2

What Can Policymakers Learn From Natural Resource Accounting?1

Robert Repetto

World Resources Institute

Washington, D.C.

THE NEED FOR NATURAL RESOURCE ACCOUNTING

Whatever their shortcomings, and however little their construction is understood by the general public, the national income accounts are undoubtedly one of the most significant social inventions of the twentieth century. Their political and economic impact can scarcely be overestimated. However inappropriately, they serve to divide the world into "developed" and "less developed" countries. In the "developed'' countries, whenever the quarterly gross national product (GNP) figures emerge, policymakers stir. Should they be lower, even marginally, than those of the preceding three months, a recession is declared, the strategies and competence of the administration are impugned, and public political debate ensues. In the ''developing" countries, the rate of growth of gross domestic product (GDP) is the principal measure of economic progress and transformation.

The national accounts have become so much a part of our life that it is hard to remember that they are scarcely fifty years old. They were first published in the United States in the year 1942. It is no coincidence that the period during which these measures have been available, with all their imperfections, has been the period within which governments in all major countries have taken responsibility for the growth and stability of their economies, and during which enormous investments of talent and energy have been made in understanding how economies can be better managed. Forecasting the next few quarterly estimates of these statistics has become, with no exaggeration, a hundred million dollar industry.

The aim of national income accounting is to provide an information framework suitable for analyzing the performance of the economic system. The current system of national accounts reflects the Keynesian macroeconomic model that was dominant when the system was developed, largely through the work of Richard Stone, Simon Kuznets and other economists writing in the English tradition. The great aggregates of Keynesian analysis—Consumption, Savings, Invest

ment, and Government Expenditures—are carefully defined and measured. But Keynes and his contemporaries were preoccupied with the Great Depression and the business cycle; specifically, with explaining how an economy could remain for long periods of time at less than full employment. The least of their worries was a scarcity of natural resources. Unfortunately, as Keynesian analysis largely ignored the productive role of natural resources, so does the current system of national accounts.

In fact, natural resource scarcity was of little concern to 19th-century neo-classical economics, from which tradition Keynesian and most contemporary economic theories are derived. Gone were the dismal predictions of Ricardo, Malthus, Marx, and other earlier classical economist that scarcity of agricultural land in industrial economies would cause stagnation or collapse because of rising rents and falling real wages. In 19th-century Europe, steamships and railroads were markedly lowering transport costs, while foodgrains and raw materials were flooding in from North America, Argentina, Australia, Russia, and the imperial colonies. What mattered to England and other industrializing nations was the pace of investment and technological change.

The classical economists had regarded income as the return on three kinds of assets: natural resources, human resources, and invested capital (land, labor, and capital, in their vocabulary). The neo-classical economists virtually dropped natural resources from their model, and concentrated on labor and invested capital. When these theories were applied after World War II to problems of economic development in the Third World, human resources were also left out on the grounds that labor was always "surplus," and development was seen almost entirely as a matter of savings and investment in physical capital. Ironically, low-income countries, which are typically most dependent on natural resources for employment, revenues, and foreign exchange earnings are instructed to use a system for national accounting and macroeconomic analysis which almost completely ignores their principal assets. It is not far from the truth that the system of national accounts represents one of the last vestiges of British colonialism.

As a result, there is a dangerous asymmetry in the way we measure, and hence, the way we think about, the value of natural resources. Man-made assets—buildings and equipment, for example—are valued as productive capital. The increase in the stock is recorded as capital formation. Decreases in the stock through use are written off against the value of production as depreciation. This practice recognizes that a consumption level maintained by drawing down the stock of capital exceeds the sustainable level of income. Natural resource assets are not so valued, and their loss entails no debit charge against current income that would account for the decrease in potential future production. A country could exhaust its mineral resources, cut down its forests, erode its soils, pollute its aquifers, and hunt its wildlife and fisheries to extinction, but measured income would not be affected as these assets disappeared.

The proper definition of income encompasses the notion of sustainability. In accounting textbooks and economics principles, income is defined as the maximum amount which the recipient could consume in a given period without reducing the amount of possible consumption in a future period. This income concept encompasses not only current earnings but also changes in asset positions. The depreciation accounts reflect the fact that unless the capital stock is maintained and replaced, future consumption possibilities will inevitably decline. Thus, proper evaluation of changes in the stock of assets is crucial as a way of evaluating the sustainability

of an economic development strategy. In resource-dependent countries, failure to extend this concept to the capital stock embodied in natural resources, which are such a significant source of income and consumption, is a major omission and inconsistency.

Underlying this anomaly is the implicit and inappropriate assumption that natural resources are so abundant that they have no marginal value. This is a misunderstanding. Whether they enter the marketplace directly or not, natural resources make important contributions to long-term economic productivity, and so are, strictly speaking, economic assets. Many are under increasing pressure from human activities and are deteriorating in quantity or quality.

