5

Transfer Models for "Green Accounting": An Approach to Environmental Policy Analysis for Sustainable Development

Paul P. Craig

Harold Glasser

Civil and Environmental Engineering University of California, Davis

THEME: ARE WE KILLING THE GOLDEN GOOSE?

Efforts to revise national income accounts to incorporate environmental externalities ("green accounting") may help us to better understand how our social, political, and economic actions impact the environment. A primary motivation behind "green accounting" is concern that humankind's activities are creating significant environmental damage which is not captured by conventional accounting techniques. Ascertaining the extent to which humans are consuming nature as contrasted with living upon interest has reached paramount importance. Phrased informally, is our society unknowingly ''killing the golden goose?"

There exists an immense range of views on this question. Optimists argue that technological advances will provide substitutes, and claim that there is no need to worry. Pessimists—"cliffologists"—worry that we are destroying irreplaceable resources and creating adverse side-effects at an accelerating pace; they fear that disaster looms.1

Regardless of perspective, there seems to be agreement that addressing questions of sustainability requires new tools. We argue here that national income accounts, as commonly constituted, are inadequate to capture some of the most important features of the debate over sustainability. We review the most important of these reasons. From this review we conclude that there are severe methodological issues that cannot as yet be resolved. We propose one approach, which we call the "transfer model" methodology. While this technique shows promise, it is still in an early stage of development.

Our transfer model approach, which emphasizes both stocks and flows, is a framework for giving meaning and context to green accounts. It also focuses upon biogeophysical measures

which represent direct indicators of particular aspects of sustainability. Such issues were raised in the major report, World Conservation Strategy (IUCN, 1980, Section 4.1):

Sustainable utilization is somewhat analogous to spending the interest while keeping the capital. A society that insists that all utilization of living resources be sustainable ensures that it will benefit from those resources virtually indefinitely.

According to this view, sustainability requires that certain baseline conditions be guaranteed. Because of difficulties associated with monetization (among others), baseline conditions are best specified in biogeophysical terms that take into account both stocks and flows. For instance, biological terms appear the most informative when discussing issues such as the need of species for habitat, healthy food, clean water, adequate range, a minimum viable population, stress resistance, etc. If these and other baseline conditions cannot be provided, species are likely to go extinct.

Because of ambiguities and uncertainties about what constitutes sustainability and whether or not it is being achieved in particular cases, it is not surprising that discussions of sustainability frequently lead to debate. Questions concerning humankind's relationship to the environment, perception of growth, views on the helpfulness or harmfulness of technology, salience of equity issues (both intragenerational and intergenerational), population stress, species and cultural diversity, and the ability of our present socioeconomic-political systems to effectively address these issues are all relevant to this discussion. These issues help us to explore the preconditions for sustainability. Improved natural capital accounts can help us to explore our current state of affairs and hypothesize about how we got here and what the future might hold. Consensus on the range of diverse issues is not necessary for directing policies in a more sustainable direction.

The economist Herman Daly has provided a useful starting point by observing that:

[f]or the management of renewable resources there are two obvious principles of sustainable development. First that harvest rates should equal [or be lower than] regeneration rates (sustained yield). Second that waste emission rates should equal [or be lower than] the natural assimilative capacities of the ecosystems into which they are emitted. Regenerative and assimilative capacities must be treated as natural capital, and failure to maintain these capacities must be treated as capital consumption, and therefore not sustainable [our interjection] (1990:2).

These two "common sense" principles for the establishment of sustainable policies differ from traditional economic indicators in that they are biogeophysically based. To make such principles operationally useful one must have data on actual stocks and flows. We suggest that when the issue at hand is sustainability, economic valuation techniques are often too decoupled from the biogeophysical world to provide us with the necessary insights. Our approach eliminates the need for developing pseudo-market values for currently nonmarketed goods. The entire issue of assigning monetary values, with its uncertainty, problems of time value, cultural variability, added cost, etc., is effectively side-stepped. Such accounts could serve as biogeochemical satellites to complement the existing monetized national income accounts.

Green accounting cannot focus on renewable resources alone. Complex trade-offs and substitutions may be consistent with sustainability. It is important to recognize that Daly's guidelines are preliminary and not absolute. They are used to illustrate the efficacy of considering a biogeophysically based approach to natural capital accounting.

Daly's notions do not convey that natural capital may be consumed and transformed into other forms that may in turn be sustainable. This may, in fact, be desirable from a development perspective. Harvesting of nonrenewables may, in certain instances, prove to be more "sustainable" than harvesting some resource sustainably. Imagine the case of using a pristine wild river to generate electricity as contrasted with creating solar cells from sand and petrochemicals. Energy from oil may provide a springboard to sustainable photoelectric electricity, while the damming of the river may irreparably destroy ecosystems and native cultures. Static or snapshot analysis is not enough either. A sustainable system should be operated so as to assure resilience against inevitable fluctuations. Determining safe and sustainable harvest levels requires much more information than inventorying natural capital accounts (stock sizes). Careful empirical modeling exercises and field studies are necessary to assess feedbacks, rates of change of stocks, critical cause and effect relationships, hazards, etc.

How to develop these satellite accounts and their associated machinery is far from clear. We believe that the focus on stocks, flows, uncertainties, and their interrelationships that lies at the core of this paper moves in the right direction, but we recognize the difficulty with making direct linkages to existing, monetized national income accounts.

The transfer model approach is designed to explicitly incorporate multiple world views and uncertainty. Accounting systems should reflect a recognition that experts differ, and that in any controversial area there are optimists and pessimists.

For example, the (current) centrist position on the long-term impact of carbon dioxide on climate and thence on agricultural output is optimistic in the sense that potential problems are believed to be addressable at the cost of a few percent of gross national product (GNP). However, some experts are less sanguine. We argue that a successful accounting system should also reflect the views of those (in this example, a minority) whose analysis suggests severe adverse impacts with high social cost.

Discussion at the National Research Council Workshop emphasized the point that all accounting systems necessarily and unavoidably reflect our perception of the world and our perspective on limits. The importance of these "value judgements" (e.g., regarding perspectives of what the future will and should be like; of the roles of technology; of how conceptual frameworks and knowledge bases will change; of how to discount the future; and of equity and the allocation of resources among different groups) becomes amplified when one is dealing with intergenerational issues. For example, the possibility of severe adverse environmental consequences from anthropogenic greenhouse gas emissions has just recently appeared on scientific and political agendas; the implications of these gases for policy has just begun to be seriously discussed.

A successful green accounting framework must be designed so as to make assumptions clear, and to allow a broad band of perspectives to be represented. Our approach, by focusing upon conceptual structures, biogeochemical indicators, and judgements about what is likely to be considered important in the future, directly addresses these considerations. We stress that this is a conceptual paper. As yet there has been only limited work on combining bio

geophysical satellite accounts with transfer models and on the use of uncertainty analysis techniques in environmental accounting. Our goal is to suggest directions, and to illustrate the promise of this approach with some oversimplified schematic examples. The framework that we propose links physically based green accounts with "transfer models" to provide the meaning, context, and insight necessary to assess the health of the ultimate "golden goose"—the global life support system.

STRUCTURE OF THE PAPER

The paper is divided into seven textual sections. It also includes eleven figures and references. The core of the paper is the conceptual. Our goal is not to provide answers (a completed green accounting framework), but to correctly frame the appropriate questions, a critical prerequisite for developing successful green accounts. Because there is much controversy over the need for an approach such as ours, we spend much of the paper presenting the background.

We open with a discussion of the need for conceptual frameworks. What kinds of goals should green accounts attempt to meet. Who are the audiences and users? We next examine limitations on optimization techniques for the long-term. We then explore the reasons why goal-setting is so important in contemplating long-term environmental issues. Next we review several technical approaches to long-term issues, indicating their primary strengths and shortcomings.

