2

Consumer Electronics

It is commonly believed that U.S. manufacturers cannot compete with offshore manufacturers because the United States is a "high-cost" manufacturing environment, particularly with respect to direct labor. An examination of the consumer electronics industry, however, demonstrates that this high-cost labor scenario is not really descriptive of the realities faced by manufacturers in this industry.

The committee has used an analysis of two products to demonstrate when labor costs can and cannot be a decisive factor in site location decisions by consumer electronics manufacturers. The analysis focuses on two products: an AT&T telephone and a Toshiba color picture tube. Both products are manufactured in the United States and abroad. Each company chose to locate facilities abroad for different reasons: AT&T sought rapid cost reductions achievable from lower labor costs abroad, and Toshiba sought greater market access security.

The committee's analysis of the manufacturing costs of these two products revealed how complex site selection can be. Although AT&T shifted production of business telephones to Singapore in 1984, at a time when direct labor accounted for 22 percent of the cost of goods. sold (COGS) in its U.S. factory, productivity improvements over time have changed the relative benefits of offshore labor. In fact, AT&T's 1990 study shows

that differentials in the cost of materials, not direct labor, now provide the offshore cost advantage.

Further, the committee has found that direct labor costs and, for that matter, total production costs are not necessarily higher in the United States than they are abroad. The Toshiba analysis demonstrates that the manufacturing cost for a color picture tube is actually lower in the United States than in Japan (a function of exchange rate differentials). Clearly, the assumption that U.S. manufacturers are at an insurmountable disadvantage because they work in a high-cost labor environment does not square with the experience of these two manufacturers.

THE AT&T EXPERIENCE

Background

In the wake of the Federal Communication Commission's deregulation of domestic telecommunications equipment on January 1, 1983, AT&T was forced to make the transition from a partly regulated to a fully competitive environment. Before the breakup, AT&T leased telephones to its customers, so its ultimate objective was to achieve the lowest overall life-cycle costs, leading customers to associate reliability with all telephones. With the breakup of AT&T, however, consumers began buying their own telephones and foreign manufacturers began to flood the marketplace with inexpensive and, in many cases, poor-quality equipment. AT&T lost market share to these new producers, some of which it regained when customers found many of the low-cost new telephones lacking in quality.

To become more competitive, AT&T had to control its production costs. This would be difficult, however, since the mindset in both the factory and the corporation was still shaped by reliability considerations. Responsiveness was undervalued. This mindset produced high prices, falling revenues, and low profitability.

In response to these problems, AT&T implemented a restructuring plan, "Project Turnaround," to reevaluate its product line and control costs. The objectives of the project were to:

-

absorb a cost structure established for a very different business

-

revise a revenue stream in decline (a leased base of telephone equipment)

-

overcome unacceptable profitability projections

-

merge cultures from many former Bell System organizations

Ultimately, AT&T needed to make its consumer products business profitable if it was to survive in the new environment. Yet these products were, in many instances, not competitive with the rest of the industry. For products manufactured in the United States, the COGS was 75 to 95 percent of net revenue. The industry analog, however, was 60 to 65 percent. Further, it was unlikely that the onshore labor cost disadvantage could be rapidly overcome by cost improvement programs. Labor cost advantages offshore were simply too great.

To meet the challenge of manufacturing a new line of residential products quickly, at sufficient quality and price to yield good margins, AT&T turned to offshore manufacturing. Existing residential products were phased out of U.S. factories and a new line of products was manufactured offshore, either in AT&T-owned facilities in Singapore or by suppliled called original equipment manufacturers1 (OEMs), typically in Korea, Hong Kong, or Taiwan. Effectively, this decision was taken because the immediate benefits of moving offshore outweighed the cost and difficulty involved in bringing its domestic factories up to world-class standards.