Another misunderstanding underlies the contention that natural resources are "free gifts of nature," so that there are no investment costs to be "written off." The value of an asset is not its investment cost, but the present value of its income potential. Many billion-dollar companies have as their principal assets the brilliant ideas and inventions of their founders: the Polaroid Camera, the Apple Computer, the Lotus Spreadsheet, for example. These inspired inventions are worth vastly more than any measurable cost to their inventors in developing them, and could also be regarded as the products of genius—free gifts of nature. Common formulas for calculating depreciation by ''writing off" investment costs (e.g., straight-line depreciation) are just convenient rules of thumb, or artifacts of tax legislation. The true measure of depreciation, which statisticians have tried to adopt for fixed capital in the national accounts, is the capitalized present value of the reduced future income stream obtainable from an asset, because of its decay or obsolescence. Thus, in the same sense that a machine depreciates, soils depreciate as their fertility is diminished, since they can produce only at higher costs or lower yields.

Codified in the United Nations System of National Accounts (SNA) closely followed by most countries, this bias provides false signals to policymakers. It reinforces the false dichotomy between the economy and the "environment" that leads policymakers to ignore or destroy the latter in the name of economic development. It confuses the depletion of valuable assets with the generation of income. Thus it promotes and seems to validate the idea that rapid rates of economic growth can be achieved and sustained by exploiting the resource base. The result can be illusory gains in income and permanent losses in wealth.2

The United Nations SNA recognizes certain natural resources, such as forests, land, and subsoil minerals, as assets in national balance sheets, the "stock" accounts. The recommended treatment for natural resources in the balance sheet accounts is very similar to the recommended treatment of other capital assets. If possible, the assets' values should be derived from market transactions. Otherwise, the accounts should be based on the discounted present value of estimated future income flows derived from the assets. However, the income and product accounts are not treated consistently with these balance sheet accounts. On the income side, for example, the total value added from resource extraction is included in wages and salaries, in

rental incomes and in company profits. In other words, the total value of natural resources current production, net of purchased inputs, is imputed to current income.

The problem is that, in contrast with the treatment of man-made capital assets, there are no accounting entries in the flow accounts for changes in natural resource stocks. Notwithstanding the economic significance of wasting natural resources, the SNA does not provide a debit on the product side of the national income accounts to show that depreciation of natural resources is a form of disinvestment. And it does not provide a depreciation factor on the income side to show that consumption of productive natural resource assets must be excluded from gross income.

Indeed, natural resource assets are legitimately drawn upon to finance economic growth, especially in resource-dependent countries. The revenues derived from resource extraction finance investments in industrial capacity, infrastructure, and education. A reasonable accounting representation of the process, however, would recognize that one kind of asset has been exchanged for another, which is expected to yield a higher return. Should a farmer cut and sell the timber in his woods to raise money for a new barn, his private accounts would reflect the acquisition of a new asset, the barn, and the loss of an old asset, the timber. He thinks himself better off because the barn is worth more to him than the timber. In the national accounts, however, income and investment would rise as the barn is built, but income would also rise as the wood is cut. Nowhere is the loss of a valuable asset reflected. This can lead to serious misestimation of the development potential of resource-dependent economies, by confusing gross and net capital formation. Even worse, should the proceeds of resource depletion be used to finance current consumption, then the economic path is ultimately unsustainable, whatever the national accounts say. If the same farmer used the proceeds from his timber sale to finance a winter vacation, he would be poorer on his return, and no longer able to afford the barn, but national income would only register a gain, not a loss, in wealth.

Consider the sad exemplary tale of Kiribati, the small atoll republic of the Solomon Islands, which depended throughout the 20th century on its phosphate mines for income and government revenues. While the mines ran, gross domestic product was high and rising, but the mining proceeds were treated as current income rather than as capital consumption. When the deposits were mined out in the 1970s, income and government revenues declined drastically, because far too little had been set aside for investment in other assets that would replace the lost revenues.

THE SCOPE OF NATURAL RESOURCE ACCOUNTING

A growing body of expert opinion has recognized the need to correct the SNA's environmental blindspots. Many leading economists, including several Nobel prizewinners, have identified the need for better accounting for natural resource assets. A number of Organization for Economic Cooperation and Development (OECD) nations, including Canada, France, Germany, the Netherlands, Japan, Norway, and the United States have set up or are working on systems of environmental accounts.

The French natural patrimony accounts, for example, are intended as a comprehensive statistical framework to provide authorities with the data they need to monitor changes in "that

subsystem of the terrestrial ecosphere that can be quantitatively and qualitatively altered by human activity."3 Like their Norwegian counterparts, these accounts cover nonrenewables, the physical environment, and living organisms. Since material and energy flows to and from economic activities form only a subset of these accounts, they are conceptually much broader than the national income accounts, and are compiled largely in physical terms.