We conclude with simplified examples focusing on two specific long-term issues— radioactive waste disposal, and global warming and its possible impact on agriculture. We present illustrative graphs that show how a risk analysis approach generates visual aids that can reflect not only the "centrist" conclusions, but which also allow one to understand what might be expected if alternative, less likely, perspectives turn out to be correct. We urge the reader to examine these figures, and to try to form a view as to whether his/her views on global climate change can be comfortably fitted into the framework. We also ask the reader to consider how this approach might influence their perspective on developing appropriate policy. We suggest that capturing a representative range of perspectives, with their estimated likelihood and conceivable impacts, can help us to become better decisionmakers.

WHY CONCEPTUAL FRAMEWORKS MATTER: LIMITS AND EQUITY

[S]tories generate theories and . . . theories are transformed in the telling, the resultant combinations serving as self-fulfilling prophecies (Apter, 1993).

Environmental accounting, like more traditional national income accounting, cannot exist in a vacuum. Data develops meaning and context by placing it within a conceptual framework that incorporates at least one view of the world. Many issues facing society today qualitatively differ from those of a generation ago. Many types of environmental problems of central importance today were unknown a generation ago. It is no surprise that as new issues emerge,

new accounting and evaluation techniques are needed to reflect society's changing insights and concerns. The motivation for ''green accounting" emanates from the growing concern over resource degradation and depletion.

To be broadly acceptable, an improved accounting system must be able to cope with the enormous diversity of views on the adaptability of mankind and of the global ecosystem. A wide range of views exist on the feasibility, necessity, and desirability of adaption to a changing environment. The "optimist" view was clearly articulated by a Harvard economist.

There is absolutely no reason why, on the grounds of the existence of depletable resources, that we ought to conserve for future generations. . .. It is important to remark on the fact that if they have any luck at all . . . they will be a lot richer than we are. . .. If history is any guide, the costs of the materials and energy that are produced even from depletable resources will be cheaper than they are to us in real terms. . .. There is no reason not to use the marketplace . . . there are no externalities of this type that ought to be brought to bear (Jorgenson, 1981).

While such a perspective does not preclude the development of more detailed green accounts, it certainly suggests that technological innovation makes such detailed accounting unnecessary. Investigation into the existence of impending physical limits is precluded by an hypothesis of their nonexistence. Such a view, however, might argue that improved natural capital accounts are necessary to insure that transition to substitutes occurs with minimal adjustment costs.

A slightly less optimistic view was expressed in the Brundtland Commission's Report:

Humanity has the ability to make development sustainable—to ensure that it meets the needs of the present without compromising the ability of future generations to meet their own needs. The concept of sustainable development does imply limits—not absolute limits but limitations imposed by the present state of technology and social organization on environmental resources and by the ability of the biosphere to absorb the effects of human activities (The World Commission on Environment and Development, 1987:8).

This view posits that sustainability is not a given. It still conveys a strong sense of technological optimism, but it recognizes—albeit grudgingly—the existence of physical limits. While not calling for detailed physical accounts directly, it suggests that more careful accounting will be necessary to insure that we can meet " . . . the needs of the present without compromising the ability of future generations to meet their own needs."

A considerably less optimistic view of limits was put forth in the Report of the World Conservation Strategy.

A society that insists that all utilization of living resources be sustainable ensures that it will benefit from those resources virtually indefinitely. Unfortunately, most utilization of aquatic animals, of the wild plants and animals of the land, of forests and of grazing lands is not sustainable (UCN-UNEP-WWF, 1980: Section 4.1).

This report expresses a clear distinction between the fruits of technological innovation and those of the natural world. Sustainable resource utilization cannot result from technological innovation alone. The report represents a more direct call for improved physical accounts. It suggests that political will, along with much more careful planning and management, are needed to approach sustainability.

Herman Daly extends the discussion of environmental limits to emphasize that natural capital and man-made capital cannot be viewed as directly fungible.

It must be clear to anyone who can see beyond paper-and-pencil operations on a neoclassical production function, that material transformed and tools of transformation are compliments, not substitutes. Do extra sawmills substitute for diminishing forests? Do more refineries substitute for depleted oil wells? Do larger nets substitute for declining fish populations? On the contrary, the productivity of sawmills, refineries, and fishing nets (man-made capital) will decline with the decline in forests, oil deposits, and fish. Natural capital as a provider of raw material and energy is complimentary to manmade capital. Natural capital as absorber of waste products is also complimentary to the man-made capital which generates those wastes (Daly, 1990:3).

Daly's more pessimistic view of the limits of technological innovation can be seen as being in direct contrast to the optimists' view as represented by the Harvard economist, Jorgenson. Daly argues that much more than "luck" is needed to approach sustainability. By focusing upon the complementary nature of natural capital and man-made capital, Daly makes a case for separate, biogeophysically based satellite accounts.

A direct attack of the limits of technological innovation, linking concerns over sustainability directly to ethical issues, was put forth by Rajni Kothari:

In the absence of an ethical imperative, environmentalism has been reduced to a technological fix, and as with all technological fixes, solutions are seen to lie once more in the hands of manager technocrats. Economic growth, propelled by intensive technology and fueled by an excessive exploitation of nature, was once viewed as a major factor in environmental degradation; it has suddenly been given the central role in solving the environmental crisis (Kothari, 1990:27).

Kothari goes on to argue that there are other perspectives of sustainability that are rooted in ethics, not neoclassical economy:

Without such striving, sustainability is an empty term, because the current model of development destroys nature's wealth and hence is nonsustainable. And it is ecologically destructive because it is ethically vacuous—not impelled by basic values, and not anchored in concepts of rights and responsibilities. Thinking and acting ecologically is basically a matter of ethics, of respecting other beings, both human and nonhuman (Kothari, 1990:27-28).

The ethical concerns of Kothari directly link issues of distribution to sustainability. A definition of sustainable development that explicitly incorporates equity concerns has been put forth by a coalition of about 130 nongovernmental, people's and church organizations actively pursuing sustainable development programs in the Philippines. The "Green Forum" (1991) defines sustainable development as:

[a] development course that is not prone to interruption by forces of its own creation which push environmental destruction to intolerable limits, exhaust resources, and exacerbate social inequalities to the point of disruptive political conflict.

The philosopher Arne Naess's views on sustainability call for this broader construction of the equity notion to emphasize sustaining human cultural diversity along with ecological diversity. Naess begins with the positive requirement that sustainable development "assures long-range elimination of abject poverty" (1992:307). He also expresses a symmetrical concern over the destructive aspect of excessive wealth engendered by overconsumption. He points to a distinction between "needs" and ''vital needs." The Brundtland Report made no such distinction. Naess's broader construction of equity views extra parking spaces and huge estates as ''needs" which may be left unsatisfied while maintenance of species diversity is more vital. Naess contends that there can be "ecological sustainability if and only if the richness and diversity of life forms are sustained" (1992:307).

Our purpose in highlighting this wide variety of views on technological innovation and the preconditions of sustainability is to illustrate how one's conception of the world influences the process of framing issues. Environmental science is a social process that entails discourse and debate along with the acquisition and analysis of data (Norgaard, 1992). In this paper we argue that a successful approach to green accounting must represent the range of views expressed above. We feel that three issues in particular should receive careful consideration:

-

How do we define the "health" of ecosystems? And relatedly, how do we assess sustainable yields, develop appropriate conservation practices, support species diversity, etc.?

-

What is the role of technological innovation and what are the limits of substituting human capital for natural capital?

-

How does one deal with "winners" and "losers?" What happens if project proponents are socio-economically better off than the losers (who may also become culturally impoverished), and a proposed project leads to the widening of this gap?

As these questions are applied to different issues, optimists and pessimists are likely to come to very different conclusions as to what factors are relevant. We argue for an approach to analyze these issues that can capture the range of identifiable perspectives, outline "possible" best-and worse-case scenarios, and assess the likelihood of this range of possible scenarios.

GREEN ACCOUNTS

The idea of redefining national accounting systems is itself not new. In fact, conventional national accounting systems were designed to match a theoretical conception of how the economic subsystem works. National Income Accounts are an example. These derive from a conceptual framework developed by John Maynard Keynes. As Anderson states: "Many of the economic statistics collected by governments in the post-war (World War II) period have been designed essentially to produce figures to put into the equations set out in, or which have been derived from the General Theory."