The decision either to outsource or to manufacture abroad was made on the basis of certain attributes of foreign manufacturing environments that AT&T found attractive. The attributes or "attractors" that initially brought AT&T to foreign manufacturing locations were:

-

access to low manufacturing costs: materials, labor rates, duties (Generalized System of Preferences status), taxes, transportation

-

access to skills (engineers, technicians, managers who had not been "tainted" by outdated management styles)

-

access to OEMs that made products AT&T found too costly to build in the United States

In the wake of AT&T's restructuring, several of its manufacturing operations are now located offshore. This global manufacturing network now includes capacity in Singapore, Taiwan, Thailand, Hong Kong, other Asian countries, and Mexico. Further, after benchmarking domestic operations against foreign ones, AT&T has improved its domestic manufacturing capabilities. Improved onshore manufacturing, in turn, is altering the criteria by which AT&T makes site location decisions—making onshore manufacturing more attractive in all performance categories, including cost.

AT&T Product Cost Analysis

In 1990, six years after the consumer products' turnaround plan was implemented, AT&T reexamined comparative manufacturing costs between domestic production and offshore OEM production in a range of consumer product lines. This new analysis was undertaken to:

-

identify and understand full-stream costs

-

identify and understand the sensitivity of the key drivers of cost

-

quantify hidden cost elements

-

develop a benchmark for onshore manufacturing

-

refine existing make/buy analyses

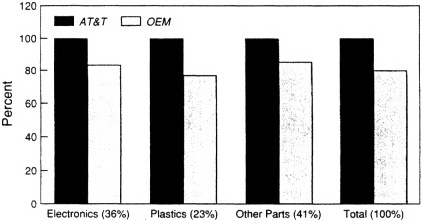

This analysis disaggregated the COGS into four categories, specifying the cost advantage for that component if the items were to be manufactured offshore (Table 2-1). After estimating the total onshore/offshore cost differentials when landed in the United States, the offshore cost advantage was found to be 8 percent. To find ways of reducing that differential, cost components and drivers were analyzed in further detail.

Labor Analysis

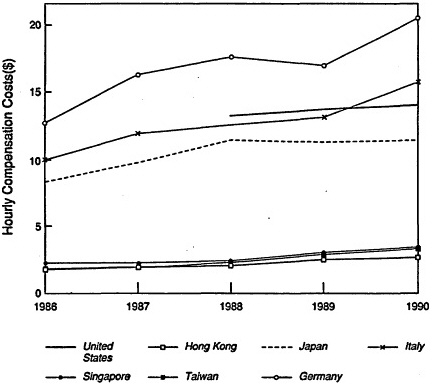

While it is clear that dramatic differences in wage rates across countries (see Figure 2-1) make foreign manufacturing locations attractive for labor-intense operations, AT&T's study showed that in-plant direct labor, in fact, accounts for a small proportion of production costs for the products examined. Even with a wage differential as high as 85 percent, the low percent-

TABLE 2-1

AT&T's Analysis of Onshore/Offshore Manufacturing Cost Differentials

|

|

Component of COGS (%) |

|

|

|

|

Typical Domestic |

OEM |

Offshore Cost Advantage (%) (Disadvantage) |

|

Labor |

9 |

4-10 |

40-85 |

|

Load (includes overhead salaries, benefit costs, taxes, and building/equipment depreciation and maintenance) |

14 |

3-13 |

40-80 |

|

Materials |

70 |

50-80 |

12-20a |

|

Functional Drivers Adding to OEM Costs (includes transportation, duties, OEM administration, quality management, purchasing operations, R&D costs, fixed central expenses, tooling depreciation, make-to-order) |

N.A. |

26-41 |

(24-40) |

|

a When consigned parts—parts supplied to the OEM by AT&T—are included. For other than consigned parts, the offshore cost advantage ranged from 13 to 28 percent. |

|||

age of labor costs in COGS (9 percent) means that eliminating that differential reduces total loaded costs by only 4 to 10 percent. How important that differential is in a cost reduction strategy depends on the product and the opportunities to reduce costs in other areas.

For some products in some markets, a potential 10 percent cost savings can mean the difference in being competitive. In general, AT&T's more labor-intensive products, which tend to be fairly unsophisticated technologically, are more likely to benefit from offshore production. Low-technology products that are hand assembled cannot be competitively manufactured in the United States. Though an analysis must be performed on every case, AT&T has found that a product with a fully loaded manufacturing cost of about $50 is likely to be produced more cost competitively offshore; as onshore production continues to improve, that threshold will fall lower.