Such environmental statistics may well encourage decisionmakers to consider the impacts of specific policies on the national stock of natural resources. However, physical accounting by itself has considerable shortcomings. It does not lend itself to useful aggregation: aggregating wood from various tree species in cubic meters obscures wide differences in the economic value of different species. Aggregating mineral reserves in tons obscures vast differences in the value of different deposits, due to grade and recovery costs. Yet, maintaining separate physical accounts for particular species or deposits yields a mountain of statistics that are not easily summarized or used.

A further problem is that accounts maintained only in physical units do not enable economic planners to understand the impact of economic policies on natural resources and thereby integrate resource considerations into economic decisions—presumably, the main point of the exercise. Yet, there is no conflict between accounting in physical and economic units because physical accounts are necessary prerequisites to economic accounts. If the measurement of economic depreciation is extended to natural resources, physical accounts are inevitable by-products.

The limits to monetary valuation are set mainly by the remoteness of the resource in question from the market economy.4 Some resources, such as minerals, enter directly. Others, such as groundwater, contribute to market production, and can readily be assigned a monetary value although they are rarely bought or sold. Others, such as noncommercial wild species, do not contribute directly to production and can be assigned a monetary value only through quite roundabout methods involving many somewhat questionable assumptions. While research into the economic value of resources that are remote from the market is to be encouraged, common sense suggests that highly speculative values should not be included in official accounts.

In industrial countries where pollution and congestion are mounting while economies are becoming less dependent on agriculture, mining, and other forms of primary production, the focus has been on "environmental accounting" rather than natural resource accounting. Several approaches to developing more comprehensive systems of national income accounting go well beyond the scope of natural resource accounting.

There are sound reasons to begin by focusing on accounting for natural resources: the principal natural resources, such as land, timber, and minerals are already listed in the SNA system as economic assets, although not treated like other tangible capital, and their physical and economic values can be readily established. Demonstrating the enormous costs to a national

economy of natural resource degradation is an important first step in establishing the need for revamping national policy.

Developing countries whose economies are dependent on natural resources are becoming particularly interested in developing an accounting framework that accounts for these assets more adequately. Work is already under way in the Philippines, China, Thailand, India, Brazil, Chile, Colombia, Costa Rica, E1 Salvador, and other countries.

SETTING UP NATURAL RESOURCE ACCOUNTS

Physical Accounts

Natural resource physical stocks at any time, and changes in those stocks during an accounting period, can be recorded in physical units appropriate to the particular resource. The basic accounting identity is that opening stocks plus all growth, increase, or addition less all extraction, destruction, or diminution equals closing stocks. Although the following discussion refers to petroleum reserves and timber stocks as examples, the principles are applicable to many other resources.

Petroleum resources consist of identified reserves and other resources: identified reserves can be divided into proven reserves and probable reserves. Proven reserves are the estimated quantities of crude oil, natural gas, and natural gas liquids which geological and engineering data indicate with reasonable certainty to be recoverable from known reservoirs under existing market and operating conditions (i.e., prices and costs as of the date the estimate is made). Probable reserves are quantities of recoverable reserves that are less certain than proven reserves. Thus, one limit on the stock of reserves is informational. Additional proven reserves can usually be generated by drilling additional test wells or undertaking other exploratory investments to reduce uncertainty about the extent of known fields. The boundary between reserves and other resources is basically economic. Vast quantities of known hydrocarbon deposits cannot be extracted profitably under current conditions. They are thus known resources, but cannot be counted as current reserves, although price increases or technological improvements might transform them into reserves in the future.

For other mining industries, geological characteristics tend to be known with more certainty, so there is less distinction between proven and probable reserves but a sharp division between economic reserves and total resources. Many minerals are present at very low concentrations in the earth's crust in almost infinite total amounts. Technological changes in mining and refining processes have markedly reduced the minimum ore concentrations that can profitably be mined, correspondingly expanding mineral reserves.

Changes in oil and gas stocks may be classified under various headings: "discoveries," the quantity of proven reserves that exploratory drilling finds in new oil and gas fields, or in new reservoirs in existing oil fields; "extensions," increases in proven reserves because of subsequent drilling showing that discovered reservoirs are larger than originally estimated; and, "revisions,'' increases in proven reserves because oil or gas firms acquire new information on market conditions or new technology. Extensions of and revisions to oil and gas reserves have historically been significantly larger than new discoveries. Reserve statistics generally produce

very conservative estimates of the total resource stocks that will ultimately enter the economic system: actual production from new U.S. fields and reservoirs was over seven times the amount initially reported as discovered.

