11

Methods and Analysis of Study Projections

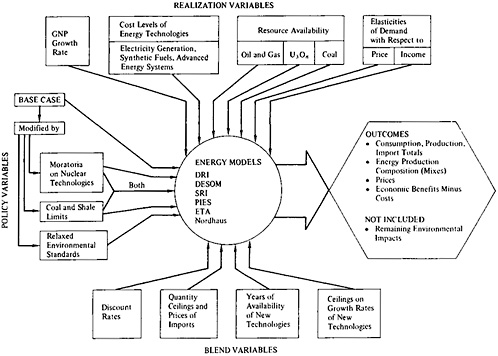

CONAES asked several of its panels to develop models of energy and the economy to make plain the interrelations among variables influencing the supply of and demand for the various forms of energy. These models were applied to sets of assumptions about, for example, the growth rate of the economy, changing prices for energy over the next three decades, and consumer response, to picture some plausible states of affairs in the year 2010 and the course of their development. Some of the resulting scenarios are described here to illustrate key interrelations and assumptions.

There is always the danger in presenting models that numerical results will be taken literally. CONAES emphasizes that many uncertain assumptions must be made to construct models, and a great deal must be simplified or left out of consideration. Judgment alone decides whether some factors are important and whether others can be safely neglected, at least in a first approximation. Models cannot predict the future, but simply represent statements contingent on the consequences of assumptions and public policies. Nor can the consequences be regarded as rigorously deduced conclusions from a set of explicitly stated assumptions. Many detailed judgments accompany reason in these cases, judgments about the costs of new technologies, the rate of future resource discoveries, or the likely responses of myriads of producers and consumers to the general political climate and to government regulation. Many of the assumptions themselves are the subjects of wide disagreement among experts. For example, the Demand and Conservation Panel assumed an annual average growth rate for the gross national product (GNP) of 2 percent between 1975 and 2010, and defended this as their assessment of the most probable

rate of future economic growth, but most of the economists involved in this study find it implausibly low. All the scenarios are “surprise free” in the sense that they ignore discontinuities such as embargoes, revolutions, natural disasters, international conflicts, and domestic strikes.

The value of models lies in the following.

-

They allow “thought experiments” to be conducted on the likely consequences of specific policies such as supply constraints, energy taxes, mandatory efficiency standards, or price regulation.

-

They allow testing of the sensitivity of outcomes (such as the rate of growth in energy consumption, or the relative consumption of various fuels) to varying input assumptions (such as economic growth rates, prices, population, work-force participation, or life-style preferences).

-

They provide an accounting device that helps ensure internal consistency among the projections.

-

They depict qualitative relations among the various factors affecting energy supply and demand. It is important to caution that the models do not usually prove qualitative statements, but rather illustrate them schematically.

CONAES has employed three different kinds of scenarios, each designed to answer different kinds of questions. The Modeling Resource Group (MRG)1 employed econometric models to estimate the consequences of various economic and policy assumptions for total energy consumption. These are equilibrium models in which prices are determined endogenously through the interaction of supply and demand schedules for energy resources (using optimization techniques that simulate a competitive market). The MRG investigated the effect on GNP of various policies and levels of energy consumption, modifying supply and demand schedules for such hypothetical possibilities as high or low discovery rates for resources and Btu taxes (i.e., taxes per Btu of primary energy input). The group used econometric models to compute the total net cost to the economy of limitations on various energy supply technologies (e.g., on the expansion of nuclear power, the development of oil shale resources, or the mining of coal). The work of the MRG was largely self-contained, as reported in detail in their report, and has not been used in the other models, although some comparisons between the MRG results and those of the other models are presented in this chapter.

The Demand and Conservation Panel focused on the demand for net energy delivered to the point of consumption (final demand), separated by different energy forms (i.e., electricity, gaseous fuels, liquid fuels, and coal). In the Demand and Conservation Panel’s models, energy prices are exogenous and are assumed to increase at various rates between 1975 and

2010. The effects of prices on the final demand for each energy form were estimated by a combination of econometric and technological models, as explained in greater detail below. Different technological models were used for each end-use sector (buildings, transportation, and industry). Specifically, the optimum design for energy-consuming equipment was chosen for each price scenario in such a way that the discounted lifetime cost of each piece of equipment is minimized over time for that particular price assumption, taking into account the normal replacement rate for the equipment, Little or no technological innovation was assumed, other than the application of well-known engineering principles.

Having obtained a set of final energy demands for each form of energy, the Demand and Conservation Panel then estimated the primary fuel requirement needed for conversion to the final fuel form, taking into account conversion efficiency and transportation or transmission losses, as well as processing losses. In the case of synthetic liquids and gases derived from coal, the partition between natural and synthetic fuels was estimated crudely on the basis of judgments by industry consultants about the availability of the synthetics technologies. Initial estimates were corrected in a second iteration by negotiation between the Demand and Conservation Panel and the Supply and Delivery Panel.

It had been hoped that the Supply and Delivery Panel would be able to generate supply curves for each primary fuel, i.e., curves of available supply as a function of price and time. This did not prove feasible. In the opinion of the panel, the political climate for energy resource development is a more influential factor than price in determining investment in energy exploration and development and, thus, future supplies. Price was included in the definition of political climate, but was not the most important factor. The Supply and Delivery Panel expressed the opinion that the energy required for any of the Demand and Conservation Panel’s scenarios could be produced for little more than twice the 1975 OPEC price (measured in 1975 dollars), and that much higher prices than this to producers would not bring forth large additional domestic supplies. Not all experts would agree to this assumption. For example, some believe that large unconventional natural gas supplies would be forthcoming at sufficiently high prices.2

The Supply and Delivery Panel projected three different “climate” scenarios: business as usual, enhanced supply, and national commitment The scenario for each primary energy source was defined somewhat differently, according to the source’s characteristics. For each scenario, the panel estimated the amount of each form of primary energy likely to be produced in 1990 and in 2010 under the corresponding assumptions.

The next step for CONAES was to try to match the Supply and Delivery Panel’s supply projections with the Demand and Conservation Panel’s

TABLE 11–1 Scenario Projections Used in the CONAES Study

|

Scenario |

Source |

Description |

|

Demand scenariosa: A*, A, B, B′, C, D |

Demand and Conservation Panelb |

A, B, C, and D explore the effects of varied schedules of prices for energy at the point of use, from an average quadrupling between 1975 and 2010 (scenario A) to a case (scenario D) in which the average price of energy falls to two thirds of its 1975 value by 2010. Basic assumptions include 2 percent annual average growth in GNP, and population growth to 280 million in the United States in 2010. Scenario A* is a variant of A that takes additional conservation measures into account. Scenario B′ is a variant of B, projecting the effect on energy consumption of a higher annual average rate of growth in GNP (3 percent). |

|

Supply scenarios: Business as usual, enhanced supply, and national commitment |

Supply and Delivery Panelc |

Projections of energy resource and power production under various sets of assumed policy and regulatory conditions. Business-as-usual projections assume continuation without change of the policies and regulations prevailing in 1975; enhanced-supply and national-commitment projections assume policies and regulatory practices to encourage energy resource and power production. |

|

Study scenarios: I2, I3, II2, II3, III2, III3, IV2, IV3 (correspondence between study scenarios and demand scenarios: I2=A*, II2=A, III2=B, III3=B′, IV2=C; scenario D was not used) |

Staff of the CONAES study |

Based on the demand scenarios; integrations of the projections of demand from the demand scenarios and projections of supply from the supply scenarios. A variant of each price-schedule scenario was projected for 3 percent annual average growth of GNP. |

|

MRG scenarios |

Modeling Resourced Group |

Estimates of the economic costs of limiting or proscribing energy technologies in accordance with various policies. |

estimated requirements for final energy. This was accomplished by carrying forward the process initiated by these two panels (and consulting with them as necessary): starting with the scenarios of demand (and a variant for each at 3 percent annual average growth of GNP), estimating the mix of primary fuels likely to meet those requirements (taking into account conversion and transmission losses), then readjusting the requirements to bring the assumed supply policies into line with the political climate likely to accompany the corresponding scenario of demand. For example, the prices and policies leading to projections of greatly moderated demand for energy would most likely correspond to policies that constitute business as usual for supply. The assumptions leading to higher projections of demand would most likely correspond to the conditions for enhanced supply.

Thus, the demand called for by a scenario of low energy consumption was initially matched with a business-as-usual supply scenario. If this did not provide enough energy to meet demand, the enhanced-supply scenario was tried. For the scenarios of high energy consumption, some national-commitment supply scenarios were permitted. The study scenarios do not employ exactly the same fuel mixes as the Demand and Conservation Panel’s scenarios to fill the required end-use demands. This results in slightly different primary energy requirements because of the differences in assumed energy-conversion efficiencies. Small differences, usually not more than 10 percent, may be observed between the primary energy inputs (total energy consumption) in the study scenarios and the scenarios computed by the Demand and Conservation Panel.