Figure 2-1

Hourly compensation costs for electric/electronic equipment (SIC 36).

Source: U.S. Bureau of Labor Statistics, 1991.

Load Analysis

AT&T found that load is a major driver of the cost differential between onshore and offshore manufacturing because load rates are much lower abroad and load is a significant portion of COGS (14 percent). Typically, about half of load costs are incurred in fixed building-related costs, equipment depreciation, salaries for indirect labor, and other direct costs. Consequently, as equipment requirements increase with higher-technology products, load becomes a higher proportion of total costs and the onshore/offshore differential declines. The offshore producer is faced with the same need to invest in capital equipment for sophisticated product manufacture as AT&T.

For the products examined, load percentages range from 12 to 16 percent for AT&T onshore manufacturing, compared with 3 to 13 percent for offshore suppliers. The wide range for OEMs is due to their specialization in different technologies. OEMs that produce low-technology, manually assembled products require little capital investment and therefore have lower load rates. OEMs that produce higher-technology products tend to have load rates comparable to those of AT&T.

Salaries and wages for indirect labor (engineers, managers, and administrative personnel in the plant), which are another component of load, are a source of some of the onshore/offshore load differential. As Table 2-2 illustrates, foreign engineers and managers are substantially less costly than comparable U.S. personnel. Because engineers are less expensive, foreign managers at AT&T's suppliers' plants typically use more of them in manufacturing operations that must achieve high yields quickly. AT&T has found that foreign engineers are as competent as their U.S. counterparts and are often assigned in large numbers to manufacturing process improvement (an assignment that is frequently undervalued in U.S. factories). This focus on yield improvement, in turn, reduces production costs as yields increase.2

AT&T's onshore plants have historically reduced their own loads by about 5 percent each year through the more efficient information and engineering systems that have been installed to enhance white-collar productivity. Similarly, it is assumed that offshore OEMs make the same kinds of improvements and so will continue to maintain appreciably lower load costs.

TABLE 2-2

Average Salary of Key Positions (U.S. dollars)

|

|

“Greenfield” |

Mexico |

Malaysia |

|

Senior engineer |

$52,500 |

$13,300 |

$28,100 |

|

Engineer |

40,000 |

11,400 |

17,160 |

|

Production supervisor |

28,000 |

7,100 |

14,900 |

|

Secretary |

18,500 |

5,200 |

6,600 |

|

SOURCE: AT&T (1989). |

|||

Materials Analysis

Because labor cost differentials tend to dominate discussions of onshore/offshore manufacturing costs, the actual cost impacts of the materials used to build products are often both underestimated and misunderstood. A cost analysis reveals that, at least with respect to this product, materials are the largest proportion of COGS (70 percent). Although the onshore/offshore materials cost differential is smaller than that of other components (it is less than a third of the differential for labor or load), a relatively small change in the cost of materials can significantly cut total manufacturing costs.

The AT&T cost study found that because AT&T is not a local manufacturer in certain areas, it buys materials at a disadvantage. Even when AT&T operates offshore plants in close proximity to OEMs, there is still a substantial price differential—ranging from 6 to 8 percent—between prices quoted to AT&T and those gained by local manufacturers.3 Considering the large share that materials represent in the total manufacturing cost of telephones, a 10 percent reduction in the cost of materials is equivalent to a 35 to 40 percent reduction in labor and load costs. Looked at another way, reducing the cost of materials by 10 percent at an onshore production facility would trim 7 percent from the fully loaded manufacturing cost. A 7 percent decrease in manufacturing costs, in turn, is often enough to make higher-technology products made in the United States cost competitive with those produced offshore.

This cost differential in materials is in part a consequence of U.S. withdrawal from the consumer electronics industry. For AT&T's product set, abandonment of the consumer electronics industry in the United States is now having a ripple effect that goes beyond that specific industry. Many of the components and subsystems that are used to manufacture the products that AT&T studied are available only from Far Eastern suppliers. Faced with a lack of domestic suppliers, AT&T and similar companies have no choice but to buy foreign materials.