Reserve levels fall because of extraction and downward revisions. In the United States, oil and gas companies are required by the Securities and Exchange Commission to disclose net annual changes in estimated quantities of oil and gas reserves, showing separately: opening and closing balances; revisions of previous estimates (from new information); improved recovery (resulting from improved techniques); purchases and sales of minerals in place; extensions and discoveries; and production (Financial Accounting Standards Board, 1982).

The accounting framework for timber resources in physical units could be expressed in hectares, in tons of biomass, or in cubic meters of available wood, although the last is probably the most important economic measure. As in the case of minerals, the total resource is larger than the economic reserve, since a substantial part of the total stock of standing timber in any country cannot be profitably harvested and marketed with current technologies and market conditions.

Additions to the timber stock can originate from growth and regeneration of the initial stock, and from reforestation and afforestation. Reductions can be classified into production (harvesting), natural degradation (fire, earthquake, etc.), and deforestation by man. Separate accounts might be established for different categories of timber stands, for example, virgin forests, logged (secondary) forests, unproductive or protected forests, and plantations. In temperate forests, where species diversity is limited, timber stocks are further disaggregated by species.

Physical accounts can be constructed along similar lines for agricultural land. Land and soil maps and classification systems are used to disaggregate land into productivity categories. Changes in stocks of each land category within a period reflect various phenomena: conversion to nonagricultural uses; conversion to lower productivity classes through physical deterioration by erosion, salinization, or waterlogging; and conversions to higher productivity classes through physical improvements by irrigation, drainage, and other investments. A set of physical accounts for agricultural land would record stocks of land at each accounting date by productivity class, and flows among classes and to other land uses according to cause.

Similarly, physical accounts can be set up for other biological resources, such as wildlife or fish populations. The principles are essentially those of demography. Additions to initial populations are attributed to fertility, estimated from reproduction rates and the size of the breeding population, and inmigration. Subtractions from stocks are attributed to natural mortality, estimated from age-specific or general mortality rates, harvesting operations, other special sources of mortality, and outmigration.

Valuation Principles

The concept of economic rent is central to natural resource valuation. Economic rent is defined as the return to any production input over the minimum amount required to retain it in its present use. It is broadly equivalent to the profit that can be derived or earned from a factor of production (for example, a natural resource stock) beyond its normal supply cost. For

example, if a barrel of crude oil can be sold for $10 and costs a total of $6 to discover, extract, and bring to market, a rent of $4 can be assigned to each barrel. in forest economics, the concept of "stumpage value" is very close to that of economic rent. Stumpage value represents timber sale proceeds, less the costs of logging, transportation and processing. Better quality and more accessible timber stands will command a higher stumpage value.

Rents to natural resources arise from their scarcity, and from locational and other cost advantages of particular stocks. In principle, rents can be determined as the international resource commodity price less all factor costs incurred in extraction, including a normal return to capital but excluding taxes, duties and royalties. Thus, the economic rent is equivalent to the net price.

This is equivalent to the economic rent in a Ricardian scarcity model, which assumes that resources from different "deposits" will be supplied at a rising incremental cost until profit on the marginal source of supply is completely exhausted. In this Ricardian model, rents arise on relatively low-cost, inframarginal sources of supply.

It is also equivalent to a user cost in a Malthusian stock scarcity model, which assumes that a homogeneous exhaustible resource is exploited at an economically efficient rate, a rate such that the profit on the marginal amount brought to market is equal to the expected return derived from holding the asset in stock for future capital gain. In such a Malthusian model, if the resource is being extracted at an efficient rate, the current rent on the last unit of resources extracted is thus equal to the discounted present value of future returns from a unit remaining in stock.

The gross operating surplus of the extractive sector in the SNA, represented by the sum of the profits made by all the different enterprises involved in resource extraction activities, does not represent true rewards to factors of production alone but also reflects rents from a "one time only" irredeemable sale of a nonrenewable natural asset. The basic definition of income as the amount which can be consumed without becoming worse off is clearly being infringed as the value of the asset base declines.

Asset transactions in natural resources, such as competitive auction sales of fights to extract timber or minerals, closely follow estimated stumpage values or rents, with allowance for risk. Because holders of those fights can usually hold the resources in stock or bring them to market immediately, the current rent or stumpage value tends to reflect the present value of expected future net income that can be derived from them. This principle is readily extended to other resources: agricultural land can be valued directly on the basis of its current market worth, or indirectly as the present value of the future stream of net income, or annual rent, that can be derived from it. The value of subsurface irrigation water deposits can be estimated from market transactions in "water fights," or by comparing the value of agricultural land overlaying a usable, known aquifer with that of otherwise equivalent land without subsurface water. Alternatively, it can be estimated as the present value of future rents, calculated as the difference between the costs (per cubic meter) of supplying the water for irrigation and the incremental net farm income attributable to the use of the water for irrigation.

