4

Operational Makeup of the Maritime Oil Transportation Industry

The committee has been asked to identify the nature and extent of changes (e.g., changes in tank vessel ownership and tank vessel type) in the maritime oil transportation industry and the safety implications of changes that may be related to OPA 90 (Section 4115). The committee will also:

-

determine if the utilization of deep-water ports (such as the Louisiana Offshore Oil Port [LOOP]) has been affected by OPA 90 and the exemptions

-

determine if vessels are being removed from service earlier than usual because of restrictions imposed by OPA 90 or IMO Rules 13F and 13G

-

evaluate changes in fleet composition resulting from OPA 90 and IMO regulations

This analysis will be based on a comparison of two base years: 1990 (before the enactment of OPA 90) and 1994 (the last year for which complete data is available). Sizes of vessels will be broken down into two broad groupings for which data are available: 5,000 to 150,000 DWT and 150,000 DWT and above. To evaluate the effect of the double-hull requirement on the composition of the industry, double-hull tankers will be distinguished from nondouble-hull tankers. The latter will be broken down into pre-MARPOL and MARPOL designs. Sales of tankers will be analyzed to determine the effects of OPA 90 or IMO (e.g., if Section 4115 is the reason for sale and, specifically, if the retirement of pre-MARPOL ships has been accelerated because of OPA 90 or IMO).

Data will be obtained from the U.S. Department of Commerce, Lloyd 's Register of Shipping, Drewry, Clarkson, and other chartering and sale and purchase brokers. In the case of two-tier markets, most of the information will probably be provided by narrative input from brokers and shipowners. Data on future trends

in the composition of the market may come from shipbuilders, owners, and brokers, and from extrapolation; thus, they are likely to be imprecise. Even data from the past may not be helpful because of the lack of standardization in size categories and the lack of attention to varieties of hull type in the usual reference sources.

OWNERSHIP, 1990 VERSUS 1994

The purpose of this task is to determine the effect of OPA 90 on vessel ownership patterns, as analyzed according to trading patterns and the size of oil tankers calling on U.S. ports. Previous ownership patterns and the size of oil tankers calling on U.S. ports before and after OPA 90 will be determined by analyzing data from Lloyd 's Maritime Information Services and the Institute of Shipping Analysis in Göteborg, Sweden. These data cover all tanker vessel shipments for vessels of more than 30,000 DWT for 1990 and 1994. The data specify vessel name, vessel owner, size, cargo loaded, cargo type, departure port, flag, and coast of call (i.e., Atlantic, Gulf, or Pacific).

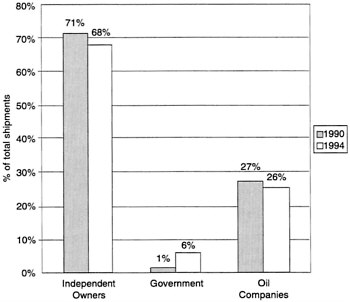

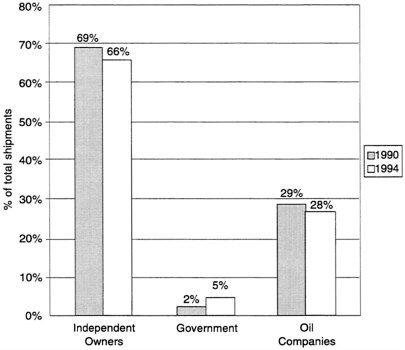

Relevant aggregates of the data will be developed for analyses, such as those shown in figures 4-1 and 4-2. These figures show oil shipments, by percent of shipments and by percent of volume, to the United States by shipowner category for 1990 and 1994, respectively. In this aggregation, vessel owners are identified and classified into one of three categories: oil companies, governments (such as Saudi Arabia), or independent shipowners. Ownership is defined as a full or majority ownership stake in the vessel. Vessels on long-term bare-boat charter or lease to oil companies are classified as oil company vessels.

Data on tank vessel movements have been acquired for 1990 and 1994 according to coast of call (Atlantic, Gulf, Pacific), vessel owner category (oil company, government, or independent), vessel size, number of shipments, total tons shipped, and age of the vessel. This information, as well as data on ownership and the sale and purchase of vessels, will be compiled by the Institute of Shipping Analysis, Göteborg, Sweden; Fearnley Research, Oslo, Norway; United Tankers, Göteborg, Sweden; and Drewry Shipping Consultants, London.

