3

The Feasibility of Incorporating Environmental and Natural Resource Availability into the National Accounts

Raymond Prince

Congressional Budget Office Washington, D.C.

National income accounting is among the most important policymaking tools to appear in the last fifty years. The accounts contribute to policymaking by taking detailed economic data and computing aggregate indicators such as gross domestic product (GDP). Aggregate measurements, such as the percentage of GDP spent on health care, often alert decisionmakers of the need for new policy initiatives. Researchers can also use the detailed data to analyze policy alternatives.

This information supports the three basic functions of the national accounts which are (a) to provide an economic interpretation of changes in the nation's assets and national wealth, (b) to provide measures of income based on the actual or imputed market value of goods and services, and (c) to measure financial and factor input flows in the economy.

DEFICIENCIES IN THE TREATMENT OF NATURAL RESOURCES AND THE ENVIRONMENT

Demands to add more information on natural resources and the environment reflect concerns that the ability of the accounts to perform their basic functions is inhibited by a deficient treatment of natural resources and the environment. The current accounts do not, for example, record changes in environmental quality and most natural resource reserves. The nation could severely degrade or vastly improve the environmental quality of its land, air, and water; nearly exhaust or greatly add to its mineral reserves, forests, fisheries, and soil fertility; and suffer—or not experience—permanent losses of biodiversity through the extinction of flora and fauna with little or no discernable effect on aggregate measures of national income or wealth. Thus, aggregate measures from the accounts may fail to alert decisionmakers of problems with the management of these national assets.

The current accounts also ignore or mislabel many of the costs and benefits associated with natural resources and the environment. They treat the costs of reducing the adverse effects of natural resource depletion and environmental degradation as ordinary investment and

consumption expenditures. Damages caused by pollution affect estimates of national income only to the extent that they influence productivity and even those effects are not separately identified in the accounts. Waste disposal services provided by air, land, and water in absorbing pollution are assigned a zero value because no one charges for them. The benefits of maintaining natural resources and a clean environment, such as preservation of biodiversity and enhanced recreation opportunities, are ignored for the same reason. These acts of omission and commission make it difficult for analysts to trace the linkages between environmental and natural resource policies and employment, trade balances and growth in GDP.

A comprehensive amending of the accounts to correct for this deficient treatment would require three kinds of revisions: (1) expanding the asset boundary to record changes in environmental quality and natural resource assets; (2) expanding the production boundary to include services of natural resources and the environment that are not counted in measures of national income such as GDP; and (3) reorganizing the production boundary to more clearly identify the input of environmental factor service flows and the costs of reducing pollution damages counted in GDP.

The data needed to make these revisions to the accounts could provide information that would be potentially useful in many policy debates. Some of the more important issues are the effect of environmental protection on economic growth, the distributional impacts of environmental and natural resource policies, and the linkages between trade and environmental and resource policies. In addition, compiling a set of more integrated information on natural resources and the environment could yield new insights into the workings of the economy and represent an important step towards a goal of producing a measure of national income compatible with the concept of sustainable income.

ASSET AND PRODUCTION BOUNDARIES UNDERLYING THE NATIONAL ACCOUNTS

The National Income and Product Accounts measure the flow of products and income in the U.S. economy. The product side of the national accounts measures the flow of goods and services currently produced in the economy. The income side of the accounts measures the income earned by factors (inputs) contributing to the production of these outputs. The two sides of the accounts represent two different measures of the same continuous flow.

The economic model underlying the accounts assumes that the production of any good or service can be linked to the flow of services provided by capital assets. That is, the goods and services sold in the market reflect the capital services of the plant and equipment used in their manufacture. Table 3-1 lists the major types of fixed capital and examples of service flows from that capital. The two general types of capital stock are reproducible capital and natural capital. Reproducible capital is subdivided into privately-owned and publicly-owned tangible capital and human capital. Natural capital is divided between the environment and natural resource reserves.