In order for adjustments to national income accounts for natural resource stock changes to attain broad acceptance, a credible standard technique for valuing natural resources must be adopted that can be applied to a variety of resources by statisticians in different countries. That

method must be as free as possible from speculative estimates (about future market prices, for example), and must depend on underlying data that is reasonably available to statistical agencies.

The three principal methods for estimating the value of natural resource stocks are: 1) the present value of future net revenues; 2) the transaction value of market purchases and sales of the resource in situ; and 3) the net price, or unit rent, of the resource multiplied by the relevant quantity of the reserve. The present value method requires that future prices, operating costs, production levels, and interest rates be forecast over the life of a given field after its discovery. The present value of the stream of net revenue is then calculated, net revenue representing the total revenue from the resource less all extraction costs. The United Nations Statistical Office has recommended use of the present value method when market values for transactions in resource stock are not available.

The net price method applies the prevailing average net price per unit of the resource (current revenues less current production costs) to the physical quantities of proved reserves and changes in the levels of proved reserves. While the net price method requires only current data on prices and costs, it will be equivalent to the other two methods if output prices behave in accordance with long-run competitive market equilibrium. The assumption here is derived from the theory of optimal depletion of exhaustible resources, that resource owners will tend to arbitrage returns from holding the stock into future periods with returns from bringing it immediately to market, adjusting current and future supplies until price changes equate those returns.

WHAT CAN POLICYMAKERS LEARN FROM RESOURCE ACCOUNTING?

Macroeconomic Policy and Structural Adjustment

National accounts that incorporate natural resource accounting provide a more adequate means of evaluating an economy's performance and progress toward sustainable development. World Resources Institute has collaborated on a pioneering report using Indonesia as a case study. Over the past 20 years, Indonesia has drawn heavily on its considerable natural resource endowment to finance development expenditures. Revenues from production of oil, gas, hard minerals, timber, and forest products have offset a large share of government development and routine expenditures. Primary production contributes more than 43 percent of gross domestic product, 83 percent of exports, and 55 percent of total employment. Indonesia's economic performance over this period is generally judged to have been successful: per capital GDP growth averaging 4.6 percent per year from 1965 to 1986 has been exceeded by only a handful of low and middle-income countries and is far above the average for those groups. Gross domestic investment rose from 8 percent of GDP in 1965, at the end of the Sukarno era, to 26 percent of GDP (also well above average) in 1986, despite low oil prices and a difficult debt situation.

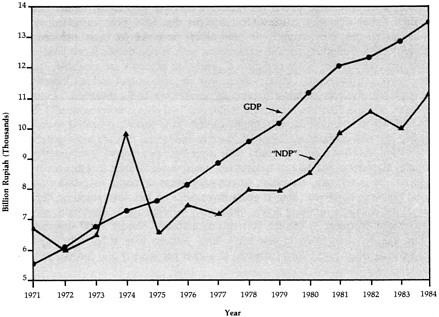

Estimates derived from the Indonesian country case study illustrate how much this evaluation is affected by "keeping score" more correctly. Figure 2-1 compares the growth of gross domestic product at constant prices with the growth of "net" domestic product, derived by subtracting estimates of natural resource depreciation for only three sectors: petroleum,

timber, and soils. It is clear that conventionally measured gross domestic product substantially overstates the growth of net income, after accounting for consumption of natural resource capital. In fact, while GDP increased at an average annual rate of 7.7 percent from 1970 to 1984, the estimate of ''net" national product rose by only 3.9 percent per year. In other words, one-half of recorded growth was generated, not by sustainable productivity increase, but by drawing down natural resource assets.

The overstatement of income growth is actually considerably more than these depreciation estimates indicate, since only three natural resources are covered: petroleum, timber, and soils on Java and Bali. Other important exhaustible resources that have been exploited over the period, such as natural gas, coal, copper, tin, and nickel have not yet been included in the accounts. The depreciation of other renewable resources, such as non-timber forest products and fisheries is also unaccounted for. When complete depreciation accounts are available, they will inevitably show a greater divergence between the growth in gross output and net income.