In the following sections, we describe the assumptions and methods of the Demand and Conservation Panel and the Supply and Delivery Panel, and we present the comparisons of supply and demand incorporated in the study scenarios. This is followed by a separate discussion of the scenarios of the MRG and by a comparison of the results of the MRG with the study

scenarios. Table 11–1 summarizes the scenarios discussed in this chapter for ready reference.

ANALYSIS AND SCENARIOS

WORK OF THE DEMAND AND CONSERVATION PANEL3

The work of the Demand and Conservation Panel relied primarily on assessments of the technological possibilities for moderating the consumption of energy in the transportation, buildings, and industrial sectors of the economy. The panel projected the extent to which these technological possibilities might be realized under various assumed sets of prices for energy at the point of use. An integrating model for the economy in the year 2010 was used to adjust these sectoral figures for consistency with one another and with final demand. The levels of energy consumption projected by the panel for 2010 range from about half today’s per capita consumption to levels twice as high.

In projecting the consumption of energy over the next three decades, the panel chose to fix some demand-shaping variables and to allow others to vary. It was most interested in the effects of changing prices for energy and various policies that would stimulate or discourage energy-conserving practices. Accordingly, the panel fixed the growth rate of GNP (experimenting, however, with a variant), population, and work-force participation, and its scenarios of energy consumption were determined by response to four sets of energy prices. The panel assumed that the decisions of consumers (both industrial and commercial) on the purchase of energyconsuming equipment would be economically rational for each assumed set of prices, and that consumers would seek to minimize the total lifetime cost of such equipment. Policy variables were also simulated in two additional scenarios to test the effects of vigorous conservation accompanied by some voluntary changes in patterns of living, working, and buying (in one case), and a higher rate of economic growth (in the other).

Population Growth

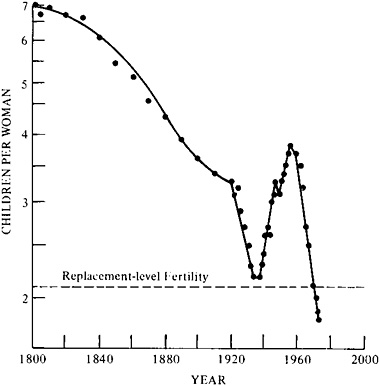

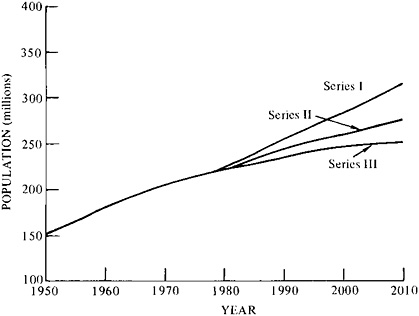

The panel assumed the Series II projection of population growth by the Bureau of the Census in all scenarios. This projection assumes a reversal of the downward trend in fertility (Figure 11–1), resulting in a population of 279 million people in the United States in 2010. The Series III projection, assuming a continued downward trend in fertility, gives a population of 250 million people in 2010. If the Series III projection were realized, the panel estimates that total energy consumption in 2010 would be lower by

about 10 percent in all the scenarios. (Series I, II, and III projections by the Bureau of the Census are pictured in Figure 11–2.)

Any assumption of future population growth must be considered arbitrary. The panel points out that the effects of illegal immigration can only be guessed, although they could well be the most significant source of demographic uncertainty.

Work-Force Participation and Other Trends

The panel assumed that the work force in the United States would grow in the direction indicated by prevailing trends: at a lower rate in the future than in the past, and in accordance with recently declining fertility rates and the consequent size of younger-age cohorts, which govern the rate of growth of the labor force. The panel also assumed that the participation of women in the work force would continue to grow. The trend toward shorter working days and fewer working days per year was presumed to extend into the future at about the same rate as in the recent past.

Growth of GNP

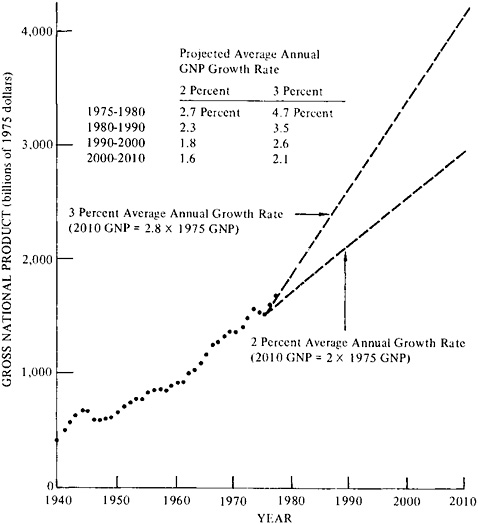

Gross national product was used in this study as a measure of economic activity, and in an extended (if not wholly satisfactory) sense as an indicator of national well-being, Over the 30-yr period from 1945 to 1975, GNP grew at an average annual rate of 2.7 percent.* The rate of increase from year to year varied (from 1950 to 1970, the average annual rate was 3.5 percent). The panel assumed that over the next 30 years, the growth of GNP would be rapid in the near term, owing in part to recovery from the 1974 recession and in part to the rapid growth of the labor force in the 1970s stemming from the postwar baby boom. Beginning in the mid-1980s, growth would slow with declining additions to the labor force. The panel selected an average annual growth rate for GNP of 2 percent over the next 30 years.† At this rate, GNP approximately doubles by 2010. One scenario was projected for an annual average growth rate of 3 percent, resulting in a near tripling of GNP (2.8 times the 1975 total) by 2010 (scenario B′). Figure 11–3

FIGURE 11–1 Total estimated fertility rates in the United States from 1800 to 1976. Source: U.S. Department of Commerce, Bureau of the Census, Estimates of the Population of the United States and Components of Change: 1940–1976, Population Estimates and Projections Series P-25, No. 706 (Washington, D.C.: U.S. Government Printing Office, 1977).

illustrates the two paths, which are approximately linear rather than exponential,‡ and the inset shows the corresponding compound growth rates used by the panel for the subperiods from 1975 to 2010.

The rate of economic growth selected by the panel prompted discussion within the committee and among other participants in the study. Most of the economists express reservations about its likelihood, feeling that a 2 percent average rate of growth would not be consistent with the assumption of full employment. Others point to recent trends of declining growth in productivity and suggest that the growing investment in environmental protection and related areas of health and safety, as well as the shift of employment from the manufacturing to the service sector, will continue to reinforce the trend of declining growth in productivity.

FIGURE 11–2 Estimates and projections of the total population of the United States from 1950 to 2010, showing Bureau of the Census alternative projections from 1975. Source: Adapted from U.S. Department of Commerce, Bureau of the Census, Estimates of the Population of the United States and Components of Change: 1940–1976. Population Estimates and Projections Series P-25, No. 706 (Washington, D.C.: U.S. Government Printing Office, 1977).

The Modeling Resource Group used an average annual rate of growth for GNP of 3.2 percent/yr as their base case, but also showed an alternative low value, corresponding to an average of about 2 percent a year, with even greater deceleration.

|

|

D/C Panel |

MRG-Low |

|

1975–1980 |

2.7 |

3.7 |

|

1980–1990 |

2.3 |

2.7 |

|

1990–2000 |

1.8 |

1.2 |

|

2000–2010 |

1.6 |

0.5 |

The Modeling Resource Group generated its high, low, and base-case projections for the growth of GNP by projecting the changes that might be expected in three determinants of potential GNP over the period 1975–2010. Those leading to the lower rate of growth are the following.

-

Work-force participation declining from 0.73 (its average value from 1950 to 1975) to 0.70 in 2010.

-

Unemployment averaging 6 percent.

FIGURE 11–3 Past and projected GNP growth in the United States from 1940 to 2010 (billions of 1975 dollars). Source: Adapted from National Research Council, Alternative Energy Demand Futures to 2010, Committee on Nuclear and Alternative Energy Systems, Demand and Conservation Panel (Washington, D.C.: National Academy of Sciences, 1979), p. 60.

-

Growth in productivity shrinking from 1.57 percent per annum in 1975 to zero by 2010.

-

Growth rate of the potential labor force and immigration slowing to 0.2 percent a year after 2010.