The section on "conceptual frameworks" illustrated how our values and perception of the world influence how we frame issues related to limits and equity. Accounting procedures naturally fare similarly. One expert in international monetary accounting put the matter this way:

From different ways of accounting follow different ways of information distribution which, in turn, has a strong influence on the distribution of value-added between interested parties. Financial accounting thus becomes a tool in the distribution of income between social groups (Colbe, 1981:179).

As new issues emerge, it is not surprising that older structures must be revised or possibly replaced. Green accounting is properly viewed as a reexamination of the ways in which we think about our relationship to and social responsibility towards the environment and future generations. If we believe that we live in a world with fundamental limits then we need tools that allow us to examine and better understand these limits so that we may learn to live within them.

Greenhouse warming and localized air pollution are illustrative. Absent theoretical constructs (the absorption of solar radiation by atmospheric carbon dioxide), atmospheric carbon dioxide concentrations would be of only minor scientific interest. Over three decades ago when Roger Revelle suggested to Charles D. Keeling that he undertake sustained precision measurements on atmospheric CO2, almost no one believed these measurements would be of more than minor academic interest. Today they may be among the most important measurements ever taken by earth scientists!

Conceptual focus depends on perspective as well as knowledge of feedbacks and limits. Smog and visibility reduction are major drivers of regional atmospheric analysis, which emphasize atmospheric particulates, hydrocarbons, nitrous oxides, ozone, and sulfates. Technical analyses of local air pollution show that carbon dioxide and methane play essentially no role. This conclusion is explicit in certain regulatory language, which defines hydrocarbons to exclude methane.2 Such exclusion may be justified when the scale of focus is limited to smog and visibility within an airshed rather than the globe.

When scientists began to investigate the possibility of adverse effects from global warming, methane assumed significance due to the ability of the methane molecule to efficiently absorb infrared radiation. Thus we have one area of atmospheric investigation (localized air pollution) where CO2 and methane play no major role and another (greenhouse warming) where they are of major importance. Similarly, stratospheric ozone is beneficial as a limiter of ultraviolet radiation, and deleterious when in urban airsheds.

Until recently global warming was on few agendas. There was no reason whatsoever to investigate incorporating its implications in national accounts. Today, scientific and technical change has altered that situation irrevocably.

Embarking upon the path of developing green accounts requires a concern over the adequacy of existing accounts to represent situations in which both stock and flow variables are important. Emphasis on flow variables tends to favor products that wear out versus those that last a long time. "Representative" stock variables must first be identified and then accurately measured. Both stock variables (resources and savings) and the effects of consumption upon these stocks (productive capacity, regenerative capacity, and waste assimilative capacity) should be considered. Accurate methods are needed for measuring savings, consumption, degradation and reinvestment (restoration, defensive measures, and general improvement/preservation).

Green accounting efforts seek to measure, in an instrumental and anthropocentrically focused fashion, the "value" and status of the goods and services provided by the environment. They extend the range of consideration to include marketed raw materials (natural capital in the traditional interpretation), unmarketed goods, and waste assimilative services. Their purpose is to support modeling efforts and empirical investigations that may help us determine if we are living on interest or capital. If we are living upon capital, these research efforts may help us to make the transition to a more sustainable path.

An acceptable approach to green accounting should incorporate the perspectives of those who believe that "development" means much more than "economic development." It should, within the limits of feasibility, attempt to represent the full set of goods and services that we obtain from the global ecosystem. It should be designed so as to include factors valued by those advocating a multiplicity of notions of sustainability and a variety of conceptions of the notion of externalities. It must reflect the concerns of those who view themselves as being or becoming worse off along with those who see themselves as advantaged.

THE CASE FOR BIOGEOPHYSICAL GREEN ACCOUNTS

Two main issues arise when considering the development of green accounts. The first consists of data structure and organization: what entities should be measured and in what format (e.g., qualitative or quantitative units, etc.) should the data be represented? The second issue, which is intimately related to the first, concerns how the descriptive content of the data is to be employed and given context. We suggest that the data should be available in a format which makes it accessible to a wide range of analytical and modeling approaches for thinking about the future. We refer to these approaches, which give meaning, context, and insight to the data, as "transfer models." They represent "meta-models" which allow us to explore particular environmental science (economic, climatological, agricultural, air pollution, soil conservation,

etc.) questions under different conditions and scenarios. Transfer models, by informing us about the effects of particular actions (or inactions), can help us to suggest prescriptive response strategies.

In this section we briefly review intergenerationally relevant aspects of several common accounting approaches. We start with existing national income accounts, which provide much of the data used by other techniques. We then look at several econometric approaches designed to internalize environmental externalities. Finally, we explore the intergenerational discount rate controversy, examine multicriteria techniques, and review biogeophysical approaches. This overview is intended to indicate the types of approaches that have been proposed for collecting and utilizing green accounts and to highlight some of their benefits and drawbacks. We conclude that monetized natural capital accounts, while necessarily derivative of disaggregated biogeophysical data, are limited in their ability to reflect physical changes in the environment. The additional step of monetization reduces data certainty, inhibits application with alternative transfer models, constrains policy insights, and results in significant added cost.

Some Difficulties with Existing Systems of National Accounts

Existing systems of national accounts (SNAs) (e.g., GNP and gross domestic product (GDP) measures) exhibit difficulties when applied to intergenerational environmental planning.3 Four "failures" appear particularly troublesome to us:

-

Failure to separate "goods" and "bads." Medical care resulting from air pollution adds to GNP as do restoration efforts, pollution control equipment, and attempts to preserve species. Similarly, highly efficient or conserving practices with many positive externalities, but a very long payback period, fail to receive adequate consideration. One can imagine a society with an ever-increasing standard of living and an ever-diminishing quality of fife.

-

Failure to take account of opportunities foregone, such as the prospective value of species, or wilderness to future generations. The term "option value" was coined by economists to represent this form of valuation, but naming a concept is no substitute for finding a successful approach for including it in an analytical framework. This difficulty becomes particularly important when we consider that a market basket of goods today includes many goods that were previously nonmarketed or nonexistent one hundred years ago.

-

Failure to account for goods and services provided outside the marketplace. Current examples include housekeeper services provided by a homemaker, barter, fuel-wood collection, and hunting and gathering. Nonmonetized farm work a century ago was a huge contributor to national well-being. As the structure of society has changed and the number of small farms has dropped, this factor has decreased. On generational time frames even greater shifts could occur.

-

Failure to account for the value of time spent on voluntary and leisure activities. Methodologies such as "contingent valuation" attempt to deal with some of these problems, but the methodology appears extremely sensitive to the degree to which a problem is currently

-

popularized. Such techniques also have difficulty with aggregation when a range of alternative projects exist.4

Some of these difficulties can undoubtedly be dealt with by incremental improvements to existing accounting procedures. Other problems, such as inherent theoretical inconsistencies and bounded knowledge-synthesis limitations of the economic paradigm (Norgaard, 1990), appear more fundamental. For instance, while global warming may be troublesome to coastal dwellers in temperate regions, it may be seen as a boon to those in northern Siberia.5 Techniques that aggregate net welfare emphasize the notion of "compensating projects," which may not be appropriate in many situations involving environmental effects. In our view, the sum of the shortcomings makes us dubious of the efficacy of continuing to focus upon monetized accounts for addressing environmental problems, especially those that exist on intergenerational time scales. This is not to say that traditional economic analysis has no role. That role comes after policy goals have been established and after a range of acceptable paths, projects or policies have been identified. Traditional economic analysis is most useful for assessing which of a group of desirable choices or transition paths are most cost-effective.

In the next two sub-sections we discuss two specific difficulties associated with monetized green accounts that directly or indirectly address the four "failures" discussed above.

Intergenerational Discount Rates

Virtually all economic analysis makes use of the concept of the time value of money. From our perspective as scientists, we are dubious about the efficacy of evaluation tools that rely on the concept of the time value of money for assessing problems on multigenerational and highly ambiguous time frames.