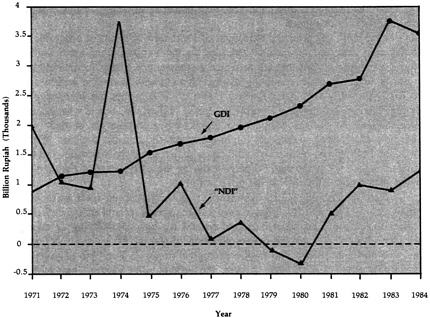

Other important macroeconomic estimates are even more badly distorted. Figure 2-2 compares estimates of gross domestic investment (GDI) and "net domestic investment" ("NDI"), the latter reflecting depreciation of natural resource capital. This statistic is central to economic planning in resource based economies. Countries, such as Indonesia, that are heavily dependent on exhaustible natural resources must diversify their asset base to preserve a sustainable long-term growth path. Extraction and sale of natural resources, must finance investments in other productive capital. It is relevant, therefore, to compare gross domestic investment with the value of natural resource depletion. Should gross investment be less than resource depletion, then, on balance, the country is drawing down, rather than building up, its asset base, and using its natural resource endowment to finance current consumption. Should "net" investment be positive but less than required to equip new labor force entrants with at least the capital per worker of the existing labor force, then increases in output per worker and income per capita are unlikely.

In fact, the results from the Indonesian case study show that the adjustment for natural resource asset changes is large in many years relative to gross domestic investment. In a few years, the adjustment is positive, due to additions to petroleum reserves. In most years during the period, however, the depletion adjustment offsets a good part of gross capital formation. A fuller accounting of natural resource depletion might conclude that in some years, depletion exceeded gross investment, implying that natural resources were being depleted to finance current consumption expenditures.

Such an evaluation should flash an unmistakable warning signal to economic policymakers that they were on an unsustainable course. An economic accounting system that does not generate and highlight such evaluations is deficient as a tool for analysis and policy in resource-based economies and should be amended.

Countries throughout Africa, Latin America, and Eastern Europe and north Asia are undergoing dramatic economic transformations, undoing decades of state intervention and market distortion. The international agencies of the World Bank and the International Monetary Fund (IMF) are being called upon to support structural adjustment and stabilization programs with policy advice and capital flows.

How economic reforms should be designed to ensure a successful transition to sustainable economic progress is a matter of urgent concern. In all these regions now undergoing structural

reforms, environmental degradation has been as obvious a symptom of the failure of the previous policies as economic collapse. Uncontrolled pollution, excessive environmental hazards, and overexploitation of natural resources have accompanied the decline of living standards. New economic policy packages must address and reverse ecological as well as economic deterioration.

In many developing countries the national balance sheet has deteriorated more from depreciation of natural resources than from foreign borrowing. In the Philippines, for example, depreciation in just three sectors—forests, soils, and coastal fisheries—averaged 4.5 percent of GDP per year in the dozen years leading up to the debt crisis, while foreign borrowing averaged only 4 percent of GDP. Unlike the highly publicized debt problem, however, resource depletion went unmeasured and largely unnoticed.

According to the IMF, the principal objectives of short-term adjustment programs are to reduce the internal and external imbalances that lead to the unsustainable accumulation of domestic and foreign liabilities. But the rate at which a country can safely accumulate debt is related to the rate at which it is accumulating assets. If both should double within a given period, the process is probably not unsustainable. However, if liabilities are increasing while assets are declining, there is undoubtedly a problem. In the Philippines, this is what occurred.

Moreover, adjustment polices designed to reduce the accumulation of debt without consideration of their environmental impacts might inadvertently increase the loss of natural resource assets. In the Philippines, restrictive stabilization policies sharply increased poverty and unemployment. Real wages fell more than 30 percent during the early years of the debt crisis, leaving 58 percent of the population below the poverty line.

Poverty "pushed" households out of overcrowded, poverty-stricken rural areas. Instead of facing unemployment in the cities, the prospects of gaining access to land sharply accelerated rural-to-rural migration into upland watersheds and coastal regions, intensifying deforestation and erosion of upland watersheds and the overexploitation of coastal fisheries and mangroves. Succeeding waves of migrants spilled into fragile ecological areas—2.5 million of them in the first half of the 1980s alone. With each harvest, the eroded soils yielded less, and more migrants competed for land. Poverty drove agricultural workers from crowded lowland rice farms, but poverty also awaited them in the cities and the fragile uplands.

To be successful, stabilization programs should be designed to stabilize both sides of the balance sheet—reducing the decumulation of assets as well as the accumulation of debts. Otherwise, adjustment programs will not lead to sustainable development. The IMF, the World Bank, and other development agencies should base their macroeconomic analysis on an accounting system that treats natural resources as the important assets that they are, and extend their analyses to examine the potential environmental effects of adjustment programs.

Sectoral Policy

Natural resource accounting is also extremely useful in formulating and evaluating sectoral economic policy. For example, the resource accounts drawn up for the Indonesian timber sector estimated the stumpage value or resource rents available from harvest of that

country's natural tropical hardwood forests. As the following table indicates, there have been large resource rents generated by exploitation of primary forest.

Those forests are in very large part within the public domain, as national forests. The government of Indonesia licenses concessionaires to extract timber under long-term contract. Many of the concession-holders are controlled by non-Indonesian interests, in partnerships with local elites. The government captures some of the resource rents from concessionaires through a variety of license fees, property taxes, royalties, and fees. In theory, since the calculation of stumpage values makes allowance for a normal return on capital invested in the logging operation, the government of Indonesia could have captured a large fraction of the available rents.