TABLE 3-1 Examples of Major Service Flows from Various Types of Capital and An Interpretation of Their Current Treatment in the National Accounts

|

Type of Capital |

Category of Service Flow |

||||

|

|

|

|

Marketed^ |

Nonmarketed |

|

|

|

|

|

Now in GDP |

Now in GDP |

Not now in GDP |

|

Reproducible capital |

A. Tangible, privately-owned |

|

1 Factor services of business-owned plant and equipment to industry and commerce |

7 Factor services of owner- occupied housing |

13 Final services of business- owned capital |

|

|

B. Tangible, publicly-owned |

|

2 Factor services paid for through user fees |

8 Nonpecuniary factor services of infrastructure to industry and commerce |

14 Final services of infrastructure to households |

|

|

C. Human |

|

3 Factor services of labor paid for by wages and salaries |

9 Nonpecuniary volunteer services |

15 Final services (benefits) of education |

|

Natural capital |

D. Environmental |

|

4 marketable permits for use of the waste disposal services of the environment |

10 Waste disposal and other services to industry and commerce of clean air, land and water |

16 Final services of the environment (effects on health, aesthetics) |

|

|

E. Renewable natural resource |

|

5 Food, lumber, water, and recreation paid for by user fees |

11* |

17 Other recreation services, biodiversity, nonuse benefits |

|

|

E Nonrenewable natural resource |

|

6 Energy, minerals, water, and recreation paid for by user fees |

12* |

18 Nonpecuniary final services of nonrenewable resources (recreation services, nonuse benefits) |

|

SOURCE: Congressional Budget Office * Major service flows not identifiable ^ Underground market activities are not included in GDP and are not represented |

|||||

Factor Services

The flows of factor services provided by various capital stock for producing final products are shown in cells 1 through 12. The factor services provided by privately owned tangible reproducible capital to businesses appear in cell 1. The factor services from this capital to households are shown in cell 7. The services to households are listed as nonmarketed because homeowners do not really pay themselves rent. The value of these services do not represent actual market exchanges but rather are imputed.

Much publicly owned reproducible capital stock adds value to GDP; the factor services from this type of capital appear in cell 2 (for marketed services) and cell 8 (for nonmarketed). The amount of human capital contributing to GDP is a function of the total number of workers plus their skills and knowledge. The services of human capital, labor services, is represented in cell 3 (for marketed services) and cell 9 (for nonmarketed).

Natural capital is made up of air (atmosphere), water (hydrosphere), and land (lithosphere) which provide both environmental and natural resource factor services. Natural capital provides marketed environmental waste disposal services (cell 4) and nonmarketed environmental waste disposal services (cell 10). The atmosphere absorbs greenhouse gases (carbon dioxide, methane, hyrdoflourocarbons, etc.), ozone depleting substances including chloroflourocarbons (CFCs), emissions of particulate matter, nitrous oxides (NOx), sulphur oxides (SOx), and volatile organic compounds (VOCs) contributing to atmospheric ozone. Water resources (the hydrosphere) absorb such pollutants as heavy metals, chlorides, plastics, acid rain, pesticides, organic wastes, and chemical fertilizers. Paper, glass, metals, rubber products, plastics, pesticides, and chemical fertilizers are also deposited on land (the lithosphere). These waste disposal services are implicit in the production boundary and, therefore, affect GDP.

Natural resources are divided into renewable and nonrenewable stocks. Renewable resources include agricultural lands, recreational areas, forests, lakes, streams, grasslands, wetlands, fisheries, and wildlife. These resources provide marketed factor services (cell 5) which serve as inputs into the production of final goods and services such as food, wood products, and drinking water and recreation.

Nonrenewable natural resource stocks include reserves of mineral fuels (petroleum, natural gas, coal and uranium), nonfuel minerals (e.g., lead, copper, gold) and groundwater. Nonrenewable resources provide inputs (cell 6) into the production of energy, metal products, and final products such as drinking water, and recreation.