The work of Mishan (1975:208-209) is aptly quoted by Cline (1992:239):

Whenever intergenerational comparisons are involved . . . it is as well to recognize that there is no satisfactory way of determining social worth at different points of time. In such cases, a zero rate of time preference, though arbitrary, is probably more acceptable than the use today of existing individual's rate of time preference or of a rate of interest that would arise in a market solely for consumption loans.

Cline observes, "Taken literally, Mishan's admonition would rule out benefit-cost analysis of the greenhouse effect." His review of the literature on long-term discount rates leads to the conclusion that the "social rate of time preference," which corresponds to the intergenerational discount rate, is somewhere in the range of 1-1.5 percent per year (Cline, 1992: Chapter 6). He concludes his discussion of these matters with a clear awareness that economic analysis may, even at its best, leave out considerations of importance to the public.

[E]conomists will do well to interpret the political reaction to alternative public initiatives as perhaps conveying information otherwise left out of the calculations. . . . Either the public is naive and sentimental and cannot make consistent calculations when it comes to the environment as opposed to other goods and services, or the public may be appropriately attaching some valuation in the environmental case that the economic analysis has failed to measure. . . . It should not be assumed automatically that the former is the case (p. 269).

Norgaard and Howarth explore intergenerational issues from the perspective of choice of intergenerational discount rates (Norgaard and Howarth, 1992; Howarth and Norgaard, 1992). Their fundamental conclusion is that distributional decisions should not be discounted, and that distributional decisions affect discount rates. Accordingly, society necessarily makes choices that impact discount rates, either implicitly or explicitly. Models that assume the same discount rate for all generations represent special cases with no particular claim to validity relative to other choices (see also Norgaard, 1991; and Howarth and Monahan, 1992).

The work of Norgaard and his collaborators provides a clear analytical demonstration that value judgments unavoidably enter into intergenerational economic analysis. The implication of these ideas for green accounting is to reinforce the idea, introduced earlier, that accounting systems must be designed so as to be congenial to many different views of the world, and that monetizing techniques should play a minor role in long-term goal setting relative to biogeophysically based approaches. Once goals are set, monetary techniques are essential aids to determining the economically efficient routes toward these goals.

Analysis Based on Single Numeraires

Most current national income accounts rely on the notion that all factors of importance can be expressed in terms of a single numeraire, usually monetary. The assumption is that a single monetized equation can be written to capture all relevant senses of value. This sum, which consists of "use value," "option value," and "existence value," is referred to as total economic value (TEV = use value + option value + existence value). A critical question for "green accounting'' is whether or not to adopt this perspective. Norgaard (1990) argues that the problems that we seek to resolve through developing green accounts are entangled in the issue of monetary valuation itself. He refers to this issue as the "value-aggregation dilemma.''

Our discussion of this issue focuses on the work of Pearce, Barbier, Markandya, and Turner. These scholars have been among the most effective advocates for the single numeraire point of view.

Pearce and Turner argue that all relevant multiple senses of value can be incorporated into existing economic tools:

We have seen that the passing-on of the resource base "intact", i.e. constant natural capital stock KN, over the next few generations is central to the concept of sustainable economic development. Such a managed growth policy, although directed primarily toward the satisfaction of human needs, would also necessarily ensure the survival of the majority of nonhuman nature and its natural inhabitants. Adequate environmental safeguards are available therefore without the need to adopt any of the radical 'deep ecology' arguments and ethics. In particular it is not necessary to have to accept the notions of intrinsic value in its widest sense, or of equal fights for all species. Our sustainability principle is general enough to encompass the environmental ethical concerns of consequentialist philosophy, as well as meeting the intergenerational equity objective (Pearce and Turner, 1990:238).

The core idea underlying Pearce and Turner's "sustainability principle" is the hypothesis that there exists in principle a scalar quantity, KN, which completely characterizes the "natural capital stock." They argue that keeping this single numeraire constant will ensure that both human and nonhuman life will thrive. While the symbol is clear enough, the procedure for operationalization is not.

Why should it be assumed that a single scalar quantity for measuring natural capital stock should even exist? If it does indeed exist, then in what units, and over what time horizon should it be defined? How is one to include the functional integrity of ecosystems, species diversity, ecosystem health, the economic value of natural resources, and human quality of life in a single optimization equation?

Von Neuman and Morganstern, in their classic work, Theory of Games and Economic Behavior (1947), underscored the conceptual and theoretical impossibility of solving such pseudo-maximum problems:

This [form of optimization problem in the context of a social exchange economy] is certainly no maximum problem, but a peculiar and disconcerting mixture of several conflicting maximum problems. . . . This kind of problem is nowhere dealt with in classical mathematics. We emphasize at the risk of being pedantic that this is no conditional maximum problem, no problem of the calculus of variations, of functional analysis, etc. It arises in full clarity, even in the most "elementary" situations, e.g., when all variables can assume only a finite number of values. (von Neuman and Morganstern, 1947:11).

Von Neuman and Morganstern's admonishment has not been adequately recognized. For example, one need only to refer to the frequent references discussing the desirability of policies leading to "the greatest good for the greatest number"—a clear example of "one too many 'greatests'" (Daly, 1980a:353). The popular misunderstanding motivating attempts to "solve" such pseudo-maximization problems still persists. We must re-emphasize von Neuman and

Morganstern's warning (1947:11) that "[a] guiding principle cannot be formulated by the requirement of maximizing two (or more) functions at once."

Pearce and Barbier, in another paper, adopt a more conservative stance by accepting that many natural resource functions cannot be substituted by man-made capital (Barbier et al., 1990:1260). Nevertheless, they persist in their belief that the cost-benefit analysis (CBA) should be maintained. They argue that alternative objective functions can be chosen which "extend" the CBA framework beyond economic efficiency. Turner and Pearce even argue that "moral" and "cultural" capital can be incorporated into CBA (Turner and Pearce, 1993).

A corollary effect of further theoretical, philosophical, and practical concern is this approach's dependence upon "compensating projects" to mitigate the net negative environmental effects of the collection of projects at the program level. In order to accommodate economic sustainability considerations, they modify the usual economic efficiency (positive net benefits) with an additional constraint that requires zero or negative natural capital depreciation. Pearce and his collaborators posit a "weak sustainability" criterion that aggregates in the time dimension, requiring the sum of individual damages to be zero or negative (i.e., the present value of the sum of environmental damages is constrained to be nonpositive). A "strong sustainability" criterion is also proposed. It constrains the sum of environmental damages to be nonpositive for each time period. Thus, rather than achieve global sustainability through extension, by requiring local sustainability, Pearce and his collaborators attempt to integrate sustainability considerations into the CBA through the concept of shadow or environmentally compensating projects (Barbier, et. al., 1990:1260-1261). This approach, however, still allows whole ecosystems and human cultures to be annihilated as long as the net "natural capital stock'' is maintained.

This body of work is still largely conceptual. It remains to be seen whether it can be operationalized in a manner that will find broad acceptance. Nevertheless, we must assert that analytical approaches that presume the existence of compensating projects, when the fungibility between environmental goods and services and man-made capital is largely unknown (and may remain largely unknown), rest upon a shaky footing.

Biogeophysical and Energy-Related Approaches

Many ideas for modifying traditional accounting procedures to better include environmental considerations have been proposed. Some of these are based on modifications of economic accounting techniques (e.g., Cobb, 1989; Ahmad et al. 1989; Anderson, 1991). Other approaches focus on physical accounting, especially energy (IFIAS, 1975; Hannon, 1982; Slesser, 1978).

Pearce et al. (1989) discuss several approaches to revised national income accounts including the French and Norwegian physically based accounts, the monetized Japanese Net National Income approach, and the Indonesian Sustainable Income approach. It is important to realize that any monetized approach is necessarily derivative of disaggregated biogeophysical accounts, which are then monetized at a later time. We emphasize again, because of this fact and because other modeling efforts require nonmonetized data, that revised accounts should be based upon disaggregated, biogeophysically based data. Additional arguments for maintaining biogeophysically based accounts include: information loss, explicit incorporation of uncertainty,

difficulties in performing sensitivity analyses, and costs associated with monetizing such data (Hufschmidt, 1983). Most significantly, by inhibiting the application of alternative transfer models, monetized accounts substantially constrain the range of possible policy insights.