Other studies examining the relation of energy consumption and the domestic economy have projected different rates of growth for GNP. The

Energy Policy Project of the Ford Foundation,4 for example, projected three scenarios to the year 2000 (in 1974). In that study, the zero-energy-growth and technical-fix scenarios assumed that GNP would rise at a rate of 3.5 percent/yr from 1975 to 1985, and at a rate of 3.1 percent/yr from 1985 to 2000. The historical-growth scenario assumed that GNP would rise at a rate of 3.6 percent/yr over the first 10-yr period, and at a rate of 3.3 percent/yr from 1985 to 2000. Exxon Corporation5 assumed that GNP would grow over the 4-yr period from 1976 to 1980 at an annual rate of 4.2 percent, and from 1980 to 1990 at an annual rate of 3.4 percent, but warns, “A reasonable range of error in estimating long-term economic growth might be perhaps ±0.5 percent per year.” The Edison Electric Institute6 set out three patterns of economic growth to the year 2010—high, moderate, and low. The high-growth case has GNP rising by 4.2 percent/yr; the moderate case, by 3.5–3.7 percent/yr; and the low case, by 2.3 percent/yr. The institute considers the moderate case to be the most likely. (Table 11–34 gives the annual average GNP growth rates projected by CONAES and other energy studies.)

CONAES did not attempt to select a “best” growth rate, but rather estimated the growth of energy consumption for both 2 percent and 3 percent growth rates in GNP from 1975 to 2010. It is important to recognize that several other estimates are higher than this range and would lead to higher energy consumption for a given set of price assumptions. The scenarios of the Demand and Conservation Panel cannot be regarded as bracketing all the possibilities.

Energy Prices

As recapitulated below, the demand scenarios (presented in chapter 2) assume energy prices held constant (scenario C), doubled (B and B′), or quadrupled (A and A*) by 2010. These are average prices of net delivered energy. The panel assumed specific prices for each source of energy by 2010, displayed in Table 11–2, under the categories of these average prices. The relative prices given in Table 11–2 were intended to reflect approximate parity in dollars per million Btu, with adjustments for the relative cleanliness, convenience, and thermodynamic qualities of fuel. Natural gas is thus priced above distillates, and coal below petroleum. Deregulation of prices was assumed in these projections. Unless otherwise specified, the panel’s overall assumption was that demand would be met at these prices. (Scenarios A* and A, for example, specify a prohibition against the use of natural gas for industrial boilers.)

The assumed prices listed in Table 11–2 for the year 2010 represent those seen by consumers at the final stage of end-use, expressed in 1975 dollars. The relative increase is the same for all consumers, industrial and

residential, and for each end-use. This assumption may overestimate the prices that would be charged for energy consumed in homes and in transportation relative to the prices charged for industrial consumption. It implies that distribution and overhead costs will rise in proportion to primary fuel prices. From 1970 to 1978, in fact, the average costs of primary fuels doubled, but the average prices of delivered energy rose just 30 percent in real dollars.7 Assuming that overhead, distribution, and capital costs remain constant (in constant dollars) while primary fuel costs increase enough to keep average delivered prices the same, a relative shift in demand would occur from industry to households and transportation and from fluid fuels to electricity. The assumed rises in primary fuel prices would have to be more than double the ratios shown in the table. Some trend of this sort is already indicated in the detailed price assumptions. Prices for electricity (with the largest capital and distribution cost) rise least, while prices for natural gas (with the lowest capital and distribution costs) rise most

Other Assumptions

Scenarios A, B, B′, and C assume that the structure of the economy will not change markedly over the next three decades. The energy-price/demand extrapolations employed by the panel are consistent with historical data for fuel-price demand elasticities and cross-elasticities, and with regional comparisons. Details are given in the report of the Demand and Conservation Panel.8

Scenario A*, a simple variant of scenario A, tests the additional moderation in the growth of energy consumption that might result from some changes in the habits and purchases of consumers and from an accelerated shift in the economy from goods to services (for example, from goods produced to be used once and discarded to goods produced to endure with much more repair and maintenance). Again, this scenario might be criticized on the grounds that high labor costs would make repairs uneconomical. On the other hand, it is possible that advances in information technology and microprocessors could greatly increase the productivity of repair services, as well as making possible better quality control and durability in original manufacture (for example, by replacing low-reliability mechanical devices with electronics of higher reliability). Such developments could shift the optimum balance between initial product cost and repair.

TABLE 11–2 Price Assumptions for Scenarios of Energy Demanda

|

|

Oil Prices |

|||||

|

Distillate No. 2b |

Utility Residual |

Gasoline Before Taxes |

||||

|

Dollars per Barrel |

Dollars per Million Btu |

Dollars per Barrel |

Dollars per Million Btu |

Dollars per Barrel |

Dollars per Million Btu |

|

|

1975 actual |

16.37 |

2.81 |

12.40 |

2.02 |

19.08 |

3.64 |

|

2010 scenarios |

|

|

|

|

|

|

|

A, A* |

78.58 |

13.49 |

59.52 |

9.70 |

91.58 |

17.47 |

|

B, B′ |

39.29 |

6.74 |

29.76 |

4.85 |

45.79 |

8.74 |

|

C |

16.37 |

2.81 |

12.40 |

2.02 |

19.08 |

3.64 |

|

Ratios of 2010 prices to 1975 prices |

|

|

|

|

|

|

|

A, A* |

|

4.8 |

|

4.8 |

|

4.8 |

|

B, B′ |

|

2.4 |

|

2.4 |

|

2.4 |

|

C |

|

1.0 |

|

1.0 |

|

1.0 |

|

|

Utility Natural Gas Prices (dollars per million Btu) |

Utility Coalc |

|||||

|

Utilityd |

Residential |

Commercial |

Industriald |

Consumption Weighted Average |

Dollars per Ton |

Dollars per Million Btu |

|

|

1975 actual |

0.75 |

1.70 |

1.41 |

0.99 |

1.29 |

17.68 |

0.81 |

|

2010 scenarios |

|

|

|

|

|

|

|

|

A, A* |

? |

19.63 |

15.89 |

11.38 |

14.84 |

70.52 |

3.24 |

|

B, B′ |

? |

9.82 |

7.94 |

5.69 |

7.42 |

35.26 |

1.62 |

|

C |

? |

4.09 |

3.31 |

2.37 |

3.09 |

17.63 |

0.81 |

|

Ratios of 2010 prices to 1975 prices |

|

|

|

|

|

|

|

|

A, A* |

|

|

|

|

11.5 |

|

4.0 |

|

B, B′ |

|

|

|

|

5.7 |

|

2.0 |

|

C |

|

|

|

|

2.4 |

|

1.0 |

Methodology

The panel investigated the consumption of energy in each of the three principal energy-consuming sectors of the economy—buildings, transportation, and industry—and projected the consumption of energy in these sectors to 2010 under the assumptions of the five scenarios. This sectoral analysis yielded interesting information about energy-efficient technologies and patterns of energy use available for the future, but it did not allow for feedback and other interactions among the sectors. The integrating model was designed to trace the flow of energy through the national economy in 2010, adjusting the energy consumption figures for the three sectors so as to be self-consistent. The energy demand totals for 2010 given here and in chapter 2 were calculated with the aid of the integrating model.

The three sectoral analyses employed different methods, briefly summarized below.

Buildings9 Residential buildings were defined as those occupied by households, and nonresidential buildings as those occupied by the service sectors of the economy. In the residential sector, energy was assumed to be used for space heating, water heating, air conditioning, the preparation and storage of food, lighting, laundry, and the operation of small appliances. In the nonresidential sector, energy was assumed to be used for heating, cooling, and operations such as cleaning and powering elevators.10

An existing engineering-economic simulation model was used to evaluate the effects of rising personal incomes and fuel prices on the cost and use of energy in residential buildings. The model is explained in the report of the Demand and Conservation Panel.11 The panel used this model to simulate the use of four fuels (gas, oil, electricity, and other) for eight functions (space heating, water heating, refrigeration, food freezing, cooking, air conditioning, lighting, and other) in three types of residential buildings (single family, multifamily, and mobile homes). The fuel consumed for each end-use was estimated in response to changes in stocks of occupied housing units and new residential construction, equipment ownership by fuel and end-use, thermal integrity of new and existing housing units, average unit energy requirements for each type of equipment, and aspects of household behavior reflected in patterns of use.

The economic submodels provided the elasticities that determine the responsiveness of households to changes in economic variables (incomes, fuel prices, and equipment prices). The elasticities were calculated for each of the three major household fuels and each of the eight end uses, each fuel price and income elasticity being separated into two elements—the elasticity of equipment ownership and the elasticity of equipment use. The

first gave changes in market shares of equipment ownership in response to changes in fuel prices and incomes; the second gave changes in equipment use with ownership held constant. The submodels also provided equipment-ownership, market-share elasticities with respect to equipment costs. The simulation model was therefore able to estimate consumer responses to changes in operating costs (fuel price times consumption) and changes in capital costs.