Final Services

Assets can also generate service flows which go to households (final users) rather than to business as primary inputs to production. These service flows are not currently recorded in the accounts; including them would require expanding the definition of GDP. The services of these assets are represented in the production boundary of Table 3-1 and labeled nonmarketed and not now included in GDP. The types of final services of these capital stocks are rarely bought and sold in organized markets because of the difficulty of excluding nonpayers.

The Golden Gate Bridge and Empire State Building, for example, contribute to the ambience of San Francisco and New York in a way that differs from their service as an input into the production of other goods and services. These services appear in cells 13 and 14. The final services of education, such as being a more informed citizen and having a heightened appreciation of historical sights, are nonpecuniary; they appear in cell 15.

Natural resources and the environment—the Grand Canyon and clean water—derive much of their value to society from the aesthetic, free recreation, and health benefits they provide. The final services to households of people who travel to beaches and mountains to enjoy the clean air and water as well as the unspoiled land (cell 16) is another example. Many natural resources also provide nonmarketed final services known as nonuse benefits (cells 17 and 18). Evidence that these services are considered valuable to final users is indicated by the willingness of individuals, who may never actually see a blue whale, to spend money to protect them.

Current Asset and Production Boundaries of U.S. Accounts

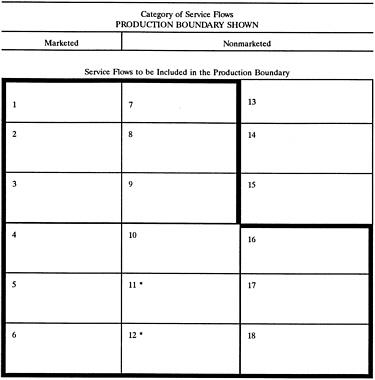

The asset and production ''boundaries'' define the set of goods and services that are included in the national accounts. The asset boundary contains real assets which include fixed capital. An asset must be included in the asset boundary if it is to be assigned a value in the balance sheets and must be designated as fixed capital if its depreciation is to be subtracted from GDP. The production boundary delineates the set of goods and services which are treated as either intermediate or final products. Only final products in the production boundary are counted toward GDP.

The contents of the current production boundary are shown in Table 3-2. Presently, GDP includes all final goods and services involving an exchange of money (a market transaction) with the exception of certain market activities in the underground economy.1 This is equivalent to the income earned from all the factor services of capital used in the production of these final goods and services. Marketed service flows are represented in cells 1-6. There are also some nonmarketed flows not involved in any market transaction that are included in GDP. The biggest single item currently recorded in the accounts in this category is the services of owner-occupied housing (cell 7). In addition, there are the nonmarketed factor services of publicly-owned reproducible capital (cell 8); the factor services—human capital—of volunteers (cell 9); environmental waste disposal factor services (cell 10); and the factor services from natural resources (cells 11 and 12).

None of the services in cells 8 through 12 appear, however, as distinct entries in the accounts because there are no direct payments to these factors for their housing). Other forms

services. Moreover, no imputed values have been assigned to them as has been done for owner-occupied housing. But the availability of such services does impact GDP through effects on productivity.2 For this reason, they are included in this representation of the production boundary. Finally, the final services of capital (cells 13-18) are not included in the production boundary and, therefore, are not counted in GDP.