Offshore OEMs achieve their advantage in materials costs in the Far East in several ways. Relying on close relationships with local suppliers, offshore manufacturers are regularly able to use techniques such as spot buying to take advantage of

temporary overstocks or bargains. More importantly, despite their integration into a highly internationalized manufacturing environment, they retain significant national/cultural links with materials suppliers. These links translate into preferential treatment when local buyers purchase materials from local suppliers. The relationship between buyer and seller has a significant impact on costs. A U.S. manufacturer like AT&T, when it must buy materials abroad for a lack of alternatives, is at a disadvantage (see Figure 2-2).

To keep its onshore, higher-end telephone manufacturing effort cost competitive, AT&T is attempting to make at least a 10 percent reduction in its materials costs by reaching global material purchasing agreements with its offshore suppliers. Instead of buying materials from a Far Eastern supplier's distributor in the United States, AT&T is negotiating bulk purchases at the supplier factory and assuming the cost and logistics of shipping and distributing the items to its own factories. AT&T sees this initiative as a potentially decisive factor in keeping the onshore manufacture of its higher-end telephones competitive. By making the 10 percent cut in the cost of materials,

Figure 2-2

Cost of purchased material at AT&T and OEMs for the same materials, often from the same supplier, all offshore.

Source: AT&T.

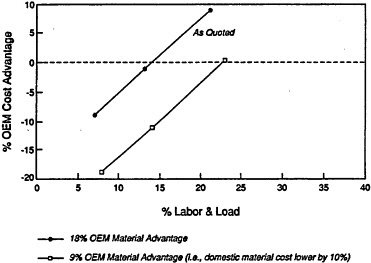

Figure 2-3

Assuming an 84 percent labor/load advantage, labor/load in onshore plants must be under 14 percent to be cost competitive with OEMs with an 18 percent materials cost advantage. By cutting that materials cost differential by 10 percent, onshore production can be competitive when labor/load is up to 23 percent of COGS.

Source: AT&T.

AT&T expects that it can manufacture more of its telephones onshore competitively (see Figure 2-3).

Analysis of Functional Drivers Impacting OEM Costs

Moving production offshore to OEMs incurs costs that need to be quantified and added to an OEM quote when assessing the cost advantage of manufacturing or sourcing abroad. These cost adders include:

-

transportation and duties

-

qualifying OEMs

-

start-up and management costs for OEM vendors

-

quality inspection and management

-

accounting for central expenses (overhead)

-

meeting return-on-investment requirements

-

other carrying cost charges

Taken together, these factors add between 26 and 40 percent to

the OEM product delivery price quoted AT&T. Several of these cost adders are described below.

Transportation and Duties

Transportation costs are relatively fixed and thus are readily identified, but associated duties can vary and have a major impact on loaded costs. Together, they are the largest functional driver, adding 7 to 10 percent to the OEM quote. The key factor driving this expense is the ability to avoid or lessen duties by manufacturing or sourcing products from countries that meet the General System of Preferences (GSP) requirements.

GSP status exempts or reduces the duty on specific products (based on their level of export to the United States) from developing countries that are trying to increase exports. An important consideration is the fact that this major cost factor is a variable one; a country with GSP status one year can lose it the next as a result of unforeseen political or economic changes. A case in point is Singapore, which supplied AT&T with corded and cordless phones under reduced duties until 1990,

Workers assemble cordless telephones at AT&T's plant in Singapore.

Source: AT&T

when the United States revoked its GSP status. There is now an 8.5 percent duty levied on their manufactured cost—a sizeable penalty.

When manufacturing can easily be moved to another country with GSP status, variability in this cost driver is not so detrimental as to preclude offshore manufacture. Low-technology, labor-intensive assembly and manufacturing operations lend themselves to this type of "shuffle" much more easily than high-technology factories that have expensive, not easily transferable skills and equipment.

Quality Management

Ten years ago the cost of quality management in an offshore operation would not have been routinely considered in a decision to move manufacturing overseas. For most American corporations, quality was not a critical issue as long as failure rates were kept to a reasonable level (say one percent).