The engineering submodels were used to evaluate the variations of purchase prices and energy use with the design of equipment. Detailed submodels were constructed for gas and electric water heaters, refrigerators, and ranges; for the other end-uses, data were combined from various sources to determine relations between energy use and initial cost.

With the simulation model, it was possible to combine the outputs from the various submodels with the initial conditions (from 1970) and the boundary conditions (including policy variables) for the scenario period. The four fuels (i), eight end-uses (k), and three housing types (m) produced 96 fuel-use components (Qi,k,m) for each year (t) of the simulation model. The model also provided annual fuel expenditures, equipment costs, and capital costs for improving the thermal integrity of new and existing structures.

Energy use in the nonresidential subsector was projected by a disaggregated model of the commercial demand for energy12,13 that covered five end-uses (space heating, water heating, cooling, lighting, and other), four fuel types (gas, electricity, oil, and other) and ten commercial subsectors (retail/wholesale, auto repair/garages, office activities, warehouse activities, public administration, education, health care, religious services, hotels/motels, and miscellaneous).

The modeling approach was traditional. The demand for energy, given fuel i, end-use k, and subsector or building type m, was represented simply as

where Q is the energy demand, S the stock of energy-using capital, and U the rate of use.

The stock of equipment was considered fixed over the short term, with only the rate of use changing in response to exogenous factors such as changes in fuel prices. Changes were permitted in the capital stock over the long term in response to rising incomes and the obsolescence of the existing stock.

The energy used in the commercial sector was estimated on the basis of the floor space served. Additions to floor space were calculated by a

desired stock estimate (based on population, per capita income, school-age population, etc.), subtracting additions still standing from previous years.

The use of solar energy was estimated separately for the residential and nonresidential subsectors. The share of the capital market that is likely to be absorbed by solar systems in new buildings was approximated by an ad hoc relationship suggested by the Solar Resource Group of this study. It was assumed that retrofit of solar installations in existing buildings would make a negligible contribution. (This assumption, made before recent federal legislation providing substantial benefits for retrofit of solar installations, may be conservative. See, for example, “Space Heating and Cooling,” in chapter 6.)

Transportation14 Five categories of passenger transportation and four categories of freight transportation were considered in the analysis of this sector.

|

Passenger Transportation |

Freight Transportation |

|

Automobiles |

Truck |

|

Light trucks and vans |

Water |

|

Air travel |

Air |

|

Mass transportation |

Rail |

|

Other |

|

The model employed features of 10 major models constructed over the past 10 years, with a particular view to evaluating the effect on fuel consumption (under the assumptions of the detailed price scenarios shown in Table 11–2) of changes in the efficiency of fuel consumption by vehicles, load factors, prices for fuel, other operating costs, and capital expenditures for transportation. The effects of public policies were assessed by varying the input parameters.

The model assumes that fuel-price ratios (relative to 1975 in 1975 dollars), load factors, and efficiency ratios will increase linearly over the years ahead, but there is considerable uncertainty about the paths they will actually follow. The paths will probably be S-shaped, but since there is also substantial uncertainty about the endpoints (which are more important than the paths), the linear transition actually assumed is not critical. Other assumptions include the following.

-

Automobile travel: Fuel economies of new cars will increase to a plateau by 2000; the average fuel economy of the total fleet will lag behind new-car improvements by 10 years. Gasoline taxes per vehicle-mile (in 1975 dollars) will remain constant on the assumption (based on historical data) that the cost of building and maintaining highways will depend primarily on the vehicle-miles of use. Expenditures-per capita on autos (in 1975 dollars) will saturate; auto ownership itself is reaching saturation,

-

and the time spent in auto travel by each person (now about 50 min/day) is not likely to increase greatly. Data from the United States and other affluent countries indicate that there is a saturation effect in auto ownership at high income levels. Auto ownership in the United States is approaching one vehicle per licensed driver, although it is believed that a firmer upper limit in auto ownership is one vehicle per person of driving age (about 71 percent of the population in the United States).

-

Light-duty trucks and vans: The assumptions for this mode are essentially similar to those for automobiles, except for a slightly higher gasoline tax per vehicle-mile.

-

Air travel: The percentage of passenger transportation dollars spent on air travel will increase with rising incomes and saturation of expenditures on auto travel. The load factor will increase linearly until 2000 and remain constant thereafter. The energy intensity (Btu per passenger-mile) will decrease linearly until 2000 and remain constant thereafter.

-

Mass transportation15 and other passenger modes: All nonfuel operating costs (in 1975 dollars) will remain constant to 2010. For mass transportation, load factors rise in each scenario except B′, as shown below.

|

Average load factors in 2010 by scenario for mass transportation |

|

|

(1975) |

(17.9 passengers per vehicle) |

|

A*, A |

31.0 passengers per vehicle |

|

B |

27.0 passengers per vehicle |

|

C |

22.0 passengers per vehicle |

|

B′ |

17.9 passengers per vehicle |

-

The energy intensity of the vehicles used remains unchanged over the period.

-

All freight modes: The growth in all modes of freight transport per capita will be proportional to the growth in real GNP per capita. Where load factors and efficiencies change, they change linearly during the 1975–2010 period.

Industry16 The analysis of energy consumption in the industrial sector concentrated on 14 industries that account for 80 percent of the energy consumed by industry: 9 energy-consuming industries (agriculture, aluminum, cement, chemicals, construction, food, glass, iron and steel, and paper) and 5 energy-producing industries (oil and gas extraction, oil and gas refining, coal mining, synthetic fuels, and electrical generation). The energy these industries are likely to require in the future was estimated by multiplying the projected level of production for each industry in 2010 by its expected energy intensity. The projected growth

rates are displayed in Table 11–3. The data available to the panel were inadequate for determination of the energy-price/consumption elasticities within individual industries. The panel identified the technologies available for increasing the efficiency of energy use within each of the 14 industries, and estimated the extent to which these might be applied under the assumptions of each scenario. The technological possibilities are indicated qualitatively in Table 11–4.

In projecting the mix of old and new industrial plants for 2010, the panel assumed the prevailing retirement rate: 2 percent/yr for plants in operation in 1975. A third of today’s facilities would thus still be in use in 2010. This assumption may be conservative for the higher-price scenarios, as the energy cost of old equipment might accelerate replacement. In these scenarios, capital not needed for energy supply would be available for accelerated replacement of energy-consuming equipment.

The panel studied the patterns of energy use by the industries named and employed a few additional assumptions to derive preliminary estimates of the fuel mix for industry in 2010. The use of natural gas, for example, was assumed to be increasingly restricted under the assumptions of scenarios A, B, and B′ as a result of higher prices and policies governing scarcer fuels. In these scenarios, the use of natural gas was limited to special applications that justify the use of this high-quality fuel at higher prices (or under the terms of restrictive policies that might be imposed on its use). Since the price of coal is competitive with that of other fuels in the higher-price scenarios, it was assumed that most industrial generation of steam would be fired by coal in scenarios A, B, and B′, and that many existing processes fueled by oil and natural gas would be converted to coal by 2010. Scenario C assumes no restrictions on the availability of natural gas for industrial use.

On the advice of the Supply and Delivery Panel, the Demand and Conservation Panel assumed that solar energy would be economical for some low-temperature industrial applications if the prices of other sources rose appreciably. The panel assumed that the direct use of solar energy would replace that of natural gas to produce low-pressure steam and hot water for agriculture, food processing, and miscellaneous manufacturing processes, accounting for 0.2 quadrillion Btu (quad) of industrial energy consumption in scenario C, for example, and 1.8 quads in scenario A.