An Alternative Transfer Model: Multicriteria Techniques

Approaches for analyzing green accounts that both take von Neuman and Morganstern's admonition to heart and are capable of considering multiple goals, measured with a variety of incommensurable units, already exist. The term "multiple criteria" or "multicriteria decisionmaking" (MCDM) has been given to a general collection of approaches for making decisions in the presence of multiple and often conflicting criteria. A characteristic of these techniques is that there is an effort to recognize explicitly that social decisionmaking has multiple goals, and that attempts to measure all of them using a single scalar are doomed to failure.

A major element of multicriteria approaches is that they aim to capture all relevant foreseeable impacts in their most appropriate and representative units. This is done to accurately reflect and assess the existence of tradeoffs. Multicriteria approaches are characterized by their attempts to systematically structure the various elements of the decision process in a manner that is flexible, clear to the decisionmaker and adaptive to changing circumstances (Nijkamp, 1985). These ideas, we believe, must lie at the foundation of all green accounting.

Four terms—attributes, objectives, goals and criteria—frequently appear in the literature on multicriteria decisionmaking. While there is no clear consensus on their definitions and some overlap exists, it is helpful to both make some distinctions between the terms and use them consistently. We believe that a deeper understanding of these terms can facilitate the conceptual development of green accounts. Our usage incorporates notions from Hwang (1981) and Zeleny (1982).

Attributes: Attributes are descriptive performance parameters and properties of alternatives. Each alternative can be characterized by a set of attributes. While attributes cannot be separated from decisionmakers' values and model of reality, they can be characterized and measured in relative independence from particular decisionmakers' preferences. For example, some attributes currently under consideration for defining sustainable forestry practices include: soil fertility, erosion hazard rating, watershed quality, tree basal area, diameter at breast height, ease of harvest, species diversity, age diversity, fire-hazard potential, etc.

Objectives: After attributes have been characterized and measured, decisionmakers must decide which attributes are desirable to "maximize" or "minimize." When particular desirable values are not (or cannot be) specified in advance and the aim of evaluation is to maximize or minimize (optimize), the most desirable levels of achievement are characterized by objectives. Objectives represent decisionmakers' normative preferences. By incorporating these preferences, by being assigned a particular direction of desirable improvement, attributes are transformed into objectives. For example, a utility company may be concerned with several objectives. It may want to maximize net energy efficiency, minimize pollutant emissions, and minimize production cost. High-level, aggregated objectives, such as "least-cost energy production" and

"maximization of environmental improvement" may need to incorporate several attributes and several lower-level sub-objectives.

Goals: Goals represent particular desirable performance values or levels of achievement (targets) that decisionmakers supply in advance of the evaluation process. They are defined in terms of specific attribute values or objectives. Goals are to be achieved, surpassed or not exceeded. They are often referred to as constraints because they serve to limit or restrict an alternative set. Automotive fuel efficiency (CAFE) standards and pollution emissions restrictions represent goals for industry.

Criteria: Criteria represent general measures, rules and standards that help to guide the decisionmaking process. They represent the basis for evaluating alternatives. All three categories, attributes, objectives and goals, can serve as relevant criteria for an actual decision process.

Multiple criteria techniques are divided into two substantial categories: those that are suitable for discrete choice problems and those that address continuous problems. A wide range of solution techniques have been formulated to address each category.

Multiple objective decisionmaking (MODM) is associated with problems where the alternatives are not predetermined or prespecified. An example would be determining the appropriate amount of carbon to be emitted to the atmosphere in various years, subject to competing demand, environmental, population, and cost constraints. The problem is one of continuous evaluation because particular scenarios have not been specified. Extensive discussions of solution techniques appear in Cohon, 1978; Hwang and Masud, 1979; and Goicoechea, 1982).

Multiple attribute decisionmaking (MADM) is distinguished by the existence of a countable small number of predetermined alternatives. An example would be selecting from an array of specific technologies (e.g., solar thermal, photovoltaic, pressurized water reactors, intrinsically safe reactors, fusion reactors). The decision problem involves selecting, prioritizing, or ranking the alternatives in a manner that "best" satisfies a range of objectives. Extensive discussions of solution techniques appear in MacCrimmon, 1968, 1973; Rietveld, 1980; Hwang, 1981; Voogd, 1983; Nijkamp, 1990; and Chen, 1992.

Multicriteria techniques have been applied to a wide variety of urban and regional planning problems, including land reclamation (Nijkamp, 1974), evaluation of forest road investment projects (Gomes, 1975), analysis of airport location issues (Palinck, 1977), evaluation of landscape plan alternatives (Xiang et al., 1987), and evaluation of urban transportation system alternatives (Gomes, 1989), to name a just a few of the myriad of applications. While further development and application is needed, this approach holds great promise for quantitative and qualitative analyses of sustainability considerations.

EXAMPLES OF ALTERNATIVE TRANSFER MODELS: RADIOACTIVE WASTE AND GREENHOUSE WARMING

Radioactive waste disposal and greenhouse warming both operate on and must be analyzed using intergenerational time scales. We treat the first example, radioactive waste, descriptively. The second example, the impact of anthropogenic carbon dioxide on agriculture,

is used to illustrate explicitly the "transfer model" concept which we believe has much promise as an integrative tool for reflecting divergent points of view and uncertainties in data.

Radioactive Waste

While controversy over specifics remains intense, there is broad consensus that storage techniques for radioactive waste can only be considered acceptable if they hold the promise for sequestration over time spans of millennia. US-EPA guidelines for high-level radioactive waste storage must "meet radioactive release limits . . . that would result in less than 1000 deaths in 10,000 years" (NRC, 1990). This is one area where the public perceives a real risk to future generations and is willing to invest heavily in remedial measures. The discussion is couched in terms of social goals and human health, and most particularly in terms of a desire to leave an inhabitable world for our descendants.

Operationalizing the 10,000-year goal has proven difficult. Public opposition to specific proposals has been relentless. Credibility of institutions grappling with the problem is low (Slovic, 1990; 1991). Expenditures for planning and analysis continue to be enormous.

In an increasingly diverse society, issues relating to trust in institutions loom increasingly large. Methodologies for valuing the environment should be sensitive to the existence of a multiplicity of value systems. A review of public confidence in radioactive waste management by a Department of Energy (DOE) Committee emphasized the centrality of trust to the policy process (DOE Energy Advisory Board, 1992:9):

In the realm of radioactive waste management problem-solving, public trust and confidence is especially salient because of the high degree of technical expertise required for understanding, participation, and sound decisionmaking. In validating alternatives, there must be trust that uncertainties are resolved in an unbiased fashion. . . . IT]here must be trust that the full range of values and alternatives has been taken into consideration and that the interests of all have been recognized even if they are not accommodated.

Policy suggestions relevant to global climate change appear in the NRC report "Rethinking High-Level Radioactive Waste Disposal" (NRC, 1990). These suggestions make the point that while it may be possible to recognize a serious long-term problem, it may not be possible to make detailed plans for addressing it. Rather, it is better to try to identify worst case outcomes and design to minimize the chance that they will occur, while simultaneously recognizing that even the very best of plans will need modification as experience is gained. The NRC report made these points:

-

Realize that surprises are bound to occur (planners must "expect the unexpected").

-

Pursue an empirical exploratory approach: one that emphasizes fairness in the process while seeking outcomes that the affected populations judge to be equitable in the light of their own values.

-

Start with the simplest description of what is known, so that the largest and most significant uncertainties can be identified early.

-

Meet problems as they emerge, instead of trying to anticipate in advance all the complexities.

-

Define the goal broadly in ultimate performance terms, rather than immediate requirements.

These guidelines place emphasis on careful attention to obtaining all relevant information, and then using judgment to form policy. A wide variety of indicators are involved, many of which must necessarily be weighed judgmentally, not by formula. Because of the complexity of the phenomena, the "simplest description of what is known" tends to be quite complex, as well as full of lacunae.