USE OF LIGHTERING AND OFFSHORE PORTS, 1990 VERSUS 1994

OPA 90 allows single-hull tank vessels, which would otherwise have been phased out, to continue to off-load cargo in the United States until January 1, 2015, by utilizing offshore deep-water ports and designated offshore lightering zones.1 These exemptions may have the overall effect of increasing the volume of oil transported through deep-water port and lightering systems.

|

1 |

Lightering is the process of transferring cargo, such as crude oil, from one floating vessel to another. Lightering is used principally to remove cargo from larger vessels to smaller, lower draft vessels that can enter shallow ports common to the Atlantic and Gulf of Mexico coasts of the United States. |

FIGURE 4-1 Change in oil shipments to the United States, 1990 and 1994. Note: Compiled using data received from the Institute of Shipping Analysis, Göteborg, Sweden (see appendix D). Totals do not reflect 100%.

The committee will first establish historic trends in use of lightering and offshore ports for supplying U.S. refineries with crude oil. Historic data on lightering and offshore port use will be obtained from the Louisiana Offshore Oil Port (LOOP), the only existing offshore port, and published by the U.S. Department of Commerce for crude oil imports to the United States; data will be presented in the aggregate and also on a regional basis.

The historic trend will be used to project future patterns in lightering and offshore port use, from which estimates of direct, lightered, and offshore port deliveries of imported crude will be made. Where possible, regional analyses of crude oil imports will be made.

One of the uncertainties affecting changes in offshore port development and lightering patterns is the possibility of new deep-water unloading ports, such as a recently announced 2.4-million-barrel-per-day port, to be located 35 miles off the Texas coast, for unloading very large crude carriers (Oil and Gas Journal, 1995). In 1994 the city of Corpus Christi began investigating an offshore terminal to

FIGURE 4-2 Change in the volume of oil shipped to the United States, 1990 and 1994. Note: Compiled using data received from the Institute of Shipping Analysis, Göteborg, Sweden (see appendix D).

serve the south Texas coast. The establishment of more ports in the Gulf of Mexico is a function of expected import volume, economics, and political pressures. Although the analysis by the committee will not address complex political variables, it will project import volume to 2010. No attempt will be made, however, to project the availability of more ports. If new deep-water ports are built in the U.S. Gulf of Mexico, the location of unloading and lightering related to those ports will be affected. The final committee report will address the general implications of changes in unloading patterns.

PATTERNS OF SALES, TRANSFERS, AND SCRAPPING

The committee will determine the impact of Section 4115 on the patterns of vessel sales, transfers, and scrappings between 1990 and 1994. The committee will also review how changes in these patterns have affected the operational makeup of the maritime oil transportation industry. In addition, the committee

will attempt to predict further changes in the operational makeup of the industry that might occur because of OPA 90 (Section 4115).

The committee will collect data from various industry sources, such as Drewry and the Institute of Shipping Analysis, to establish tanker sales and ship transfers for the years 1990 through 1994. This information will be separated into categories, such as oil company, independent, and government fleets, to determine significant trends in the operational makeup of the tanker industry. Similar data may be required for the oceangoing barge industry in the United States, and, if so, these data will be obtained from the U.S. Coast Guard and verified by the American Waterway Operators. In addition, the committee will need data concerning changes in the tanker and oceangoing barge fleet operating under the Jones Act.

The data for tankers and barges will be analyzed to determine if changes are attributable to OPA 90 (Section 4115). In this area, however, the effect of OPA 90 (Section 4115) may not yet be apparent in actual sales and transfers. As additional information is obtained, the committee expects, but can not ensure, that future trends can be projected.

FINDINGS

The committee expects that available sources will be adequate, particularly for transactions involving larger vessels, the ownership of which is usually better documented than for smaller ships. Inevitably, there will be cases where the identity of buyers cannot be determined, especially in recent transactions, and this may affect the reliability of data on transfers between owners groups.

The policy adopted by some oil companies of making special arrangements with independent owners and managers to handle tankers they formerly owned introduces an element of doubt regarding ownership. This relationship cannot be assessed for at least several years. Judgments about the quality of operation are highly subjective, in any case, and none of the available criteria is entirely satisfactory.

Available data are based on different size categories, making an accurate assessment difficult. The overall figures will probably be correct, but the subdivisions may be less so. Ships often carry partial cargoes, which can effectively shift them into a different category, and crude carriers sometimes carry petroleum products (or vice versa). These variables should not invalidate conclusions, however.

Changing shipping patterns is another area of uncertainty. Whether new deep-water, offshore terminals will actually be built in the Gulf of Mexico, and, if so, when, are still unanswered questions. The use of offshore terminals and lightering zones will be governed by tanker economics. If lightering or deep-water ports are less expensive than direct shipments, their use will certainly increase as a percentage of total shipping (number of tank vessels and crude oil tonnage).