Integrating model17 Since the three sectoral analyses were carried out independently, the panel sought some means to array and correct their results in a model of the economy for 2010. The model used national economic data from the U.S. Department of Commerce18 for the year 1967 (the most recent at the time the panel conducted the analysis). Corrections were made for data from the sectoral analyses (using 1975 as

TABLE 11–3 Projection of Industrial Growth Rates from 1975 to 2010

|

Industry |

Growth Rate of Production 1960–1972 (percent per year) |

Ratio of Production Growth Rate to GNP Growth Ratea |

Initial Future Growth Rate Approximationb (percent per year) |

Modified Growth Rates for Final Projections (percent per year) |

Reasonsc for Modification |

||||

|

For 2 percent per year GNP Growth |

For 3 Percent per year GNP Growth |

||||||||

|

A |

B |

B |

C |

||||||

|

Agriculture |

1.6 |

0.39 |

0.8 |

1.2 |

1.7 |

1.7 |

1.7 |

1.7 |

1,2,8 |

|

Aluminum |

6.9 |

1.68 |

3.4 |

5.0 |

3.2 |

3.6 |

5.4 |

4.0 |

3,4 |

|

Cement |

3.6 |

0.88 |

1.8 |

2.6 |

1.8 |

1.8 |

2.6 |

1.8 |

|

|

Chemicals |

8.4 |

2.05 |

4.1 |

6.1 |

3.6 |

3.8 |

4.8 |

4.1 |

3,4,5 |

|

Constructiond |

3.8 |

0.93 |

1.8 |

2.8 |

0.7 |

0.7 |

1.0 |

0.7 |

1,3,6 |

|

Food |

3.3 |

0.80 |

1.6 |

2.4 |

2.2 |

2.2 |

3.2 |

2.2 |

1,8 |

|

Glass |

4.3 |

1.05 |

2.1 |

3.1 |

2.1 |

2.1 |

3.1 |

2.1 |

|

|

Iron and steel |

3.6 |

0.88 |

1.8 |

2.6 |

1.7 |

1.7 |

2.7 |

1.7 |

6,7 |

|

Paper |

5.4 |

1.32 |

2.6 |

3.9 |

1.9 |

1.9 |

2.9 |

1.9 |

5,6,7 |

|

Other manufacturing and mining activities |

4.8 |

1.17 |

2.3 |

3.5 |

2.2 |

2.2 |

3.2 |

2.2 |

6,7 |

|

aThe average growth rate in GNP (constant dollars) was 4.1 percent per year during the 1960–1972 period. bBased on the 1960–1972 ratio of production growth to GNP growth. cThe reasons are as follows: (1) Growth rate for this industry is relatively independent of the GNP growth rate. (2) Exports will cause a slight increase in the prevailing growth rate. (3) Product is energy intensive. High energy prices will lower the otherwise expected growth in demand. (4) Unique properties of products from this industry will tend to increase demand growth. (5) Market saturation will dampen present growth rates. (6) New technological developments will decrease the otherwise expected growth in demand. (7) Competing products will lower the growth rate of production in the United States. (8) Adjusted for assumed lower population growth rate. dAsphalt paving claims about half the energy used by the construction industry. Source: Adapted from National Research Council, Alternative Energy Demand Futures to 2010, Committee on Nuclear and Alternative Energy Systems, Demand and Conservation Panel (Washington, D.C.: National Academy of Sciences, 1979), p. 100. |

|||||||||

TABLE 11–4 Potential for Industrial Energy Conservation for 2010

|

|

Agriculture |

Aluminum |

Cement |

Chemicals |

Constructiona |

Food |

Glass |

Iron and Steel |

Paper |

Other User Industries |

|

Conservation Effect on Consuming Industriesb |

||||||||||

|

Basic “housekeeping” |

|

— |

— |

— |

|

— |

— |

— |

— |

— |

|

More recycling |

|

— |

|

|

— |

|

— |

|

— |

|

|

Environmental controls |

+ |

|

+ |

+ |

|

+ |

|

+ |

+ |

+ |

|

Conversion of gasoline engines to diesel |

— |

|

|

|

|

|

|

|

|

— |

|

Increased yield of product |

+ |

|

|

|

|

|

|

+ |

+ |

+ |

|

Changing product preference |

+ |

|

|

+ |

|

|

|

+ |

+ |

+ |

|

New basic process |

|

— |

— |

— |

|

— |

|

— |

— |

|

|

More waste heat recovery |

|

— |

— |

— |

|

— |

— |

— |

— |

— |

|

Cogeneration |

|

— |

— |

— |

|

— |

|

— |

— |

|

|

Substitute products |

|

|

|

|

— |

— |

|

|

|

|

|

Feedstock demand |

|

|

|

+ |

|

|

|

|

+ |

|

|

Lower-quality raw materials |

|

+ |

|

+ |

|

|

|

+ |

|

|

|

Conversion to electricity |

+ |

+ |

|

|

|

+ |

|

+ |

+ |

+ |

|

Estimated Net Reduction in Energy Intensity by Energy-Consuming Industriesc |

||||||||||

|

Scenario A |

15 |

45 |

40 |

26d |

42 |

34 |

31 |

28 |

36 |

43 |

|

Scenario B |

15 |

37 |

37 |

22d |

35 |

24 |

24 |

24 |

29 |

25 |

|

Scenario B′ |

15 |

37 |

37 |

22d |

35 |

24 |

24 |

24 |

29 |

25 |

|

Scenario C |

5 |

21 |

25 |

16d |

27 |

14 |

18 |

17 |

24 |

15 |

|

aAsphalt only. bA minus indicates reduction in energy intensity; a plus, increased energy intensity. cPercent reduction or increase in energy use per unit of production. dDoes not include chemical feedstocks. Source: Adapted from National Research Council, Alternative Energy Demand Futures to 2010, Committee on Nuclear and Alternative Energy Systems, Demand and Conservation Panel (Washington, D.C.: National Academy of Sciences, 1979), p. 104. |

||||||||||

TABLE 11–5 40 Sectors of the Integrating Model

|

Extraction, Processing, Conversion of Energy Coal mining Crude petroleum, natural gas Shale oil Coal gasification Coal liquefaction Refined petroleum products Natural gas utilities Coal combined-cycle electricity Fossil fuel electric utilities Light water reactors High-temperature gas-cooled reactors Renewable energy utilities |

Production of Goods and Services Agriculture Mining Construction Food Paper Chemicals Glass products Stone and clay products Iron and steel Nonferrous metals Intermediate goods Rail transport Bus transport Truck transport Water transport Air transport Wholesale and retail trades Other services Motor vehicles and equipment Consumer goods |

|

Energy Services, End-Uses Ore-reduction feedstocks Chemical feedstocks Motive power Process heat Water heat Space heat Air conditioning Miscellaneous uses of electricity |

the base year). The Department of Commerce data were supplemented by specific data on new energy technologies and processes to highlight the end-uses of energy and to express consumption of energy in physical, rather than monetary units, as the price of energy varies with the type of purchaser. A 40-sector model was constructed to characterize the economy. Twelve sectors represent the extraction, processing, and conversion of energy resources, 8 represent energy services or end-uses of energy, and the remaining 20 represent the sectors that produce nonenergy goods and services (see Table 11–5).

The interrelation between these sectors make up a 40×40 matrix of input-output coefficients. A typical element A represents the input required from sector i to produce one unit of output from sector j. The matrix manifests the state of technology by indicating the energy intensity (energy needed per unit of output) for the services and products of each sector. The results of the sectoral analyses were used to define the energy intensities and technologies (described below).

The model presents a simplified picture of energy flow through the economy. By tracing this flow through the sectors, the panel was able to derive self-consistent energy consumption figures for the scenarios.

TABLE 11–6 Demand for Energy Projected by Scenario A* for 2010 (quads)a

|

Energy Form |

Industryb |

Buildingsb |

Transportationb |

Total Demandb |

Conversion Lossc |

Primary Energy Input |

Efficiency (percent) |

|

Coal |

9.4 |

0.6 |

0.1 |

10.1 |

— |

10.1 |

100 |

|

Oil |

8.0 |

1.5 |

10.0 |

19.5 |

2.7 |

22.2 |

88 |

|

Gas |

5.8 |

1.6 |

0.1 |

7.5 |

0.5 |

8.0 |

94 |

|

Purchased electricityd |

2.4 |

2.7 |

— |

5.1 |

12.6 |

17.7 |

29 |

|

TOTAL |

25.6 |

6.4 |

10.2 |

42.2 |

15.8 |

58.0 |

73 |

|

aResults are shown to three significant figures to allow display of the small quantities under Transportation. bDemand for energy at point of consumption. cConversion losses include those incurred in extraction, refining, production, transmission, and distribution. dIncludes all energy sources projected for electricity generation—coal, oil, gas, hydroelectric, nuclear, geothermal, and solar. |

|||||||

The panel found it necessary to adopt some accounting conventions for this model. Total primary energy is defined as the total Btu content of the fossil fuels extracted plus the Btu equivalent of energy from hydroelectric, nuclear, solar, and geothermal sources (computed as the heat content of the coal it would take to generate the equivalent amount of electricity). Fossil fuels flow to the energy-producing sectors (for synthetic fuels and generation of electricity) and to the energy-consuming sectors. Tables 11–6 to 11–10 set out the inputs of energy to the energy-consuming sectors and the energy likely to be consumed in producing and distributing these inputs, and Table 11–11 gives figures for 1975. Adding these losses to the inputs flowing into the energy-consuming sectors yields the total primary energy input to the economy.

