drugs that they dispense. Clearly, the lower the price at which the distributor can obtain a drug, the greater his or her profit margin.

8. The elasticity of demand with price is the ratio of the proportionate increase in volume sold to the proportionate decrease in price. Thus, if a 1 percent decrease in price produces a 2 percent increase in sales, the elasticity is 2. A little calculus shows that if the elasticity of demand is less than 1, expenditure (i.e., price × volume) will increase when the price is increased. In so far as it can be measured the elasticity of demand for drugs is well below one in all countries.

9. Under the Drug Price Competition and Patent Term Restoration Act research-based United States companies received a qualified extension of patent life; in return they had to allow the information in their original new drug applications to be available to generic companies when the latter applied for marketing authorization. This meant that the generic firms only had to demonstrate to the FDA that their copies were of satisfactory quality and had the requisite bioequivalence and bioavailability. Formerly they had to undertake a full program of testing if the product they wished to copy had been introduced after 1962. This information has always been available to would-be generic copiers in European countries; accordingly some other, and less welcome, quid pro quo for patent life extension may well be sought.

10. Between 1945 and 1955 all European nations suffered from an acute lack of dollars as they underwent reconstruction after World War II. In order to conserve foreign exchange many of them encouraged United States firms to set up local subsidiaries; this was a major stimulus to the multinational system of operation in the pharmaceutical industry.

11. Tariff barriers were widely used to encourage local investment in the 1950s and early 1960s. Illegal under the Treaty of Rome, they have now been eliminated within the Community. Non-tariff barriers comprise measures such as unusual safety or packaging requirements which have the effect of restricting imports. An example is the Japanese demand that all safety testing of drugs be carried out on Japanese subjects. They too have largely disappeared within the Community.

12. In both cases the Court struck down the schemes as contrary to article 30 of the Treaty of Rome because they laid down different criteria for imported and domestically produced drugs, thereby explicitly discriminating in favor of domestic products.

13. I am grateful to a senior official of the United Kingdom Department of Health for clarifying the legal status of the United Kingdom scheme and to spokesmen of the Société Nationale de l'Industrie Pharmaceutique for discussions on how the French pricing system works.

14. Two commercial systems are already in existence. That of VAMP Ltd. covers about 20 percent of all United Kingdom medical practices. The information obtained is collected regularly, analyzed, and sold to pharmaceutical firms.

REFERENCES

1. Martin BR , Irvine J , Narin F , Sterrin C. The continuing decline of British science . Nature 1987 ; 330 : 123-126 .

2. Irvine J , Martin BR. Is Britain spending enough on science? Nature 1986 ; 323 : 591-593 .

3. Burstall ML , Wallerstein K. American Pharmaceutical Companies in Britain and Europe, unpublished .

4. Burstall ML , Reuben BG. The Cost of Fragmentation in the European Community's Pharmaceutical Industry and Market . Brussels : European Community 1988 : 52-67 .

5. Lis Y , Walker SR. Novel medicines marketed in the United Kingdom 1960-1987 . British Journal of Clinical Pharmacology 1989 ; 28 : 333-343 .

6. Chew R , Teeling-Smith G , Wells N. Pharmaceuticals in Seven Nations , London : Office of Health Economics , 1985, Table 26, p. 39.

7. Burstall ML , Reuben BG. The Cost of Fragmentation in the European Community's Pharmaceutical Industry and Market . Brussels : European Community 1988 : 90-99 .

8. European Commission . Report from the Commission on the Activities of the Committee for Proprietary Medicines [COM (88) 143 Final] .

9. Association of the British Pharmaceutical Industry (ABPI) and the United Kingdom Department of Health and Social Services (DHSS) : The Pharmaceutical Price Regulation Scheme, 1986.

10. See the company-by-company information given in the annual issues of Scrip's Pharmaceutical League Tables, 1981/2 to date. Richmond-on-Thames : PJB Publications .

11. Burstall ML. Generic Pharmaceuticals in Europe—Blessing or Threat? London : Economists Advisory Group Ltd. , 1986 , pp. 16-32, 47-55 .

12. Burstall ML , Wallerstein K. American Pharmaceutical Companies in Britain and Europe, unpublished.

13. Council Directive relating to the Transparency of Measures Regulating the Pricing of Medicinal Products for Human Use and Their Inclusion Within the Scope of National Health Insurance Systems [COM (88) 231. OJ C 129, 18/5/1988] .