What might one ask of a "green accounting" system that would provide insight into the implications of radioactive waste systems? Estimates of containment and leakage involve technological and geological extrapolations into regions where, in many cases, information is limited. Costs of control technologies have a long history of underestimation. Uncertainties about time frames for construction as well as time frames and probabilities for leaks to the environment make it difficult to estimate future costs, and make use of economic discounting techniques extraordinarily problematic. In practice, the public debate over nuclear waste has largely been framed in terms of perceived risk and confidence rather than economic benefit-cost analysis.

Radioactive waste management thus provides a major challenge to any new accounting methodology. Most technical analysis appears to show that the probability of truly disastrous accidents is small in all time frames. On the other hand, worst-case analysis gives rise to enormous social impacts. Public concern focuses on worst-case analysis, and public perception is strongly influenced by many examples of false assurance by both government and industry in the U.S. as exemplified by Hanford, Rocky Flats, and Three Mile Island, and by Chernobyl and Chelyabinsk in the Former Soviet Union. An accounting methodology that looks only at center line expert opinion will be no more credible than one that focuses on worst cases.

This overview provides convincing (to us) evidence that any green accounting system for radioactive waste that uses either single numeraires (point estimates) or monetary measures alone has no possibility of wide acceptance. Approaches more likely to win acceptance will emphasize probabilistic statements of a variety of outcomes, and will be structured so that the views of all major involved groups are accurately reflected in the spectrum. Accomplishing this goal will not be easy. We illustrate one way to proceed by presenting an illustrative, risk-based transfer model focusing on the impact on agricultural output of global warming.

Global Warming

Greenhouse warming is the most discussed aspect of long-term global climate change. "Greenhouse," in this context, refers to the prospect of global warming driven by substances introduced into the atmosphere by human activities. Greenhouse warming itself is not scientifically controversial. Absent radiation trapping, the average temperature at the earth's surface would be about 250K rather than the actual 290K, and far too cold for life as we know

it. Anthropogenic carbon dioxide, chlorofluorocarbons, and other greenhouse gases may be producing rapid warming with potentially serious consequences for virtually all life forms.

Typical current projections are for a rise in global temperature of from about 1°C to as much as 5°C within the next century. This is a rate of change far greater than has been seen historically. Figure 5-1 shows historical data, and several forecasts of what the next century might hold in store (Organization for Economic Cooperation and Development (OECD), 1991).

Whether such warming is occurring is not as yet proven. Correlations between carbon dioxide and global average temperature in this century are not especially striking. There is general agreement that about one degree Centigrade warming has occurred in the post-industrial revolution period. However, some data contradicts this—for example, tree ring results from South America (Lara and Villalba, 1993). Anticipated effects of anthropogenic gases on climate include large geographical variations, increased fluctuations of all sorts, and shifts in rainfall.

Major analyses have been conducted by many groups, including the U. S. Office of Technology Assessment (OTA, 1991), the Intergovernmental Panel On Climate Change (IPCC, 1991); the NAS (NAS, 1991); and the Dutch Government (Krause, 1988; 1989). A variety of perspectives may be found in Singer (1989). "Integrated Assessments" and models are among the analytical approaches in use (Dowlatabadi and Morgan, 1993; Rotmans, 1990). Methodological issues of the risk assessment approach may be found in Morgan and Henrion (1990). Qualifications to the risk assessment methodology (primarily in the context of near-term issues) are discussed generically in Shrader-Frechette (1991) and Hornstein (1992). A practitioner's perspective is given by Lash (1992). The U.S. government has set up a Carbon Dioxide Information Center (ORNL, 1991), which is one of dozens of relevant databases that will serve as the source for the information to be used in new accounting systems.

Dramatic as some predictions of adverse effects are, it is important to remember that they depend extensively on a worldwide database and large-scale computer models, both of which have severe limitations.

It is also useful to recognize that the scientific community has been anything but consistent in its collective attitude toward anthropogenic climate change. One of the discoverers of greenhouse warming, S. Arrhenius (SCEP, 1970), reportedly hoped the effect would make his native Sweden warmer and more comfortable. As recently as 1977 the meteorologist Reid Bryson prefaced a book "Climates of Hunger" as follows:

In 1973 an international group of scientists wrote to the President of the United States about a matter of grave concern. They were specialists in the history of ice ages, and they could see from the rhythm of past ice ages the possibility of another ice age within centuries, and almost positively within a few millennia (Bryson and Murray, 1977: ix).

At about this time careful work to explore global warming was beginning with the SMIC and SCEP studies pioneered by Carroll Wilson (SCEP, 1970; SMIC, 1971). These opened the modem era of climate study.

Today, interest in ice ages has virtually vanished (e.g., California Energy Commission, 1989), yet the memory of the scientific community changing its mind persists. As understanding of the effects of the proposed greenhouse warming increases, we can expect that, due to unanticipated effects, revisions in both directions will occur. Indeed, recent estimates show that

sulfate aerosols may cool, biosphere CO2 uptake may increase as CO2 levels increase, and ozone depletion may decrease radiation forcing (IPCC, 1992).

Greenhouse warming may well be a major threat to our society. The "Precautionary Principle" suggests that the mere possibility of its existence should motivate us to reconsider those actions which may be exacerbating such a phenomena. We ourselves believe that the weight of scientific evidence and the fact that cost-effective responses exist are sufficient to warrant placing the matter high on our social agenda. It is important, however, to recognize that the uncertainties remain great, and that there remain individuals of stature—though ever fewer of them—who argue that the evidence is not yet compelling. This view, in fact, was at the core of the Bush Administration global climate change policy agenda. Their "no regrets" strategy was based on the idea that the nation should make no investments in mitigation that might later on turn out to have been unnecessary.

"No regrets" policies stand in contrast to "insurance policy" strategies, known in this context as the "Precautionary Principle." Emphasis is placed on taking those precautions that make sense today, in anticipation of change in the future. Thus, for example, it is now policy in the Netherlands to build new off-shore oil drilling rigs and new dikes about 1 meter higher than previously planned just in case sea-level rise occurs. The argument is that it costs little to add one meter in new construction, but would cost far more to modify an existing structure later, should the need arise.

Human activities are certainly producing increases in atmospheric carbon and other anthropogenic gases. Changes in the global ozone system are being driven by anthropogenic chlorofluorocarbons. Yet experimental observation of effects on ecosystems due to increases in greenhouse gases is as yet problematic. There is consensus within the global scientific community on a significant possibility that warming of several degrees Centigrade could occur within the next century. However, the magnitude of the effect must be estimated using large-scale models, and there remains great concern as to the validity of these models, both in forecasting average temperature responses and, especially, in forecasting regional responses. Understanding of fluctuation phenomena, including weather of all types, which is likely to be of immense importance to biological systems, is at a far more rudimentary level.

Response of biological systems (including both natural ecosystems and human agricultural systems) to temperature change and to weather fluctuations is poorly understood. We find no consensus, except that responses might turn out to be large and nonlinear, and that systems with long internal response times are likely to be particularly vulnerable. Forests are probably the most important case in point. Forests grow slowly, and a change of a few degrees over a century could lead to die-out in some regions and inadequate time for new growth in others. They could either contribute to stabilization, or amplify threats of global warming (Rosenfeld and Botkin, 1989), with the possibility of catastrophic collapse.

One consideration that makes plausible inclusion of "collapse" possibilities in global climate change analysis is that we have evidence for such effects in the past. Examples include the Mayans and Incas in Central and South America; cities in the cradle of civilization such as Petra, Baalbek, Persepolis; and the American desert culture of the Anasazi. In every case there is debate about the origins of the collapse, but overextension of the agricultural base is invariably one of the most discussed possibilities, sometimes driven or abetted by extended periods of drought (Carter and Dale, 1974). Developing nations are especially vulnerable.

Cohesion within the international scientific community is clearest in the reports and deliberations of the newly formed Intergovernmental Panel on Climate Change (IPCC, 1992). Scientific members of the IPCC axe close to and trusted by their governments, and their concerns are reflected in governmental attitudes. There is also a great deal of nongovernmental interest in global climate change, which also contributes to driving the policy process.