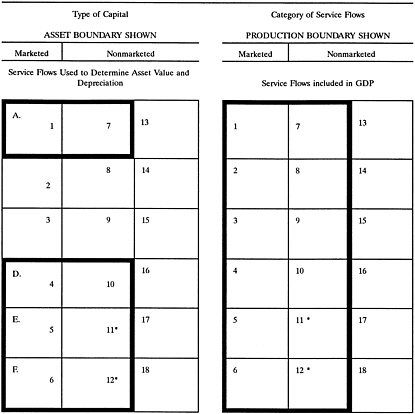

The current asset boundary, demarcated by the thick-lined box on the left in Table 3-2, shows that the accounts only recognize privately owned tangible, reproducible capital (including of capital—publicly owned reproducible, human, and natural capital—whose services appear in cells 2 through 6, 8 through 12, and 14 through 18—are not included in the asset boundary. This means that an asymmetry exists between the current asset and production boundaries since the current production boundary does implicitly or explicitly count the factor services of publicly owned capital, human capital and natural capital. This asymmetry means that the balance sheets do not record investment or depreciation for some kinds of capital stock whose factor services are counted in GDP.

ADDRESSING THE DEFICIENCIES IN THE TREATMENT OF NATURAL RESOURCES AND THE ENVIRONMENT

Three kinds of revisions to the accounts are possible: (1) expanding the asset boundary to record changes in environmental quality and natural resource assets (cells 4-6 and 10-12); (2) expanding the production boundary to include the final services of natural resources and the environment, which are not counted in measures of national income such as GDP (cells 16-18); and (3) reorganizing the production boundary to more clearly identify the input of environmental factor service flows (cells 4 and 10) and the costs of reducing pollution damages counted in GDP.

Expanding the Asset Boundary to Record Changes in Natural Resources and the Environment

Expanding the asset boundary to record changes in natural resources and the environment implies that values for depletion and degradation would be computed for these natural capital assets along with depreciation for tangible reproducible capital. For conventional GDP, the asset boundary would have to be expanded to account for natural capital generating services flows represented in cells 4-6 and 10-12 as shown in Table 3-3. That is, values for depletion and degradation could be estimated for natural resource assets such as forests, mineral reserves, and the quality and quantity of agricultural lands. Values for degradation would also be calculated for the changes in currently available environmental waste disposal services. Available waste

disposal services depend on limits set by regulation. Of course, changes in the production boundary would imply an expanded set of services for valuing capital assets.

Subtracting depreciation for the expanded set of assets from GDP could be used to produce what might be termed an "environmentally adjusted NDP." That is, NDP would be adjusted for depreciation of tangible capital, depletion of natural resources, and degradation of environmental assets. The balance sheets are the component of the accounts where most of the changes implied by redefining the asset boundary would occur. It is there that changes in assets—whether from use, capital gains and losses, or investment—are recorded.

Expanding the Production Boundary to Include More Services of Natural Resources and the Environment in Measures of National Income

Expanding the production boundary to include more services of natural resources and the environment would mean that expanded definitions of national income could now be calculated. A measure of a "green" GDP, for example, would count the final nonmarketed services of natural resources and the environment. Therefore, the production boundary would have to be expanded to include cells 16-18 as shown in Table 3-4. That is, the value of nonhealth-related services—recreation, biodiversity, aesthetic, and nonuse benefits—as well as pollution damages (treated as negatively valued health-related services) would be included in national income.

Two implications of this kind of change to the accounts deserve mention. One is that the flows in cells 16-18 are among the most difficult nonmarket services to value. Because they are not inputs to the production of marketed goods and services, the choice of techniques for imputing a price for the assets generating these services is much more limited. Second, many of the changes implied by expanding the production boundary would show up in the NIPA component of the accounts where imputed expenditures and rent are recorded. As with other fixes, however, other components of the accounts would be affected to some degree. For example, there may be some depreciation from use of the service flows to households. To be internally consistent, the asset boundary could be extended to measure depreciation (due to use) of assets providing these services.

Reorganizing Items Included in the Production Boundary to More Clearly Identify Environmental Services and the Costs of Reducing the Risks of Pollution

Reorganizing items included in the production boundary to more clearly identify service flows from the environment would recognize the flow of waste disposal services from the environment to businesses as an input into production. As is the case for other kinds of factor services in production, there is an associated return (income). Since waste disposal services are not marketed, a price would have to be imputed based on the productivity of this factor (similar to identifying wages for the services of labor—as flows of human capital). This information could be estimated by sector, recorded in the Input-Output (I-O) tables, and used in analysis of

the impacts of environmental policies. For example, the economic impact on production of an environmental policy to change allowable emission levels, could then be traced on an industry-by-industry level through the I-O tables.