In a more competitive environment such as the one faced by AT&T today, products of an inferior quality are not tolerated. As other countries have become world-class competitors, offering quality products at reasonable prices, consumer expectations are now higher than they might have been 10 years ago. When purchasing an electronic product such as a telephone, the consumer has more choices because there are more competitors. Manufacturers literally cannot afford to produce low-quality goods that might push consumers to other products.

In a total systems context, quality is free. Whatever upstream costs are incurred in quality improvement are more than offset by lower rework costs, less wasted materials, higher efficiency of work flow, fewer returns, and fewer dissatisfied customers. There are, however, certain up-front costs associated with ensuring quality in an offshore operation.

AT&T's study found that the cost of quality management for an OEM operation added 1.9 to 6.2 percent to the quoted product price. The added costs come from several sources. First, start-up activities to qualify an OEM include comprehensive audits of vendor manufacturing and management systems, along with initial inspection of vendor output until full-stream

production is achieved. Vendor qualification, lot-by-lot inspections, and process improvement also are standard expenses. (These costs are incurred onshore as well and are part of the reason AT&T's onshore load costs are higher.) There is also the need to intensify quality management efforts as a product becomes more sophisticated, when there are quality failures (reinspection/requalification), or as quality standards become more rigorous.

Make to Order

Responsiveness to customer demand is one of the key advantages companies can use to succeed in a highly competitive global environment. Onshore manufacturing is attractive in this respect because, even when an OEM is quickly able to build to a customer's specific order, ocean transport is an unavoidable delay. Because availability is a major issue in a consumer market, firms facing potential bottlenecks in the pipeline from their offshore suppliers must carry additional inventories. The cost of carrying such inventories must be figured into the total cost of offshore sourcing when a firm competes in a make-to-order environment.

Because practically all of AT&T's parts and components suppliers are located in the Far East, AT&T has had to develop a direct pipeline from Asian supplier factories to its domestic plants. The relatively small size and weight of electronic components make them air freightable, and, with well-coordinated trucking and ordering systems, AT&T is able to achieve a six-day turnaround (from order to delivery) on Asian parts destined for its onshore manufacturing plants. When products are made to order onshore with Asian components, additional inventory carrying charges are avoided. If the end product is made in Asia, however, an average of 4 percent additional inventory carrying cost is incurred.

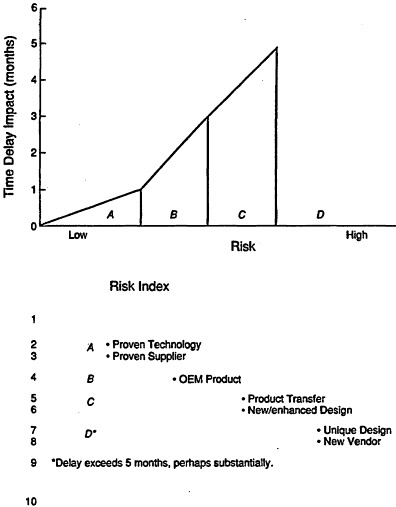

Unquantified Risks

AT&T also studied risk factors incurred in doing business with an offshore OEM, including environmental exposure and the inadvertent transfer of strategic information to suppliers, and concluded that while such factors needed to be considered

they were not major cost drivers. One exception, however, is the possibility that lags in OEM production may adversely affect product realization targets.

AT&T's product realization strategy focuses on time to market—that is, the time it takes for a product to move from conception to general availability. This factor, while difficult to quantify, is vital to AT&T's competitiveness and so is included in its analysis of the potential costs of locating offshore.

AT&T's experience with its onshore plants and OEMs indicates that site impact on time to market is a real concern, even though it is difficult to assign a direct dollar value to it. In a study that tracked both company-owned and OEM facilities producing nearly 60 products between them during 1986-1988, AT&T facilities met target production deadlines nearly twice as frequently as OEMs. Factors contributing to the OEMs' poor track record included continued AT&T technical changes during product ramp-up, OEM component supplier problems, and cultural and language barriers.