Thus far there is rather little policy in place relating directly to global climate change. The Montreal Protocol, an international agreement that is leading to the phasing out of one set of anthropogenic greenhouse gas, chlorofluorocarbons (CFCs), is one example.

Econometric Approaches for Examining the Impacts of Global Climate Change

Several efforts have been made to use econometric tools to examine the impact of global warming. The work of Cline (1992), Nordhaus (1991), and OECD (1992) is particularly interesting. Cline and Nordhaus seek to estimate the economic impact of doubling of greenhouse gases. The two studies have been compared by Howarth and Monahan (1992), who have summarized the assumptions and have made some corrections in order to place them on comparable footing. The key results are that Cline's annual cost to the U.S. of a doubling of greenhouse gases is estimated as 1.25 percent of 1981 income, while Nordhaus' estimate is 0.26 percent of 1981 income.

An OECD study (1992) finds the estimated annual damage from global warming to the U.Ss economy to be $61.6 billion (1990 dollars) for a doubling of CO2 leading to 2.5°C temperature increase, and $338.6 billion (1990 dollars) for long-term warming of 10°C.

These annual costs of global warming are relatively small percentages of GNP. The uncertainty in growth rate of total GNP is far greater. Accordingly, given the discussions of the prospect of ecological or biological collapse it is not surprising that these results are sometimes described, especially by Cassandras, as missing the point. Given the uncertainties, they are consistent with no adverse effect upon economic growth.

From an ecological perspective, any work that leads to a primary conclusion that greenhouse warming a century hence is probably only a few percent of GNP seems problematic. The issue is basically one of how one analyzes uncertainty and risk. It may well be that the current ''best" estimate of loss is modest. If, however, there is a significant chance that actual losses will be much greater then there axe very different policy implications. At issue is whether society wants to make its planning decisions on the basis of averages, worst-case analysis, or other planning rules. We argue that, to be acceptable, accounting systems must support the acknowledgement of both optimistic and pessimistic minority positions.

An Alternative Transfer Model Approach for Examining the Agricultural Impacts of Global Climate Change

We illustrate our concept of transfer models using a highly simplified conceptual example. We consider just three categories: greenhouse gas emissions due to carbon dioxide,

warming and fluctuations due to these emissions, and response of the agricultural system to warming.

We focus on the agricultural sector since a major problem in that sector would be critical to every society. It is important to recognize that in industrial nations, the economic contribution of on-farm activities to total GNP is quite small. Since food is critical to any society, it is clear that if global warming has severe adverse impacts on this sector, then there would be major repercussions throughout the society. Green accounts should be sensitive to this issue.

In practice, many more categories would be required to adequately represent the level of complexity and range of feedbacks involved. The task of determining how many categories are necessary, and how to keep the number of categories from growing too large to be manageable remains an issue for research.

The links we consider are:

|

Carbon input |

= > temperature and temperature fluctuations |

|

|

= > agricultural and ecological system impacts |

-

Greenhouse gas emissions. A proper accounting scheme should include all substances that might contribute significantly to the greenhouse effect. We consider carbon as a surrogate quantity.

-

Warming. A proper accounting scheme will include the differential impact of various substances, the local climatic impacts, and fluctuation phenomena (which some believe may prove far more important than shifts in means). We aggregate to a single functional relationship between greenhouse gases and global temperature.

-

Agricultural and ecological impacts. The impacts of warming and temperature fluctuations can affect many aspects of society. We restrict discussion to one impact—the globally averaged impact on agricultural output. Detailed accounting will require geographic disaggregation.

These three elements form a causal sequence (with feedback). Examination of feedbacks is, however, not our goal. We are interested in providing an example that explicitly includes multiple perspectives and uncertainty. The methodology has the capability to include a multitude of expert views, integrated via statements about the statistical properties of the views of experts.

Carbon emissions are believed to be causally related to global temperature. Specification of this relationship in detail requires large-scale models. For simplicity we let average global temperature vary linearly with delayed cumulative global carbon input. More realistic delay mechanisms could be included. A practical version of the methodology might use expert judgment to provide estimates of temperature as a function of both time and greenhouse gas input, using a particular model of analysis.

Agricultural output is assumed to decrease logistically with global temperature increase. Parameters depend on temperature, temperature fluctuations, technological optimism (e.g., about

bioengineering), etc. The relation between anthropogenic global climate change (warming and temperature fluctuations) and agricultural output has been studied only very little, so this part of the transfer model is likely to be the most uncertain (e.g., Knox and Scheuring, 1991). On the other hand, if anthropogenic gases do impact agriculture significantly, this part of the model could well be determinative. The model we use here is discussed in more detail in the appendix at the end of the paper (p. 107).

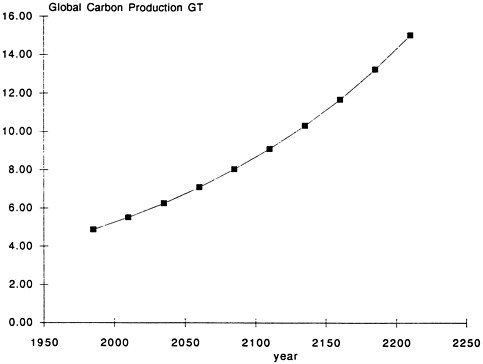

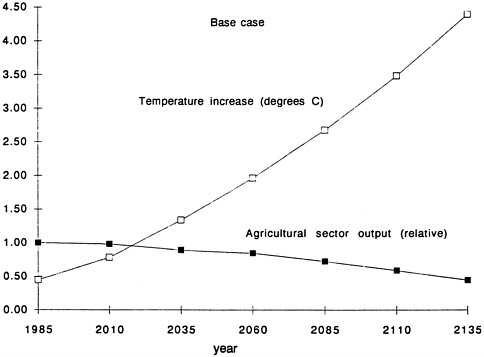

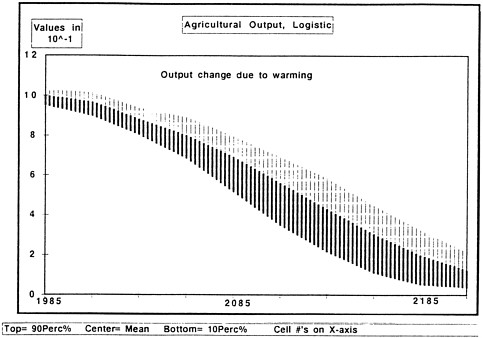

Figure 5-2 shows an illustrative baseline growth in human carbon production. Figure 5-3 shows the baseline illustration of temperature increase and the baseline agricultural output decline due to temperature increase.

At this stage probabilities are introduced. Experts (and others) contribute opinions on parameters that drive the system responses. These views are assembled into probability distributions. The implications of the probability distributions are propagated through the model so as to provide a clear picture of how much consensus exists, and of how lack of consensus in one area impacts other areas.

Expert opinions are only loosely related to probability. Surprises occur. With time and new information expert views will change. The process is, in essence, collecting Bayseian priors. New information and concepts can lead either to changes in the probability distributions (maintaining the structure of the system fixed) or to changes in system structure.

For illustrative purposes we include uncertainty as follows. Growth of carbon (and other greenhouse gases) is assumed to follow an exponential path. The coefficient of the exponent in the base case, is distributed by a normal probability distribution. The relation between carbon emissions (a surrogate for all greenhouse gases) and temperature is also distributed normally. Finally, the parameter in the logistic function is normally distributed.6

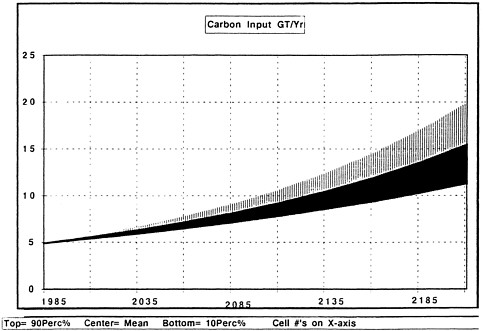

Figures 5-4 through 5-6 (for carbon, temperature, and agricultural output) illustrate the spreads of values obtained when probability distributions are introduced. The means are required to be identical to those in Figures 5-2 and 5-3. The bands show the 10 percent and 90 percent probability zones.