Each element in the 40×40 matrix (A) may change over the next three decades as production technologies change. Specifying all these possible changes would be a laborious task. The most significant changes (for projecting possible paths of reducing energy consumption through conservation techniques) will occur in those aspects of production technologies that have the greatest effect on demand for energy. To identify these aspects, “energy input fractions” (gi,j below)—each the fraction of the total energy intensity of a product from sector j (∈j) that is

TABLE 11–7 Demand for Energy Projected by Scenario A for 2010 (quads)a

|

Energy Form |

Industryb |

Buildingsb |

Transportationb |

Total Demandb |

Conversion Lossc |

Primary Energy Input |

Efficiency (percent) |

|

Coal |

10.7 |

— |

0.1 |

10.8 |

|

10.8 |

100 |

|

Oil |

8.7 |

2.2 |

14.0 |

24.9 |

3.2 |

28.1 |

89 |

|

Gas |

6.2 |

2.5 |

0.1 |

8.8 |

0.5 |

9.3 |

95 |

|

Purchased electricityd |

2.6 |

4.8 |

— |

7.4 |

18.0 |

25.4 |

30 |

|

TOTAL |

28.2 |

9.5 |

14.2 |

51.9 |

21.7 |

73.6 |

70 |

|

aResults are shown to three significant figures to allow display of the small quantities under Transportation. bDemand for energy at point of consumption. cConversion losses include those incurred in extraction, refining, production. transmission, and distribution. dIncludes all energy sources projected for electricity generation—coal. oil, gas. hydroelectric, nuclear, geothermal, and solar. |

|||||||

TABLE 11–8 Demand for Energy Projected by Scenario B for 2010 (quads)a

|

Energy Form |

Industryb |

Buildingsb |

Transportationb |

Total Demandb |

Conversion Lossc |

Primary Energy Input |

Efficiency (percent) |

|

Coal |

12.6 |

— |

0.1 |

12.7 |

— |

12.7 |

100 |

|

Oil |

10.0 |

2.9 |

19.4 |

32.3 |

5.8 |

38.1 |

85 |

|

Gas |

6.9 |

3.4 |

0.1 |

10.4 |

0.6 |

11.0 |

94 |

|

Purchased elec-tricityd |

3.1 |

6.3 |

— |

9.4 |

22.7 |

32.1 |

29 |

|

TOTAL |

32.6 |

12.6 |

19.6 |

64.8 |

29.1 |

93.9 |

69 |

|

aResults are shown to three significant figures to allow display of the small quantities under Transportation. bDemand for energy at point of consumption. cConversion losses include those incurred in extraction, refining, production, transmission, and distribution. dIncludes all energy sources projected for electricity generation—coal, oil, gas, hydroelectric, nuclear, geothermal, and solar. |

|||||||

TABLE 11–9 Demand for Energy Projected by Scenario B′ for 2010 (quads)a

|

Energy Form |

Industryb |

Buildingsb |

Transportationb |

Total Demandb |

Conversion Lossc |

Primary Energy Input |

Efficiency (percent) |

|

Coal |

17.5 |

— |

0.2 |

17.7 |

— |

17.7 |

100 |

|

Oil |

14.2 |

3.7 |

26.9 |

44.8 |

11.8 |

56.6 |

79 |

|

Gas |

9.6 |

4.6 |

0.2 |

14.4 |

1.4 |

15.8 |

91 |

|

Purchased electricityd |

4.4 |

8.6 |

0.1 |

13.1 |

30.4 |

43.5 |

30 |

|

TOTAL |

45.7 |

16.9 |

27.4 |

90.0 |

43.6 |

133.6 |

67 |

|

aResults are shown to three significant figures to allow display of the small quantities under Transportation. bDemand for energy at point of consumption. cConversion losses include those incurred in extraction, refining, production, transmission, and distribution. dIncludes all energy sources projected for electricity generation—coal, oil, gas, hydroelectric, nuclear, geothermal, and solar. |

|||||||

TABLE 11–10 Demand for Energy Projected by Scenario C for 2010 (quads)a

|

Energy Form |

Industryb |

Buildingsb |

Transportationb |

Total Demandb |

Conversion Lossc |

Primary Energy Input |

Efficiency (percent) |

|

Coal |

9.6 |

— |

0.1 |

9.7 |

— |

9.7 |

100 |

|

Oil |

9.7 |

4.0 |

25.9 |

39.6 |

9.7 |

49.3 |

81 |

|

Gas |

13.9 |

7.0 |

0.1 |

21.0 |

4.8 |

25.8 |

81 |

|

Purchased electricityd |

5.8 |

9.3 |

0.1 |

15.2 |

34.8 |

50.0 |

30 |

|

TOTAL |

39.0 |

20.3 |

26.2 |

85.5 |

49.3 |

134.8 |

64 |

|

aResults are shown to three significant figures to allow display of the small quantities under Transportation. bDemand for energy at point of consumption. cConversion losses include those incurred in extraction, refining, production, transmission, and distribution. dIncludes all energy sources projected for electricity generation—coal, oil, gas, hydroelectric, nuclear, geothermal, and solar. |

|||||||

TABLE 11–11 Demand for Energy in 1975 (quads)a

|

Energy Form |

Industryb |

Buildingsb |

Transportationb |

Total Demandb |

Conversion Lossc |

Primary Energy Input |

Efficiency (percent) |

|

Coal |

3.8 |

0.2 |

— |

4.0 |

— |

4.0 |

100 |

|

Oil |

5.3 |

5.4 |

16.7 |

27.4 |

2.5 |

29.9 |

92 |

|

Gas |

8.6 |

7.6 |

0.6 |

16.8 |

— |

16.8 |

100 |

|

Purchased electricityd |

2.3 |

3.6 |

— |

5.9 |

14.2 |

20.1 |

29 |

|

TOTAL |

20.0 |

16.8 |

17.3 |

54.1 |

16.7 |

70.8 |

76 |

|

aResults are shown to three significant figures to allow display of the small quantities under Transportation. bDemand for energy at point of consumption. cConversion losses include those incurred in extraction, refining, production, transmission, and distribution. dIncludes all energy sources projected for electricity generation—coal, oil, gas, hydroelectric, nuclear, geothermal, and solar. |

|||||||

embodied in the input from sector i (∈j)—were calculated for the base year by the equation

and ordered by rank.

Computing the energy input fractions brought several aspects of energy consumption into sharper focus. In the production of automobiles, for example, calculating the energy input fractions revealed that the energy consumed in assembly accounts for only 10 percent of the total energy cost, while more than a third of the total energy cost can be attributed to the energy used in producing steel. Thus, from the perspective of energy conservation, the size, weight, and material composition of automobiles manufactured in 2010 are more important to the energy consumption than the degree to which assembly is mechanized.

Changes in production techniques were defined by multiplying factors, applied term by term to important elements of the A matrix. Energy can be conserved in two ways in the production of goods and services: by reducing energy inputs, or by replacing these inputs with nonenergy inputs. Industry experts on the panel (and others consulted by the panel) estimated the type and extent of conservation that might be practiced as energy prices rise.

The panel selected the technological changes that seemed most plausible

and assessed their effects under the conditions of various scenarios. (For a detailed description of this model and a complete set of the energy input fractions used to calculate total demand for energy in 2010, see the report of the Demand and Conservation Panel.19

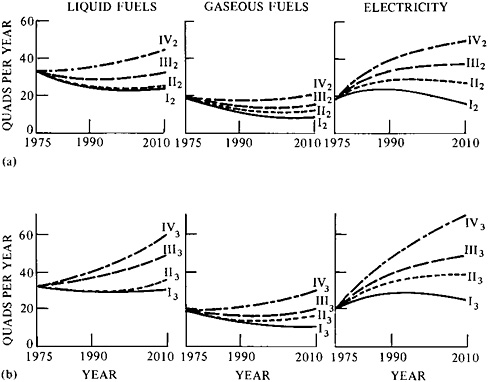

Demand for Electricity

Each of the resource groups of the Demand and Conservation Panel (buildings, industry, and transportation) was asked to estimate the minimum and maximum amounts of purchased electricity required by each of the basic scenarios (A* and B′ being considered variants). The estimation of demand for electricity, as stressed several times in this report, is difficult and controversial.*

The maximum and minimum figures are set out in Table 11–12. The figures for the maximum amount of purchased electricity in the buildings sector proceed from the assumption that almost all space heating in the high-energy scenarios is provided by electricity. The maximum figures for the industrial sector entail the electrification of many processes and no self-generation of electricity. For the maximum figures in the transportation sector, however, the sector is assumed to continue operating primarily on liquid fuels; major advances in the storage of electrical energy (such as high-efficiency batteries) could radically alter this projection.