Managing time to market involves considering the potential risks (i.e., costs) of time delays on product development, manufacture, and delivery. The risks tend to be low with proven technologies and proven suppliers. The risk increases, however, when AT&T must deal with new designs and new suppliers. The relative risk of delay for various attributes of product and producer is illustrated in Figure 2-4.

Summary Observations: AT&T Cost Analysis

The AT&T study of COGS comparing onshore and offshore production prompts the following observations:

-

Although offshore manufacturing has inherent cost advantages, their relative importance has changed over time. The factor with the greatest leverage on total COGS—materials—is also the factor with the least offshore advantage.

-

It is most difficult to overcome offshore cost advantages for low-technology, labor-intensive products. Included are products that will remain above cost parity even after onshore cost initiatives like global component purchasing are implemented—potentially any product that costs less than $50 for fully loaded manufacture.

Figure 2-4

Time-to-market impact, relative risk in meeting commitments.

Source: AT&T.

-

Material cost reduction programs are key to reducing COGS. Although AT&T's study concentrated on telephones, the same principle holds for many other electronic products.

-

Cost adders for offshore manufacturing can become significant if not actively managed (e.g., quality).

-

Onshore cost reduction programs need to be aggressively pursued with specific targets if domestic operations are to

Worker inspects color picture tube at Toshiba Display Devices.

Source: Toshiba.

-

approach parity with offshore operations. Highlighted AT&T programs include global component purchasing and continuous load reduction.

-

Factory value-added initiatives such as make to order can provide a differential competitive advantage in comparison with competitors and offshore manufacturing.

-

Effectively benchmarking onshore operations against offshore analogs is a means of assessing where improvements could be made in onshore operations. Further, it delineates the limits of improvement and spurs managers to think about alternative ways to lower costs and be competitive.

THE TOSHIBA EXPERIENCE4

Background

Toshiba began building color picture tubes (CPTs) in New York in a joint venture with Westinghouse in 1985. Toshiba Display Devices (TDD) employs 1280 people in its New York

operation, 850 of whom are direct laborers. Two years after the venture began production, Westinghouse sold its part of the venture because the market for CPTs was not growing as quickly as initially expected. TDD is now a wholly owned subsidiary of Toshiba.

A first-order consideration for Toshiba when it was approached by Westinghouse was market access. After a petition was filed against Japanese television makers by the Electronics Industry Association in 1971, Japanese firms such as Toshiba began to establish television assembly plants in the United States. The demand in the United States for televisions is approximately 20 million sets per year, despite the fact that 98 percent of all households have at least one set. Demand is expected to grow by approximately 1 to 2 percent per year.

Cost of Materials

Regardless of manufacturing location, the most significant cost component in CPT production is materials. Table 2-3 illustrates the major costs, comparing Toshiba's plant in Himeji, Japan, with one in Thailand in 1990. Of the 70 percent or so of total costs accounted for by materials, about 40 percent is glass.5 Because glass is both heavy and fragile, it tends to be purchased locally to avoid shipping costs; therefore, the cost of glass is a major determinant of the relative cost of CPT production in different locations.

As a proportion of total costs, Toshiba pays less for glass in the United States than it does in either Thailand or Japan, pri-

TABLE 2-3

Thirteen-inch CPT Manufacturing Cost Comparison: Himeji vs. Thailanda

|

|

Himeji |

|

Thailand |

|

|

Cost of materials |

689 |

(68.9%) |

704 |

(72.8%) |

|

Direct labor |

74 |

(7.4%) |

20 |

(2.0%) |

|

Factory overhead |

237 |

(23.7%) |

243 |

(25.2%) |

|

Total |

1,000 |

(100.0%) |

967 |

(100.0%) |

|

a Indexed to 1000. |

||||

marily because of the relative capability of local suppliers. Production yields on the high-quality glass demanded for CPTs vary substantially by supplier, ranging from about 40 to 65 percent. Toshiba's American suppliers, benefiting from both superior process control capabilities and product technology transferred from Toshiba's supplier in Japan, achieve yields at the high end of this range, providing cost advantages to Toshiba's American plant. With this as a major factor, it is worth noting that an estimated 90 percent of TDD's required materials were sourced from U.S. suppliers in 1990, and a plan is in place to raise that to 100 percent within the next few years.