Identifying waste services is described as a reorganization rather than a redefinition of the production boundary since this kind of revision would not have to result in a change in the goods and services included in GDP. It would involve, instead, assigning some of the value added now recorded as profits, wages, rents, etc. to imputed factor payments for the environment. Reorganizing the production boundary would, therefore, result in changes to the I-O table more than to other components of the accounts.

Reorganizing items included in the current production boundary to more clearly identify the costs of reducing the risks of health damages from pollution would mean that some of the expenditures now listed as investment and consumption would be listed as defensive expenditures. These expenditures would include expenses for ameliorating environmentally-related health problems and for abatement equipment. Reclassifying these costs as a part of reorganizing the accounts would also help to identify the benefits and costs of changing emission levels at the industry level. It is called a reorganization because it would not have to result in a change in the measure of national income.3

An important problem with carrying out this reorganization will be handling the joint service output of many items. For example, air conditioners may reduce the affects of air pollution on sufferers of respiratory ailments, but they are not purchased for the medicinal purposes alone. The percentage of the total cost of such items to assign to defensive expenditures will have to be determined.

CONCLUSIONS

Incorporating more information on natural resources and the environment into the accounts ("green accounting") will require much conceptual work and data gathering. The principal problems with incorporating more information into the accounts are identifying the most appropriate way of measuring physical changes in environmental quality and natural

resource reserves and identifying reliable and consistent methods of pricing the nonmarket services of these assets.

Estimating changes in the reserves of economically exploitable resources is difficult when market conditions are changing. Measuring net changes in biological resources is difficult because of uncertainties about population growth rates. And aggregate measures of environmental quality mask problems associated with "hot spots" which are well below minimum standards.

Valuing natural resource depletion or environmental degradation depends heavily on techniques to impute prices because many of the services of natural resources and the environment are not sold in markets. The lack of organized markets is especially a problem in valuing service flows associated with the health effects of changes in environmental quality.

If a decision is made to add more information on natural resources and the environment into the accounts, the most immediate concern will be how to proceed with the three types of revisions. The United Nations (UN) and Bureau of Economic Analysis (BEA) have decided to maintain satellite accounts to record measures of the value of natural capital, its depletion, and flow of services, while measurement issues are being resolved. These measures could later be integrated into the main components of the accounts as problems of measurement and data axe resolved.

In addition, initial efforts by the UN and BEA, which are meant to improve their understanding of how best to incorporate natural resources and the environment into the accounts, have relied to a large extent on market data. These initial efforts concentrate on two types of revisions to the accounts: determining the monetary value of environmental asset degradation and resource asset depletion and identifying pollution abatement and control expenditures designed to reduce pollution damages.

The focus of these initial efforts is logical since it is possible to estimate the costs of reducing pollution damages largely from data already collected in compiling the national accounts. Likewise it is possible to estimate environmental degradation and natural resource depletion largely from market data on the costs of maintaining environmental quality and revenues from goods and services from natural resources. In contrast, expanding the production boundary or valuing environmental waste disposal services requires much greater reliance on imputed prices.

Imputed prices are now used in computing aggregate measures such as GDP but are limited to items, such as the value of services of owner-occupied housing, for which much relevant market data exist. Revising the accounts beyond current efforts implies, however, a significantly expanded reliance on imputed prices for valuing services for which there are much less relevant market data. Nevertheless, a gradual process of modifying measures of national economic performance is consistent with our experience since first introducing the national accounts. It is within this context that any effort to incorporate more information on environmental and natural resources into the national accounts should be judged.