It was a small step from the estimation of sectoral accounts to the question whether the government was actually collecting as much of the value from forest exploitation as it might. A leading Indonesian environmental organization, in cooperation with academic economists, undertook to examine the issue of rent capture, and found that in recent years the government had succeeded in capturing only 10 to 15 percent of resource rents, losing potential revenues of $2 billion annually—equivalent to 40 percent of annual ODA.

This study led to reexamination of the supply of logs at prices well below international levels to domestic mills, to the lag in forest taxes behind inflation, and to weaknesses in the supervision of timber concessions. These issues axe important not only for fiscal reasons, but also to promote more efficient and sustainable utilization of Indonesia's rich forests.

TABLE 2-1 Forest Resource Accounts-Indonesia (1970-76)

|

PHYSICAL UNITS (million cu. meter) |

|||||||

|

|

1970 |

1971 |

1972 |

1973 |

1974 |

1975 |

1976 |

|

OPENING STOCK(1) |

21713 |

21651 |

21587 |

21522 |

21450 |

21383 |

21325 |

|

ADDITIONS: |

|||||||

|

Growth(2) |

51.9 |

51.9 |

51.9 |

51.9 |

51.9 |

51.9 |

51.9 |

|

Reforestation(3) |

1.3 |

3.4 |

5.5 |

7.6 |

9.7 |

11.8 |

13.8 |

|

REDUCTIONS: |

|||||||

|

Harvesting(4) |

10.0 |

13.8 |

16.9 |

26.3 |

23.3 |

16.3 |

21.4 |

|

Deforestation(5) |

99.0 |

99.0 |

99.0 |

99.0 |

99.0 |

99.0 |

99.0 |

|

Degradation(6) |

6.6 |

6.6 |

6.6 |

6.6 |

6.6 |

6.6 |

6.6 |

|

|

---- |

---- |

---- |

---- |

---- |

---- |

---- |

|

NET CHANGE |

62.4 |

64.1 |

65.1 |

72.4 |

67.3 |

58.2 |

61.3 |

|

(ROUNDED) |

(62) |

(64) |

(65) |

(72) |

(67) |

(58) |

(61) |

|

|

---- |

---- |

---- |

---- |

---- |

---- |

---- |

|

CLOSING STOCK(1) |

21651 |

21587 |

21522 |

21450 |

21383 |

21325 |

21264 |

|

UNIT VALUES ($U.S. per cu. meter) |

|||||||

|

FOB Export Price |

10.90 |

15.10 |

17.10 |

29.30 |

41.60 |

26.40 |

44.70 |

|

Harvesting Costs |

4.90 |

6.80 |

7.90 |

13.18 |

18.72 |

11.88 |

20.12 |

|

|

---- |

---- |

---- |

---- |

---- |

---- |

---- |

|

'Primary' Rent(7) |

6.00 |

8.30 |

9.20 |

16.12 |

22.88 |

14.52 |

24.58 |

|

'Secondary' Rent(7) |

3.78 |

5.23 |

5.80 |

10.16 |

14.41 |

9.15 |

15.48 |

|

MONETARY ACCOUNTS ($ million) |

|||||||

|

|

1970 |

1971 |

1972 |

1973 |

1974 |

1975 |

1976 |

|

OPENING STOCK |

---- |

105224 |

145064 |

160339 |

280137 |

396227 |

250782 |

|

ADDITIONS: |

|||||||

|

Growth |

196 |

271 |

301 |

527 |

748 |

475 |

803 |

|

Reforestation |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

|

REDUCTIONS: |

|||||||

|

Harvesting |

60 |

115 |

155 |

424 |

533 |

237 |

526 |

|

Deforestation & Degradation |

399 |

552 |

612 |

1073 |

1522 |

966 |

1635 |

|

|

---- |

---- |

---- |

---- |

---- |

---- |

---- |

|

NET CHANGE |

-263 |

-396 |

-466 |

-970 |

-1307 |

-728 |

-1358 |

|

REVALUATION: |

|||||||

|

Opening Stock |

---- |

32620 |

12764 |

97798 |

95039 |

-117258 |

140777 |

|

|

---- |

---- |

---- |

---- |

---- |

---- |

|

|

CLOSING STOCK |

105525 |

145495 |

160823 |

281077 |

397468 |

251464 |