Labor Costs

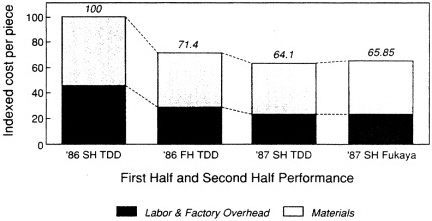

Although direct labor is far less than 10 percent of CPT production costs, and therefore is not a major driver in location decisions, the rate at which workers learn their jobs and improve productivity has an important impact on how quickly a plant becomes competitive. Figure 2-5 illustrates this learning curve effect in comparing the manufacturing costs of TDD about one year after start-up and of Toshiba's plant in Fukaya, Japan. The figure shows both the U.S. advantage in the cost of

Figure 2-5

Nineteen-inch CPT manufacturing costs, TDD versus Fukaya (Japan).

Source: Toshiba (1986).

TABLE 2-4

Comparison of Labor Costs, Toshiba Japan vs. TDD, 1989a

materials and the significant drop in labor cost and factory overhead, allowing TDD to undercut Fukaya slightly in overall costs.

Table 2-4 provides a more detailed look at labor costs in the two locations. The main lesson here is the importance of exchange rates in determining relative labor costs. At the prevailing rate of 125 yen per dollar, American wages are less than half those in Japan; even with higher American benefit rates, labor costs about half ($9.60 vs. $18.60) in the United States. Consequently, despite the 9 percent disadvantage in productivity, total direct labor costs per piece are substantially lower at TDD. By comparison, U.S. and Japanese wage and benefits costs would be equal at an exchange rate of 242 yen per dollar, giving the Japanese plant a slight labor cost advantage on the basis of higher productivity at that rate.

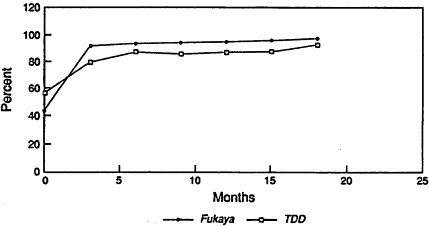

What accounts for this productivity difference? The machinery and equipment for CPT production at TDD is virtually identical to that used by Toshiba in Japan. Yet despite the similarities, a comparison of yield in both plants (Figure 2-6) reveals that TDD achieved yields of 90 percent in the same time it took Toshiba Japan to reach 93 to 95 percent.6

The difference in yields can partly be attributed to differences in personnel experience and turnover rates. Almost all of the Toshiba personnel in Japan had approximately 15 years of experience, whereas those in America had none. The training of key TDD personnel was conducted in Japan, which also

Figure 2-6

Comparison of yield ratio (from start of operation).

Source: Toshiba.

accounts for the lag in the rate of yield increase. Furthermore, monthly employee turnover at TDD was 4.7 percent in 1987, declining to 2.7 percent in 1988 and 2.3 percent in 1989, but still higher than the Japanese rate of under 2 percent. These factors notwithstanding, however, Toshiba has found that—compared to American and German workers—the yields achieved by Japanese workers are typically higher.

Capital Budgeting

An initial investment of $220 million was required to begin production at TDD. The cost of that initial outlay was de-frayed slightly by low-interest financing offered by the U.S. government and the state of New York.

When automated production was introduced in CPT manufacturing in 1980, continued participation required large equipment investments. In the first five years following the plant's opening, TDD spent approximately $187 million on fixed assets such as machinery, equipment, and facilities. Of that amount, almost $150 million was for manufacturing equipment, $75 million of which was procured from Toshiba Japan.

Toshiba believes that the return on this investment is about

5 percent, significantly lower than the 15 to 20 percent return that U.S. companies often expect on new investments. Toshiba's willingness to accept a 5 percent return reflects its consideration of the strategic value of having significant CPT production in the United States, gaining experience working with U.S. suppliers and an American work force, and having more timely access to technological developments in the United States.