The penultimate line of Table 11–12 gives the percentage of total primary energy use claimed by electricity in each projection: a range of one quarter to one half. (See also “Electricity” under “Implications of Study Results: Comparisons of Supply and Demand” in this chapter.)

Minimum Energy-Use Scenario (CLOP)20

The Consumption, Location, and Occupational Patterns (CLOP) Resource Group of the Synthesis Panel developed a scenario of energy consumption moderated by shifting attitudes and preferences rather than by rising prices. The group speculated that attitudes emerging in younger generations (for example, thrift in the use of all resources and a preference for environmental quality at the expense of material consumption) might dominate the choices of American society in 2010. Significant changes assumed in the CLOP scenario include major occupational shifts from the employment of individuals in large organizations to self-employment and employment in small groups; increased emphasis on recreational and leisure activities, in forms that consume little material or energy (e.g., cultural activities); and new patterns of settlement that decrease the need

|

* |

See statement 11–4, by R.H.Cannon, Jr., Appendix A. |

TABLE 11–12 Projections of Maximum and Minimum Demand for Purchased Electricity in 2010 (quads)

|

|

Scenario Aa |

Scenario B |

Scenario C |

1975 (actual) |

|||

|

Minimum |

Maximum |

Minimum |

Maximum |

Minimum |

Maximum |

||

|

Buildings |

11 |

22 |

14 |

26 |

21 |

44 |

11 |

|

Industry |

8 |

17 |

9 |

20 |

18 |

23 |

7 |

|

Transportation |

— |

4 |

— |

4 |

— |

4 |

— |

|

TOTAL |

19 |

43 |

23 |

50 |

39 |

71 |

18 |

|

Primary energy |

74 |

94 |

134 |

|

|||

|

Electricity (percent of primary energy) |

26 |

55 |

24 |

53 |

29 |

53 |

28 |

|

Average annual electricity growth (percent)b |

0.2 |

2.5 |

0.7 |

3.0 |

2.2 |

4.0 |

— |

|

aA major shift to electricity for ground transportation is not assumed here. However, if about half of transportation were shifted to electricity by 2010 the additional electrical demand, beginning in 1990, would be approximately 5 GWe/yr. bOver the period 1975–2010. Source: Adapted from National Research Council, Alternative Energy Demand Futures to 2010, Committee on Nuclear and Alternative Energy Systems, Demand and Conservation Panel (Washington, D.C.: National Academy of Sciences, 1979), p. 208. |

|||||||

for energy in transportation. This scenario relies heavily on sophisticated technologies to provide high-quality services and conserve exhaustible resources of energy and materials—solar energy, advanced engine designs, extensive telecommunications systems, and rationalized transportation networks.

Energy consumption in the CLOP scenario totals 53 quads in 2010—a value surprisingly close to that projected by the Demand and Conservation Panel in scenario A* (58 quads), and about half the energy consumed today on a per capita basis. The assumptions of this low-energy projection, however, are distinct. Nuclear power has been phased out, and oil and gas imports have been reduced to zero. The demand for liquid and gaseous fuels is about half that of 1975, and no coal is converted to liquid fuels. The accelerated introduction and expansion of solar technologies in the CLOP scenario result in 10 quads from this source by 2010.

The pattern of energy consumption between 1975 to 2010 was not investigated by the CLOP group.

Total Primary Energy Use

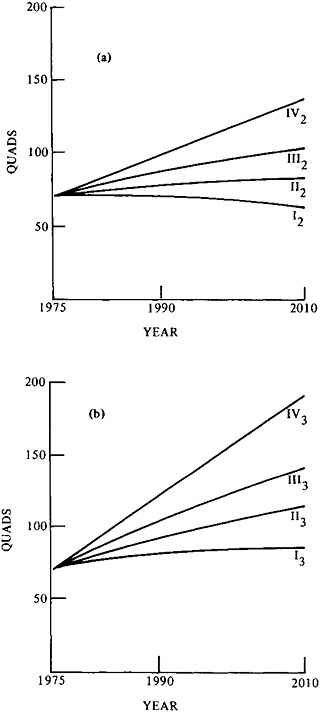

Figure 11–4 maps the various paths projected by the Demand and Conservation Panel and shows the endpoints projected by scenario A* and by the CLOP scenario for 2010. These projections were based on the results of the individual sectoral analyses for 1990 and the integrating model for 2010. They indicate how the amount of energy consumed might vary over a wide range—from 53 to 135 quads*—as a result of different prices for energy, rates of growth in GNP, the rate at which available energy-conserving technology is applied, and various public policies. While the projection of lowest growth in the use of energy (A*) assumes some changes in the preferences and life-style choices of energy consumers, these are modest. The projections of the Demand and Conservation Panel depend principally on factors that stimulate (to a greater or lesser degree) the conservation of energy by the application of known technology and practices, rather than depending on fundamental changes in consumer choices or patterns of living and working. This latter pathway to lower energy consumption was investigated qualitatively by the Consumption, Location, and Occupational Patterns Resource Group of the Synthesis Panel, as described in the previous section.

WORK OF THE SUPPLY AND DELIVERY PANEL21

Supply and Delivery Panel was originally expected to generate supply curves, i.e., projections of the amount of each energy form or source that could be produced as a function of time and price. However, the panel concluded that production would be so much influenced by nonprice variables that conventional supply curves would be relatively meaningless. Instead, the panel attempted practical assessments of the conditions of resource recovery and the rate of use of new production technologies, measured against the political and economic forces that influence the decisions of energy resource producers, utilities, and heavy industrial consumers of energy. The practical and judgmental nature of their investigation provides frequent counterpoints to the findings of other panels and resource groups. For example, the Demand and Conservation Panel assumed that under the conditions of their scenarios, sufficient capital would be available for investment in producing the energy

|

* |

See statement 11–5, by R.H.Cannon, Jr., Appendix A. |

resources needed to meet demand in each scenario. The Supply and Delivery Panel replied bluntly that under prevailing conditions, financiers and potential owners would consider investment in new energy supplies to be unacceptably risky, principally because of uncertainties in government policy, regulatory requirements, and delays in acquiring licenses and permits. Thus, for example, the demands projected in scenario B′ could not be met without significant policy changes or greatly increased petroleum imports.

The committee emphasizes that the major point of both panels’ work is that policies enacted to balance energy supply and demand while maintaining satisfactory economic performance must be consistent and sustained. To make the required investments in energy production and end-use capital, consumers and suppliers must be able to read these policies as clear signals encouraging, maintaining, or discouraging various levels of production or end-use. In practice, given policies are likely to be read as different signals by the producers of each energy resource. The Supply and Delivery Panel asked each of its resource groups to estimate the production of its resource or energy form under three sets of conditions and assumptions: business as usual, enhanced supply, and national commitment. The specific conditions assumed for each of these categories varied with the resource. In general, the business-as-usual estimates assumed that existing policies and practices22 carry over into the future with little change. Enhanced-supply estimates assumed that promising new supply technologies are encouraged by policies effected for energy resource production; for example, relaxing environmental standards, or reducing and expediting required regulatory processes. The national-commitment estimates assumed that the policies and regulatory actions of enhanced supply are pursued with urgency. It must be emphasized that policies of national commitment cannot be effected simultaneously for all supply sources. Giving very high priority to the development of one source necessarily implies lower priority and less stimulus to the development of other sources.23

The Supply and Delivery Panel’s resource groups reviewed available estimates of reserves and resources, as well as their producibility, and selected those that matched their consensus judgment. In addition, they considered the availability of the various energy supply technologies during the period to 2010 for each of the three sets of assumed conditions. Table 11–13 displays the estimates of each resource group under the three categories of policy.

The specific assumptions made by each group are set out in Table 11–14. The Supply and Delivery Panel emphasizes that neither table should be read as representing self-consistent sets of possibilities. Many of these estimates presume success with technologies that either have not yet been

tested or have been demonstrated only on small scales. It is possible that some of the prospective technologies on which these estimates are based cannot be successfully developed with any level of commitment. On the other hand, new supplies from unexpected discoveries (of unconventional gas, for example) or from unexpected technical progress in certain technologies (such as solar photovoltaics or coal liquefaction) could outstrip specific estimates.

Maximum-Solar Scenario

To analyze the extent to which solar energy can substitute for other fuels, a “maximum solar” scenario was developed by the Solar Resource Group of the Supply and Delivery Panel.24 It represents an estimate of the maximum feasible application of solar energy between now and 2010, from the point of view of technical, rather than economic, feasibility. The group concluded that increased energy prices, within the range considered by the study, would not be sufficient to stimulate widespread use of solar energy by 2010. Heavy subsidies and government mandates would be needed to encourage installation of solar energy systems in that period to the extent described by the maximum-solar scenario.

