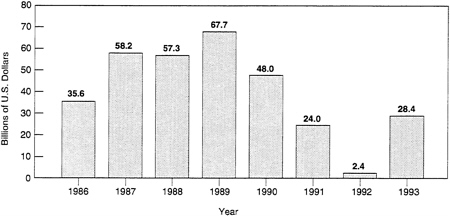

FIGURE 2 Foreign direct investment in the United States. Inflows, current-cost basis, 1986–1993. SOURCE: Flow of Funds Accounts: Flows and Outstandings, Fourth Quarter 1993. Board of Governors of the Federal Reserve System, Washington, D.C., March 9, 1994.

SOURCES OF LOWER SAVING

What are the sources, then, of the exceedingly low U.S. saving rate? The federal deficit currently represents dissaving of more than 3.5 percent of GDP. This dissaving effect will decline below 3.0 percent by the end of the current 5-year budget agreement if all of its provisions are implemented. Thereafter, it will rise steadily without a renewed commitment to decreasing the annual deficit. The federal budget deficit is a problem for three reasons: the impact on national savings just described; the possibility that foreign financed debt will not be rolled over as it matures; and the cumulative deficits that run year after year (known as the federal debt), causing interest payments to consume more of the federal budget and constraining the government ’s ability to fund important programs without additional revenues and/or upward pressure on the budget deficit. Table 6 summarizes the federal budget outlook. These projections are made on the assumption that the provisions of the Omnibus Budget Reconciliation Act of August 1993 will be successfully implemented. They do not allow for likely expenditures, some of them off-budget, for example, for defaults on government-sponsored guarantees, natural disaster recovery, and health care reform if enacted. Even with optimistic assumptions, by 1998 interest payments would still represent 3.0 percent of GDP and about 15 percent of the federal budget.

Because the deficit accounts for about one-half of the nation’s saving

TABLE 6 Budget Outlook Through 2004 (By fiscal year)

problem, deficit reduction is necessary to increase saving over the next 5 years. Nevertheless, declining private saving has also been an important contributor to the falling national saving rate. Several factors may be contributing to this decline in addition to the obvious effect of job insecurity and earnings declines for many workers. The factors include the changing age structure of the U.S. population and less need for saving because of high capital gains in the real estate and stock market and improvements in the social insurance safety net, but there is little scholarly consensus on their relative importance (Congressional Budget Office, 1993; Poterba, 1994). Partly because of this lack of a comprehensive understanding of the dynamics of private saving, it is difficult to predict how changes in government policy will affect the saving rate. The board believes that additional international comparative studies of the differences in private sector saving would help illuminate this phenomenon. It should be a priority of the scholarly economics profession and research funding organizations. 6

U.S. saving and investment patterns will not change quickly. Movement onto a different trajectory will probably take several years. Although the low saving and investment rates are not likely to create a crisis in the short run, over the course of a decade sustained differentials of this size will seriously erode productivity growth, efficiency in global markets, and job creation and hence most other economic and social goals that depend upon these fundamentals.

The board is aware that a sudden increase in saving in the United States would not necessarily be accompanied by a sudden increase in a combination of domestic and foreign direct investment. For example, a rapid reduction in the federal deficit might reduce aggregate demand and hence induce a recession rather than a move to a sustained growth path. The transition to a different long-term growth path should be gradual to avoid disrupting the recovery. Our concern is that a sustained recovery, especially if it is accompanied by a slowdown in corporate restructuring, will relieve what little pressure there is to focus on increasing investment and saving across cycles.

To summarize, investments in corporate tangible and intangible as

|

6 |

The Organization for Economic Cooperation and Development (OECD) has underway a major comparative study of the effects of tax policies on aggregate levels and allocations of household saving (scheduled for completion in fall 1994). The board’s recommended research and synthesis would examine many factors that affect saving, such as credit institutions, demography, structure of financial markets, and tax policy and would attempt to arrive at a consensus regarding total private saving, not just household saving, in different national contexts. |