424581 |

|

PHYSICAL UNITS (million cu. meter) |

||||||

|

|

1977 |

1978 |

1979 |

1980 |

1981 |

1982 |

|

OPENING STOCK(1) |

21264 |

21204 |

21144 |

21085 |

21028 |

20973 |

|

ADDITIONS: |

||||||

|

Growth(2) |

51.9 |

51.9 |

51.9 |

51.9 |

51.9 |

51.9 |

|

Reforestation(3) |

15.9 |

18.0 |

20.1 |

22.1 |

24.2 |

26.3 |

|

REDUCTIONS: |

||||||

|

Harvesting(4) |

22.2 |

24.2 |

25.3 |

25.2 |

16.0 |

13.4 |

|

Deforestation(5) |

99.0 |

99.0 |

99.0 |

99.0 |

108.0 |

108.0 |

|

Degradation(6) |

6.6 |

6.6 |

6.6 |

6.6 |

6.6 |

6.6 |

|

|

---- |

---- |

---- |

---- |

---- |

---- |

|

NET CHANGE |

60.0 |

59.9 |

58.9 |

56.8 |

54.5 |

49.8 |

|

(ROUNDED) |

(60) |

(60) |

(59) |

(57) |

(55) |

(50) |

|

|

---- |

---- |

---- |

---- |

---- |

---- |

|

CLOSING STOCK(1) |

21204 |

21144 |

21085 |

210288 |

20973 |

20923 |

|

UNIT VALUES ($U.S. per cu. meter) |

||||||

|

FOB Export Price |

47.50 |

46.70 |

85.21 |

106.93 |

95.84 |

100.59 |

|

Harvesting Costs |

21.38 |

21.05 |

29.84 |

34.24 |

37.93 |

41.00 |

|

|

---- |

---- |

---- |

---- |

---- |

---- |

|

'Primary' Rent(7) |

26.12 |

25.65 |

55.37 |

72.69 |

57.91 |

59.59 |

|

'Secondary' Rent(7) |

16.46 |

16.16 |

34.33 |

45.07 |

35.90 |

36.95 |

|

MONETARY ACCOUNTS ($ million) |

||||||

|

|

1977 |

1978 |

1979 |

1980 |

1981 |

1982 |

|

OPENING STOCK |

423362 |

448617 |

439298 |

945662 |

1238129 |

983843 |

|

ADDITIONS: |

||||||

|

Growth |

854 |

839 |

1782 |

2339 |

1863 |

1918 |

|

Reforestation |

0 |

0 |

0 |

0 |

0 |

0 |

|

REDUCTIONS: |

||||||

|

Harvesting |

580 |

621 |

1401 |

1832 |

927 |

799 |

|

Deforestation & Degradation |

1738 |

1706 |

3625 |

4759 |

4114 |

4234 |

|

|

---- |

---- |

---- |

---- |

---- |

---- |

|

NET CHANGE |

-1464 |

-1149 |

-3244 |

-4252 |

-3178 |

-3115 |

|

REVALUATION: |

||||||

|

OPENING STOCK |

26525 |

-8072 |

621808 |

296719 |

-251107 |

29225 |

|

CLOSING STOCK |

448617 |

439298 |

945662 |

1238129 |

983843 |

1009953 |

|

PHYSICAL UNITS (million cu. meter) |

||

|

|

1983 |

1984 |

|

OPENING STOCK(1) |

20923 |

20875 |

|

ADDITIONS: |

||

|

Growth(2) |

51.9 |

51.9 |

|

Reforestation(3) |

29.6 |

35.3 |

|

REDUCTIONS: |

||

|

Harvesting(4) |

15.2 |

16.0 |

|

Deforestation(5) |

108.0 |

108.0 |

|

Degradation(6) |

6.6 |

6.6 |

|

|

---- |

---- |

|

NET CHANGE |

48.3 |

43.4 |

|

(ROUNDED) |

(48) |

(43) |

|

|

---- |

---- |

|

CLOSING STOCK(1) |

20875 |

20832 |

|

UNIT VALUES .($U.S. per cu. meter) |

||

|

FOB Export Price |

78.75 |

93.15 |

|

Harvesting Costs |

43.31 |

51.23 |

|

|

---- |

---- |

|

'Primary' Rent(7) |

35.44 |

41.92 |

|

'Secondary' Rent(7) |

22.33 |

26.41 |

|

MONETARY ACCOUNTS ($ million) |

||

|

|

1983 |

1984 |

|

OPENING STOCK |

1009953 |

602974 |

|

ADDITIONS: |

||

|

Growth |

1159 |

1371 |

|

Reforestation |

0 |

0 |

|

REDUCTIONS: |

||

|

Harvesting |

539 |

671 |

|

Deforestation & Degradation |

2559 |

3027 |

|

|

---- |

---- |

|

NET CHANGE |

-1939 |

-2327 |

|

REVALUATION: |

||

|

OPENING STOCK |

-408918 |

106424 |

|

|

---- |

---- |

|

CLOSING STOCK |

602974 |

711725 |