This scenario assumes that a national policy decision has been made by 1985 to encourage the use of solar energy in all its applications. The government mandates that solar energy be used to supply heat, air conditioning, and hot water to all new buildings, and to supply industrial process heat where technically feasible. A schedule is set in motion for several solar electric central generating stations, and state and local governments are ordered to adopt as rapidly as possible technologies for converting municipal and agricultural wastes to useful energy. These installations might be financed in part from revenues received from taxing nonrenewable energy sources, a practice that would also help make the solar installations more competitive.

Estimates for the maximum potential application of solar energy are set out in Table 11–15. These numbers represent an effective upper bound on solar energy production. Whether this quantity and mix could be effectively used depends on prevailing conditions. The panel made no attempt to estimate the cost of achieving this projection. More details about this scenario and its context in the study are given in chapter 6.

CONAES Projections of Supply Versus Other Projections

For ready comparison, the estimates of the Supply and Delivery Panel for the year 2000 and the year 2010 are compared to the most recent midrange

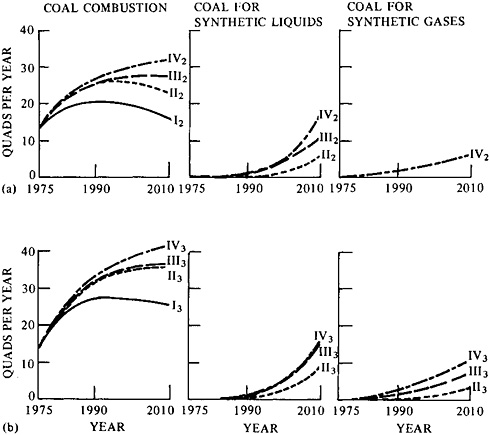

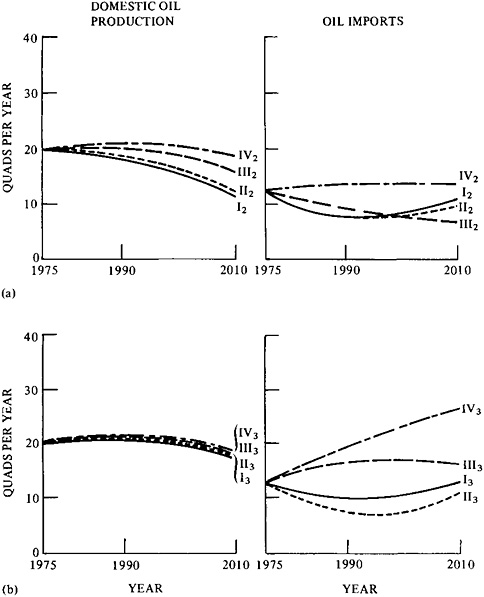

TABLE 11–13 Domestic Energy Production for Three Sets of Assumed Conditions (quads per year)a

|

Scenario and Energy Source |

Year |

|||

|

1977 |

1990 |

2000 |

2010 |

|

|

Business as usualb |

|

|

|

|

|

Crude oil |

19.6 |

16.0 |

12.0 |

6.0 |

|

Natural gas |

19.4 |

10.3 |

7.0 |

5.0 |

|

Oil shale |

0 |

0 |

0 |

0 |

|

Synthetic liquidsc |

0 |

(0.3) |

(2.3) |

(6.1) |

|

Synthetic gasc |

0 |

(1.3) |

(3.5) |

(4.1) |

|

Coal |

16.4 |

25.0 |

34.0 |

42.0 |

|

Geothermal |

0 |

0.4 |

0.9 |

2.4 |

|

Solar |

0 |

0 |

0.1 |

0.6 |

|

Nuclear |

2.7 |

10.0 |

12.5 |

15.8 |

|

Hydroelectric |

2.4 |

4.0 |

5.0 |

5.0 |

|

Enhanced supplyb |

|

|

|

|

|

Crude oil |

19.6 |

20.0 |

18.0 |

16.0 |

|

Natural gas |

19.4 |

15.8 |

15.0 |

14.0 |

|

Oil shale |

0 |

0.7 |

1.0 |

1.5 |

|

Synthetic liquidsc |

0 |

(0.4) |

(2–4) |

(8.0) |

|

Synthetic gasc |

0 |

(1.7) |

(3.5) |

(4.8) |

|

Coal |

16.4 |

26.6 |

37.2 |

49.5 |

|

Geothermal |

0 |

0.6 |

1.6 |

4.1 |

|

Solar |

0 |

1.7 |

5.9 |

10.7 |

|

Nuclear |

2.7 |

13.0 |

29.5 |

41.7 |

|

Hydroelectric |

2.4 |

4.1 |

5.0 |

5.0 |

|

National commitmentb |

|

|

|

|

|

Crude oil |

19.6 |

21.0 |

20.0 |

18.0 |

|

Natural gas |

19.4 |

18.0 |

17.0 |

16.0 |

|

Oil shale |

0 |

2.0 |

2.5 |

3.0 |

|

Synthetic liquidsc |

0 |

(0.7) |

(4.7) |

(12.9) |

|

Synthetic gasc |

0 |

(1.7) |

(4.5) |

(7.9) |

|

Coal |

16.4 |

32.5 |

75.0 |

100.0 |

|

Geothermal |

0 |

2.2 |

7.8 |

19.9 |

|

Solar |

0 |

3.3 |

13.1 |

28.8 |

|

Nuclear |

2.7 |

12.0 |

27.5 |

42.5 |

|

Hydroelectric |

2.4 |

4.1 |

5.0 |

5.0 |

|

aExcept for the business-as-usual projections, the entries in this table should not be added to obtain yearly totals; no more than a very few energy sources or technologies could be simultaneously accorded the priorities implied by the enhanced-supply or national-commitment scenarios. bFor specific assumptions guiding selection of estimates under this set of conditions, see Table 11–14. cSynthetic fuels are produced from coal and oil shale and are not added in the totals. Source: Compiled from National Research Council, U.S. Energy Supply Prospects to 2010, Committee on Nuclear and Alternative Energy Systems, Supply and Delivery Panel (Washington, D.C.: National Academy of Sciences, 1979). |

||||

TABLE 11–14 Assumptions Specific to Energy Resource Estimates

|

Energy Source |

Scenarioa |

||

|

Business as Usual |

Enhanced Supply |

National Commitment |

|

|

Coal |

Production limited by difficulties teasing federal land; increasing costs and delays from lack of consistent environmental policies |

Increased demand from enactment of consistent environmental policies |

Rising worker productivity; availability of more capital; streamlined regulatory policies |

|

Oil and gas |

Price controls discourage domestic production; separate permits required for exploration and production in outer continental shelf; delays in leasing; withdrawal of public lands |

Accelerated federal offshore leasing; lifting of controls on wellhead prices; streamlined permit processes; improved exploration and production technologies |

Relaxation of Clean Air standards; streamlined procedures for environmental impact statements; federal loan guarantees for development and application of new technologies; federal return of withdrawn lands; assignment of priority status to materials and labor for oil exploration and recovery |

|

Coal-based synthetics (oil and gas) |

Federal nonrecourse loans for a limited number of new plants: design and construction of such plants takes 6 years (production in seventh year) |

Permits for mining, plant construetion, and operation acted upon within 12 months: design and construction of such plants takes 5 years |

Government agency established to underwrite prices, expedite approval of permits, act to ensure priority assignment of labor, capital, and materials, and so on: design and construction of plants takes 4 years |

projection (Series C) of the Energy Information Administration (EIA)25 in Table 11–16. The EIA projections were made in 1978.

The EIA projections for both oil and gas, assuming enhanced-recovery techniques, are above even the national-commitment scenario of the Supply and Delivery Panel—about 30 percent above in the case of oil, and 20 percent above in the case of gas. The projection of oil and gas production in the year 2000, including enhanced recovery and all synthetics, totals 62.7 quads in the Series C projections of EIA. For 2010, the production of oil and gas, including all synthetics, totals 67.0 quads in the Series C projection. The Supply and Delivery Panel projects oil and gas production of 50.4 quads in 2000 and 58.3 quads in 2010 under the conditions of the national-commitment scenario. The CONAES projections for fluid fuels appear conservative in this context. Nevertheless, additions to domestic oil reserves in 1978 were only 1.3 billion barrels, compared to production of 3.2 billion barrels. To maintain domestic production of oil through the 1980s would require an average annual finding rate of 4.0 billion barrels.26

Several additional points of comparison emerge from inspection of Table 11–16:

-

The EIA projections for coal-derived synthetic liquids agree quite well with those of the enhanced-supply scenario for both 2000 and 2010.

-