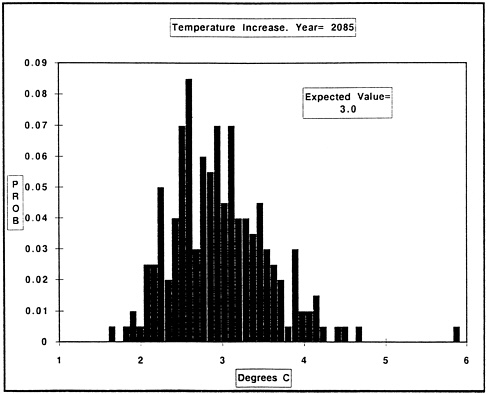

A primary goal of the approach is to allow ready discussion of the implications of different views of the causal relation between atmospheric carbon and its impact on the biosphere. A good way to make the implications clear is to look at the probability distributions for a particular year. Figure 5-7 shows the distribution of temperature in year 2085. The ''raggedness" of the data results from the sampling procedure.

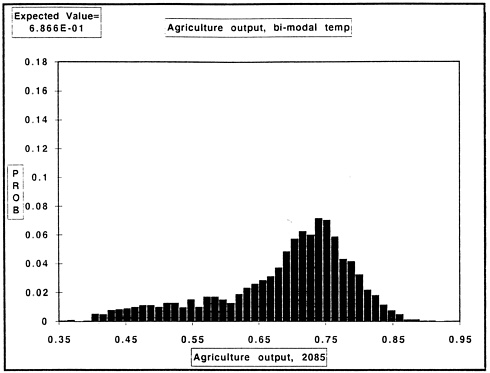

The example shows how statistical distributions give rise to a most likely shift of 3°C (as it must), a significant chance of 2°C and 4°C shifts, and a very small probability of a shift of 6°C. Figure 5-8 shows the distribution of agricultural productivity in 2085.

Risk and Uncertainty Made Explicit

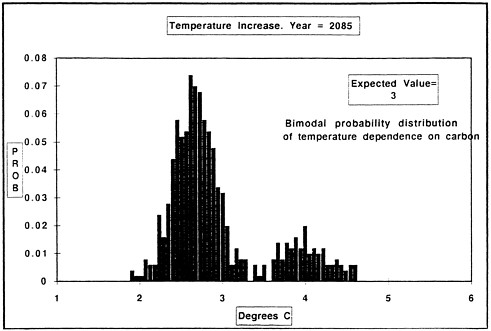

The relation between cumulative global carbon and temperature is controversial. Suppose there are two theoretical constructs leading to two rather different relationships. Does this

FIGURE 5-4 Inclusion of uncertainty changes the point calculations in Figure 5-2 to uncertainty bands.

FIGURE 5-5 Inclusion of uncertainty changes the point calculations in Figure 5-3 to uncertainty bands.

FIGURE 5-6 Inclusion of uncertainty changes the point calculations in Figure 5-3 to uncertainty bands.

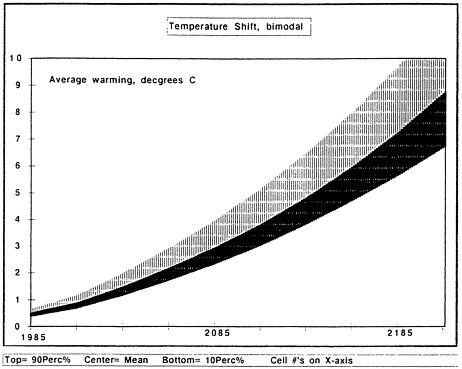

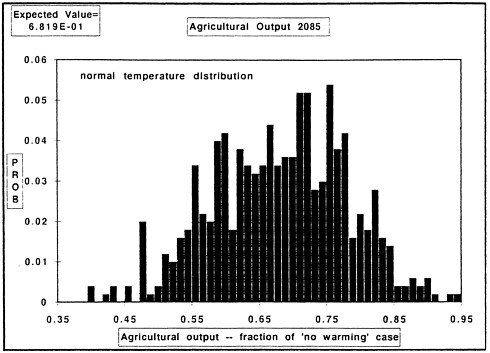

matter? In this example the focus is the impact on agriculture, which also entails uncertainty. We describe disagreement among experts by using two normal probability distributions. One of these leads to a most likely temperature increase of 2.5°C in the year 2085, the other to a most likely increase of 4°C in 2085. The two distributions are weighted at 80 percent and 20 percent respectively, so the most likely warming in 2085 remains 3°C. When this probability is folded with the distribution on greenhouse gas emissions, the result for 2085 is bimodal but blurred (Figure 5-9).

However, when one examines the agricultural output (Figure 5-10), the bimodal temperature distribution is no longer visible. Instead, one finds an asymmetrical agricultural output distribution peaking a bit at about 72 percent of the base output, with an expected value of 68 percent of the base, and with a significant probability of only 45 percent of base case output. The uncertainties among experts in relating warming to temperature are large enough that they barely affect the final estimates of agricultural output.

This is an example of how a probabilistic approach can help focus discussion on where better information may make a difference, and where improved data may be necessary. Such analysis can help focus research programs on areas where acquisition of new or improved data matters most. Most important, the probabilistic aspects of this particular transfer model approach provide a way to explore implications of minority views, to examine the sensitivity of certain planning paths to different assumptions, and to include the concerns of optimists, pessimists, and the range in between.

DIRECTIONS

We argued that green accounting for the long-term is inextricably intertwined with goal setting and social values. Our images of desirable futures serve as the basis for such goal setting. These images must be explored, scrutinized, and discussed. Carefully constructed green accounts have the potential of helping us to analyze a selection of feasible transition paths for realizing desirable future states.

There are many views of the future. To some, technological ingenuity and ''progress" will provide future generations with undreamed of opportunities and few adverse side effects. This is the optimists' view. To others, the pessimists, our generation is depleting irreplaceable resources. We are impoverishing our descendants and the rest of the world's inhabitants. Such differences in world view, while unlikely to be resolved, can be discussed beneficially. A green accounting system must be capable of representing the views of optimists, pessimists, and the wide range in between. It should also take into account the possibility that if technological optimists turn out to be wrong we may be left with an impoverished world. One of the main goals of green accounting should be to help us reduce the likelihood of realizing such an undesirable scenario.

These considerations lead to several general observations:

-

The structure of existing accounting systems contains biases. Among the most important of these are biases in favor of quantities that enter into commerce, in favor of flow quantities, and against stocks.

-

Innovation has created ''resources" where none previously existed, but has also lead to new types of side effects. Improved procedures are needed for anticipating side effects, especially those which may be uncertain in character and delayed in time.

-

The concept of limits is not made explicit in most prevailing accounting systems. Limits may be reached so rapidly that there is inadequate time to develop alternatives. In addition, the mere fact of approaching limits may result in bifurcations and irreversibilities (e.g., indirect species extinction resulting from loss of critical habitat).

These broad principles lead to a general recommendation which is in the spirit of Ann Harrison's final recommendation presented at a UNEP-World Bank Symposium (Harrison, 1989):

Accounting systems should be structured so that they "show for all capital—man-made, natural and human—the ratio of stock at the end of the period to that at the beginning."

This broad guideline is open and flexible, but implementing it is difficult. We make several observations directed towards facilitating implementation:

-

Many kinds of measurement units should be included in a green accounting system. When long-range and multicriteria problems are involved, biogeophysical and equity indicators must figure prominently. Econometric techniques become most important after goals have been set and near-term policy decisions are required.

-

Green accounting systems should be fashioned so that very different types of indicators, with different spatial and temporal scales, can be constructed. Some of these will be highly aggregated; others will focus on highly specialized questions (e.g., the number and health of particular species in a given region).

-

Uncertainty is intrinsic and must be made explicit. Approaches for analyzing green accounts must admit minority views, thereby recognizing that, not infrequently, today's minority position is tomorrow's reigning paradigm.

-

Green accounting systems should be dynamic and flexible. They should be structured so that their internal organization can be updated as new indicators and information become available.

-