Summary Observations: Toshiba Color Picture Tube Manufacturing

Toshiba's experience manufacturing CPTs in the United States prompts the following observations:

-

The primary consideration in Toshiba's decision to locate in the United States was market access.

-

Labor is less expensive in the United States than in Japan at recent exchange rates, but it is such a small component of production costs that it has only a small impact on the relative cost competitiveness of Toshiba's plants worldwide.

-

Parts and materials are primarily procured in the United States. Extensive cooperation with its U.S. glass suppliers, including transfer from Japan of product technology, coupled with high-quality, high-yield glass supplies, has provided an important materials cost advantage to TDD.

-

Despite rapid improvement, the learning curve for TDD was not as steep as a comparable Japanese plant due to higher employee turnover and a less experienced work force.

-

Although the initial motivation for Toshiba's investment in American production facilities was to ensure continued market access in the face of protectionist pressures, TDD proved to be a low-cost producer once initial start-up difficulties were overcome. The United States effectively provides a favorable manufacturing environment for this product.

CONCLUSIONS

Of the three major factors in site location consideration—access to markets, access to technologies/capabilities, and access to low-cost—the first was most significant in Toshiba's

site selection and the last in AT&T's case. The experiences of AT&T and Toshiba attest to the importance of access to both low-cost and markets, although clearly each firm had different motives and competitive requirements.

AT&T, for example, began manufacturing abroad or outsourcing to foreign OEMs because of cost advantages and the immediate difficulty of raising its onshore facilities to world-class Standards. Finding ways of manufacturing products at low-cost became essential when AT&T made the decision to move offshore in 1984: the market was changing from one that was partly regulated to one that was fully competitive, profitability projections were unacceptable, and AT&T's revenue stream was in decline. Becoming competitive was not a matter of gaining access to the market, but rather of becoming competitive in price while maintaining quality and timely product development.

A different set of circumstances shaped Toshiba's decision to locate a plant in the United States. Unlike AT&T, Toshiba was primarily concerned with market access; its domestic facilities were already working at world-class levels. By manufacturing in the United States, Toshiba could increase the local content of the products it was selling in the United States, thereby assuaging American discontent with the dominance of Japanese imported consumer electronics goods. Further, through a combination of a strengthening yen and capable American suppliers, total manufacturing costs actually have been lower in the United States than in Japan in recent years.

Both these decisions illustrate some of the general principles that affect site decisions within this industry. Among them:

-

With respect to low-cost, low-technology consumer electronics products, firms must reduce costs to be competitive. For a manufacturer such as AT&T that produces products requiring materials predominantly available in Asia, the United States is not as attractive a manufacturing location. Instead, these products will likely be produced in areas where labor and materials are comparatively inexpensive.

-

When market access is granted on the basis of local content and/or local presence, manufacturing decisions become

-

very “site sensitive.” Because the United States is host to a large and steadily growing market for television sets, it attracts manufacturers like Toshiba who might otherwise be unable to serve this market from a distance.

-

External factors such as exchange rate differentials have a major impact on relative production costs in globally scattered facilities.

-

Managers in Asian supplier plants place a high priority on yield improvement, often assigning large numbers of engineers to the problem.

-

Greenfielding is not simply a method for lowering labor costs onshore. Management is often greenfielded in an attempt to eliminate outdated ways of manufacturing. Similar improvements in manufacturing practice may be expected when moving manufacturing offshore (i.e., changing manufacturing "cultures").

-

Managing quality at a distance (in, say, Asian plants) is costly and difficult. Considering the consequences of quality lapses, the potential costs of both ensuring and failing to achieve adequate quality must be weighed in location decisions. Further, Asian or even Japanese manufacturers are not the exclusive practitioners of effective quality management. In some cases, U.S. firms know more about quality production than their offshore OEMs and suppliers. These variations in quality competencies need to be factored into location decisions as well.

-

Time to market is often a critical factor in the success of a product. Time to market also impacts production costs. Speeding progress through the product realization process is another way of overcoming onshore/offshore cost differentials.